Concept explainers

Videos

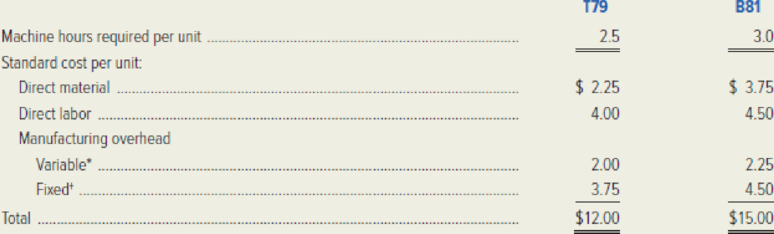

Upstate Mechanical, Inc. has been producing two bearings, components T79 and B81, for use in production. Data regarding these two components follow.

*Variable manufacturing

†Fixed manufacturing overhead is applied on the basis of machine hours.

Upstate Mechanical’s annual requirement for these components is 8,000 units of T79 and 11,000 units of B81. Recently, management decided to devote additional machine time to other product lines, leaving only 41,000 machine hours per year for producing the bearings. An outside company has offered to sell Upstate Mechanical its annual supply of bearings at prices of $11.25 for T79 and $13.50 for B81. Management wants to schedule the otherwise idle 41,000 machine hours to produce bearings so that the firm can minimize costs (maximize net benefits).

Required:

- 1. Compute the net benefit (loss) per machine hour that would result if Upstate Mechanical accepts the supplier’s offer of $13.50 per unit for component B81.

- 2. Choose the correct answer. Upstate Mechanical will maximize its net benefits by:

- a. purchasing 4,800 units of T79 and manufacturing the remaining bearings.

- b. purchasing 8,000 units of T79 and manufacturing 11,000 units of B81.

- c. purchasing 11,000 units of B81 and manufacturing 8,000 units of T79.

- d. purchasing 4,000 units of B81 and manufacturing the remaining bearings.

- e. purchasing and manufacturing some amounts other than those given above.

- 3. Suppose management has decided to drop product T79. Independently of requirements (1) and (2), assume that the company’s idle capacity of 41,000 machine hours has a traceable, avoidable annual fixed cost of $44,000, which will be incurred only if the capacity is used. Calculate the maximum price Upstate Mechanical should pay a supplier for component B81.

Want to see the full answer?

Check out a sample textbook solution

Chapter 14 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

- Brees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for 66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows: Prior to making a decision, the companys CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following: 3 setups1,160 each (The setups would be avoided, and total spending could be reduced by 1,160 per setup.) One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is 12,300 and could be totally avoided if the part were purchased. Engineering work: 470 hours, 45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.) 75 fewer material moves at 30 per move. Required: 1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier. 2. Now, using the special study data, repeat the analysis. 3. Discuss the qualitative factors that would affect the decision, including strategic implications. 4. After reviewing the special study, the controller made the following remark: This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs? Is the controller right?arrow_forwardThe management of Wy Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity. The company's controller has provided an example to illustrate how this new system would work. In this example, the allocation base ismachine-hours and the estimated amount of the allocation base for the upcoming year is 50,000 machine-hours. In addition, capacity is 59,000 machine-hours and the actual level of activity for the year is 53,300 machine-hours. All of the manufacturing overhead is fixed and is P1,622,500 per year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the year as well as the manufacturing overhead at capacity. It is further assumed that this is also the actual amount of manufacturing overhead for the year. A number of products were worked on during the year, one of which was Product X. This product required 230 machine-hours. 20. If the company bases its predetermined overhead rate on the…arrow_forwardThe management of Wy Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity. The company's controller has provided an example to illustrate how this new system would work. In this example, the allocation base ismachine-hours and the estimated amount of the allocation base for the upcoming year is 50,000 machine-hours. In addition, capacity is 59,000 machine-hours and the actual level of activity for the year is 53,300 machine-hours. All of the manufacturing overhead is fixed and is P1,622,500 per year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the year as well as the manufacturing overhead at capacity. It is further assumed that this is also the actual amount of manufacturing overhead for the year. A number of products were worked on during the year, one of which was Product X. This product required 230 machine-hours. 22. If the company bases its predetermined overhead rate on the…arrow_forward

- The management of Wy Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity. The company's controller has provided an example to illustrate how this new system would work. In this example, the allocation base ismachine-hours and the estimated amount of the allocation base for the upcoming year is 50,000 machine-hours. In addition, capacity is 59,000 machine-hours and the actual level of activity for the year is 53,300 machine-hours. All of the manufacturing overhead is fixed and is P1,622,500 per year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the year as well as the manufacturing overhead at capacity. It is further assumed that this is also the actual amount of manufacturing overhead for the year. A number of products were worked on during the year, one of which was Product X. This product required 230 machine-hours. 21. If the company bases its predetermined overhead rate on the…arrow_forwardLine Company has the following information related to its production. Use the information below to answer the required questions. Line is in the business of producing fishing line. Line allocates overhead by the use of machine hours. Variable overhead consists of $50,000 of indirect labor and $15,000 in indirect materials and plans on using 130,000 total hours of machine hours. The line machine is expected to use 12,500 machine hours. At the end of the period, Line finds that they have used 12,000 machine hours with a variable overhead rate of $0.51. REQUIRED: 1) What is the Total Variance in the MOH for the Line? 2) What is the Overhead Rate Variance in the MOH costs? 3) What is the Efficiency Variance in the MOH costs? DO NOT GIVE ASNWER IN IMAGE FORMATarrow_forwardAcklin Company has two products: A and B. The annual production and sales of Product A is 600 units and of Product B is 900 units. The company has traditionally used direct labor-hours as the basis for applying all manufacturing overhead to products. Product A requires 0.5 direct labor-hours per unit and Product B requires 0.3 direct labor-hours per unit. The total estimated overhead for next period is $63,322. The company is considering switching to an activity-based costing system for the purpose of computing unit product costs for external reports. The new activity-based costing system would have three overhead activity cost pools--Activity 1, Activity 2, and General Factory--with estimated overhead costs and expected activity as follows: Activity Cost Pool Est Ovhd Cost Expected Acty - Prod A Expected Acty -Prod B Total Activity 1 $ 18,900 700 200 900 Activity 2 $ 15,631 1,000 100 1,100 General Factory $ 28,791 300 270 570 Total $ 63,322 The overhead cost per…arrow_forward

- Ellis Equipment (EE), manufactures three models of lawn tractor: EE-1000, EE-1800, and EE-2800. Because of the different materials used, production processes for each model differ significantly in terms of machine types and time requirements. Once parts are produced, however, assembly time per unit required for each type of tractor is similar. For this reason, EE allocates overhead on the basis of machine-hours. Last quarter, the company shipped 8,000 EE-1000s, 3,200 EE-1800s, and 800 EE-2800s. The revenues and expenses for the last quarter were as follows: ELLIS EQUIPMENT Income Statement For the Quarter Ended June 30 EE-1000 EE-1800 EE-2800 Total Sales revenue $ 12,800,000 $ 8,000,000 $ 3,520,000 $ 24,320,000 Direct costs Direct materials 4,800,000 3,200,000 1,120,000 9,120,000 Direct labor 1,680,000 768,000 230,400 2,678,400 Variable overhead Setting up machines 1,400,000 Quality testing 1,800,000 Painting 780,000…arrow_forwardAcklin Company has two products: A and B. The annual production and sales of Product A is 600 units and of Product B is 900 units. The company has traditionally used direct labor-hours as the basis for applying all manufacturing overhead to products. Product A requires 0.5 direct labor-hours per unit and Product B requires 0.3 direct labor-hours per unit. The total estimated overhead for next period is $63,322. The company is considering switching to an activity-based costing system for the purpose of computing unit product costs for external reports. The new activity-based costing system would have three overhead activity cost pools--Activity 1, Activity 2, and General Factory--with estimated overhead costs and expected activity as follows: Activity Cost Pool Est Ovhd Cost Expected Acty - Prod A Expected Acty -Prod B Total Activity 1 $ 18,900 700 200 900 Activity 2 $ 15,631 1,000 100 1,100 General Factory $ 28,791 300 270 570 Total $ 63,322 The predetermined…arrow_forwardAcklin Company has two products: A and B. The annual production and sales of Product A is 600 units and of Product B is 900 units. The company has traditionally used direct labor-hours as the basis for applying all manufacturing overhead to products. Product A requires 0.5 direct labor-hours per unit and Product B requires 0.3 direct labor-hours per unit. The total estimated overhead for next period is $63,322. The company is considering switching to an activity-based costing system for the purpose of computing unit product costs for external reports. The new activitybased costing system would have three overhead activity cost pools--Activity 1, Activity 2, and General Factory--with estimated overhead costs and expected activity as follows: Estimated Overhead Activity Cost pool Costs Expected Activity Product A…arrow_forward

- Acklin Company has two products: A and B. The annual production and sales of Product A is 600 units and of Product B is 900 units. The company has traditionally used direct labor-hours as the basis for applying all manufacturing overhead to products. Product A requires 0.5 direct labor-hours per unit and Product B requires 0.3 direct labor-hours per unit. The total estimated overhead for next period is $63,322. The company is considering switching to an activity-based costing system for the purpose of computing unit product costs for external reports. The new activity-based costing system would have three overhead activity cost pools--Activity 1, Activity 2, and General Factory--with estimated overhead costs and expected activity as follows: Activity Cost Pool Est Ovhd Cost Expected Acty - Prod A Expected Acty -Prod B Total Activity 1 $ 18,900 700 200 900 Activity 2 $ 15,631 1,000 100 1,100 General Factory $ 28,791 300 270 570 Total $ 63,322 The overhead cost per…arrow_forwardAcklin Company has two products: A and B. The annual production and sales of Product A is 600 units and of Product B is 900 units. The company has traditionally used direct labor-hours as the basis for applying all manufacturing overhead to products. Product A requires 0.5 direct labor-hours per unit and Product B requires 0.3 direct labor-hours per unit. The total estimated overhead for next period is $63,322. The company is considering switching to an activity-based costing system for the purpose of computing unit product costs for external reports. The new activity-based costing system would have three overhead activity cost pools--Activity 1, Activity 2, and General Factory--with estimated overhead costs and expected activity as follows: Activity Cost Pool Est Ovhd Cost Expected Acty - Prod A Expected Acty -Prod B Total Activity 1 $ 18,900 700 200 900 Activity 2 $ 15,631 1,000 100 1,100 General Factory $ 28,791 300 270 570 Total $ 63,322 The predetermined…arrow_forwardA company manufactures two products, Drills and Saws. Their total estimated overhead cost forthe year is $1,044,000 and expected labor hours are 72,600 hours; 32,600 for drills and 40,000for saws. The company is considering using ABC for applying overhead to their products, instead of asingle traditional overhead rate. They have broken down their overhead costs into the followingcost pools and cost drivers.arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning