Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:d. DN

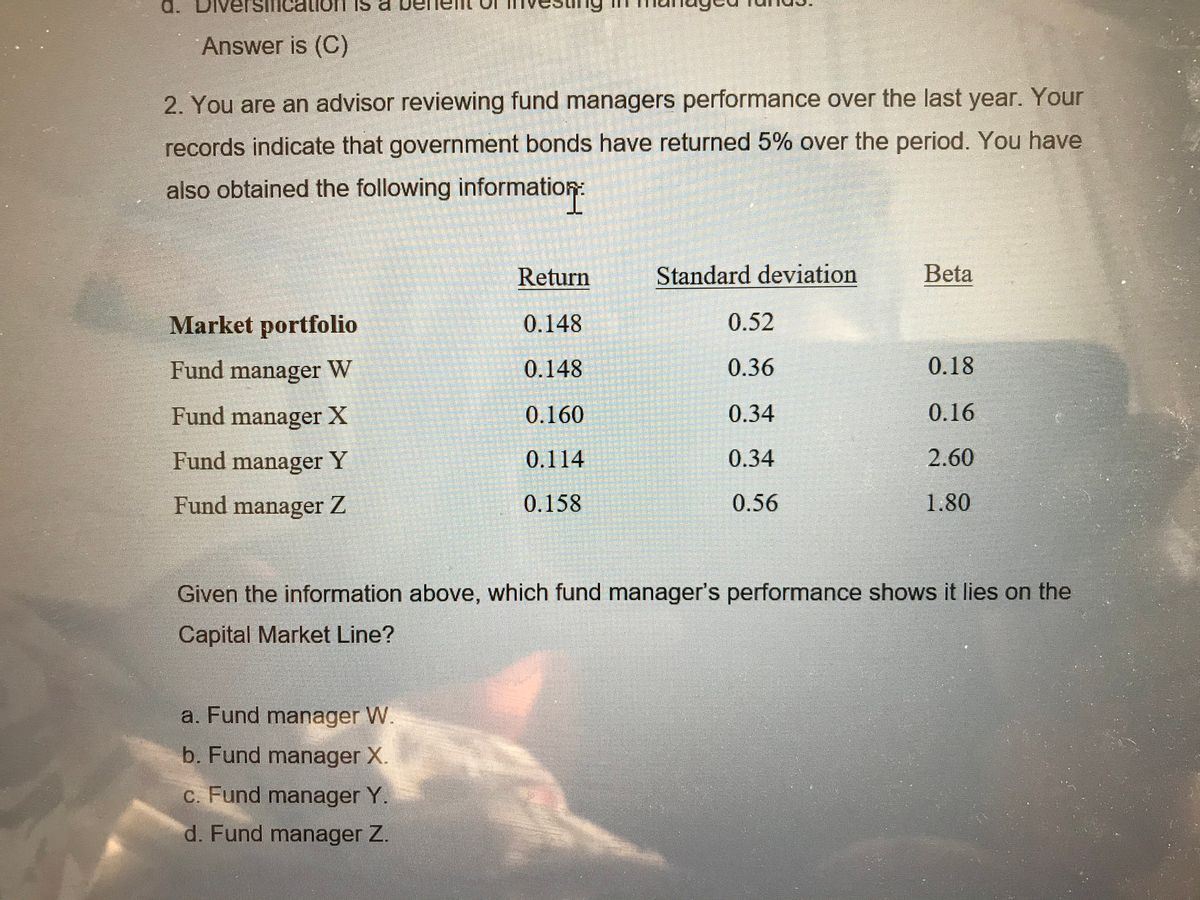

Answer is (C)

2. You are an advisor reviewing fund managers performance over the last year. Your

records indicate that government bonds have returned 5% over the period. You have

also obtained the following information:

Return

Standard deviation

Beta

Market portfolio

0.148

0.52

Fund manager W

0.148

0.36

0.18

Fund manager X

0.160

0.34

0.16

Fund manager Y

0.114

0.34

2.60

Fund manager Z

0.158

0.56

1.80

Given the information above, which fund manager's performance shows it lies on the

Capital Market Line?

a. Fund manager W.

b. Fund manager X.

c. Fund manager Y.

d. Fund manager Z.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You invested $90,000 in a mutual fund at the beginning of the year when the NAV was $54.3. At the end of the year, the fund paid $.40 in short-term distributions and $.57 in long-term distributions. If the NAV of the fund at the end of the year was $63.94, what was your return for the year? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.)arrow_forwardNonearrow_forward7. Impacts of Costs on Returns. A mutual fund has a 1.6% expense ratio and begins with a $124.655 NAV. It experiences the annual returns shown below. What are the end-of-year NAVS after fees for each year? What are the after-fee returns each year? (LO 4-4) Money to Invest NAV Expense ratio Year 1 return Year 2 return Year 3 return Year 4 return Year 5 return $ 10,000.00 $ 124.655 1.6% 5% -12% 18% 4% 23%arrow_forward

- Mr. Ota is an analyst for a large pension fund and he has been assigned the task of evaluating two different external portfolio managers (K and C). He considers the following historical average return, standard deviation, and CAPM beta estimates for these two managers over the past five years: Actual Average Standard deviation Portfolio Beta Return Manager K Manager C 7.80% 10.05% 0.75 12.0% 15.50% 1.45 Additionally, Mr. Ota estimate for the risk premium for the market portfolio is 5.40% and the risk-free rate is currently 2.50%. a. For both Managers K and C, calculate the expected return using the CAPM. Express your answers to the nearest basis point (i.e., xX.XX%)arrow_forwardThe days to maturity for a sample of five money market funds are shown here. The dollar amounts invested in the funds are provided. Days to Maturity Dollar Value ($ millions) 17 15 13 6 5 4 10 25 15 10 Use the weighted mean to determine the mean number of days to maturity for dollars invested in these five money market funds. Round your answer to 2 decimal places. x = daysarrow_forward17. Average Return and Standard Deviation. In a recent five-year period, mutual fund manager Diana Sauros produced the following percentage rates of return for the Mesozoic Fund. Rates of return on the market index are given for comparison. Calculate (a) the average return on both the fund and the index and (b) the standard deviation of the returns on each. Did Ms. Sauros do better or worse than the market index on these measures? (LO11-3) Fund Market index 1 -1.2 -0.9 2 +24.8 +16.0 3 +40.7 +31.7 4 +11.1 +10.9 5 +0.3 -0.7arrow_forward

- You are the manager of the Mighty Fine mutual fund. The following table reflects the activity of the fund during the last quarter. The fund started the quarter on January 1 with a balance of $60 million. Mighty Fine Mutual Fund Monthly Data (measured at end of month) January February March Net inflows ($ million ) 4.3 -5.3 0 HPR (%) -1.90 5.60 4.80 Required: a. Calculate the quarterly arithmetic average return on the fund. (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. Calculate the quarterly geometric (time - weighted) average return on the fund. (Do not round intermediate calculations. Round your answer to 2 decimal places.) c. Calculate the quarterly dollar-weighted average return on the fund. (Do not round intermediate calculations. Round your answer to 2 decimal places.)arrow_forwardInvestor has had the following returns in the Magic Fund for the past 4 years: 15%, 25%, -30%, 18%. c) State whether the annual geometric return (assume positive) should be higher, lower, or the same as the annual arithmetic return. Neither calculation nor explanation is necessary. d) State which measure, annual arithmetic return or annual geometric return, better represents how an investment performed over time. Neither calculation nor explanation is necessary.arrow_forwardes Required information [The following information applies to the questions displayed below.] A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) 15% 9% Bond fund (B) The correlation between the fund returns is 0.15. Expected Return Expected return Standard deviation Required: What is the expected return and standard deviation for the minimum-variance portfolio of the two risky funds? (Do not round intermediate calculations. Round your answers to 2 decimal places.) % % Standard Deviation 32% 23%arrow_forward

- Part C: What is the standard deviation of the 10 years of returns?arrow_forwardsign Layout References Mailings Review Help el me what View RCM Acrobat Foxit Reader PDF Foxit 2. You are an advisor reviewing fund managers performance over the last year. Your records indicate that government bonds have returned 5% over the period. You have also obtained the following information: Return Standard deviation Beta Market portfolio 0.148 0.52 Fund manager W 0.148 0.36 0.18 Fund manager X 0.160 0.34 0.16 Fund manager Y 0.114 0.34 2.60 Fund manager Z 0.158 0.56 1.80 Given the information above, which fund manager's performance shows it lies on the Capital Market Line? a. Fund manager W. b. Fund manager X. c. Fund manager Y. d. Fund manager Z.arrow_forwardYou are an analyst for a large public pension fund and you have been assigned the task of evaluating two different external portfolio managers (Yellen and Zagami) who (actively) manage two funds which are considering. Your associates have assembled the following historical average return, standard deviation, and CAPM beta estimates for these two fund managers over the past five years. In addition, you have estimated that the risk premium for the market portfolio is 5.12% and the risk-free rate is currently 4.14%. What is Ms. Yellen's average "alpha" for the period. Report your answer in percentage format rounded to three decimal places. (For example.1234 should be entered as "12.3"). Fund Manager Actual Avg. Return Standard Deviation Ms. Yellen 11% Mr. Zagami 8.24% Answer: 11.07 8.75% Beta 1.18 0.9arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education