PRIN.OF CORPORATE FINANCE

13th Edition

ISBN: 9781260013900

Author: BREALEY

Publisher: RENT MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 7, Problem 7PS

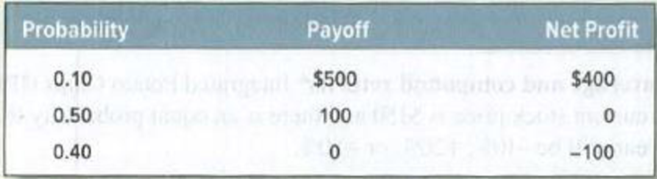

Expected return and standard deviation A game of chance offers the following odds and payoffs. Each play of the game costs $100, so the net profit per play is the payoff less $100.

What are the expected cash payoff and expected

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Consider an investment with the following probability distribution:

Probability:

Payoff:

0.40

41.0%

0.40

-6.0

0.20

-20.0

Calculate the expected return. Do not round intermediate calculations. Round your answer to two decimal places. _____%

Calculate the standard deviation. Do not round intermediate calculations. Round your answer to two decimal places. _____%

Calculate the coefficient of variation. Do not round intermediate calculations. Round your answer to two decimal places. _____

A game of chance offers the following odds and payoffs. Each play of the game costs $200, so the net profit per play is the payoff less $200.

Probability

Payoff

Net Profit

0.10

$700

$500

0.50

300

100

0.40

0

–200

a-1. What is the expected cash payoff? (Round your answer to the nearest whole dollar amount.)

a-2. What is the expected rate of return? (Enter your answer as a percent rounded to the nearest whole number.)

b-1. What is the variance of the expected returns? (In the calculation, use the percentage values, not the decimal values for the rates of return. Do not round intermediate calculations. Round your answer to the nearest whole number.)

b-2. What is the standard deviation of the expected returns? (Enter your answer as a percent rounded to 2 decimal places.)

A game of chance offers the following odds and payoffs. Each play of the game costs $200, so the net profit per play is the payoff less $200.

Probability

Payoff

Net Profit

0.30

$400

$200

0.60

300

100

0.10

0

–200

1. What is the expected cash payoff?

Note: Round your answer to the nearest whole dollar amount.

2. What is the expected rate of return?

Note: Enter your answer as a percent rounded to the nearest whole number.

1.What is the variance of the expected returns?

Note: In the calculation, use the percentage values, not the decimal values for the rates of return. Do not round intermediate calculations. Round your answer to the nearest whole number.

2.hat is the standard deviation of the expected returns?

Note: Enter your answer as a percent rounded to 2 decimal places.

Chapter 7 Solutions

PRIN.OF CORPORATE FINANCE

Ch. 7 - Rate of return The level of the Syldavia market...Ch. 7 - Real versus nominal returns The Costaguana stock...Ch. 7 - Arithmetic average and compound returns Integrated...Ch. 7 - Risk premiums Here are inflation rates and U.S....Ch. 7 - Risk Premium Suppose that in year 2030, investors...Ch. 7 - Stocks vs. bonds Each of the following statements...Ch. 7 - Expected return and standard deviation A game of...Ch. 7 - Standard deviation of returns The following table...Ch. 7 - Average returns and standard deviation During the...Ch. 7 - Prob. 10PS

Ch. 7 - Prob. 11PSCh. 7 - Diversification Here are the percentage returns on...Ch. 7 - Risk and diversification In which of the following...Ch. 7 - Prob. 14PSCh. 7 - Portfolio risk To calculate the variance of a...Ch. 7 - Portfolio risk a) How many variance terms and how...Ch. 7 - Portfolio risk Table 7.8 shows standard deviations...Ch. 7 - Portfolio risk Hyacinth Macaw invests 60% of her...Ch. 7 - Stock betas What is the beta of each of the stocks...Ch. 7 - Stock betas There are few, if any, real companies...Ch. 7 - Portfolio betas A portfolio contains equal...Ch. 7 - Portfolio betas Suppose the standard deviation of...Ch. 7 - Portfolio risk Here are some historical data on...Ch. 7 - Portfolio risk Suppose that Treasury bills offer a...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Draw the indifference curve in the expected return–standard deviation plane corresponding to a utility level of .05 for an investor with a risk aversion coefficient of 3. (Hint: Choose several possible standard deviations, ranging from 0 to .25, and find the expected rates of return providing a utility level of .05. Then plot the expected return–standard deviation points so derived.)arrow_forwardCompute the (1) net present value, (2) profitability index, and (3) internal rate of return for each option. (Hint: To solve for internal rate of return, experiment with alternative discount rates to arrive at a net present value of zero.) (If the net present value is negative, use either a negative sign preceding the number eg -45 or parentheses eg (45). Round answers for present value and IRR to 0 decimal places, e.g. 125 and round profitability index to 2 decimal places, e.g. 12.50. For calculation purposes, use 5 decimal places as displayed in the factor table provided.) Option A Option B $ $ LA Net Present Value Profitability Index Internal Rate of Return % %arrow_forwardOn the basis of the utility formula below, which investment would you select if you were risk averse with A = 4? Investment Expected return E(r) Standard deviation σ 1 0.12 0.30 2 0.15 0.50 3 0.21 0.16 4 0.24 0.21arrow_forward

- An investor wants to follow a spread strategy by buying a put for 6$ with a strike price of 95$ and writing a put for 4$ with a strike price of 90$. a. Draw the graph of strategy payoffs and profits b. Find the equilibrium price of this strategy (the equilibrium price is the market price of the stock where the profit is 0) c. What is the maximum profit and loss from this strategy?arrow_forwardSuppose the nominal rate of return is 0.085 and the risk-free rate is 0.010. What is the risk premium? Instruction: Round to two decimal places. E.g., if your answer is 0.0106465 or 1.06465%, you should type ONLY the number .01, neither 0.0106465, 0.0106, nor 1.065. Otherwise, Blackboard will treat it as a wrong answer.arrow_forwarda. What is the market risk premium (M-FRF)? Round your answer to two decimal places. % b. What is the beta of Fund P? Do not round intermediate calculations. Round your answer to two decimal places. c. What is the required return of Fund P? Do not round intermediate calculations. Round your answer to two decimal places. % d. Would you expect the standard deviation of Fund P to be less than 14%, equal to 14%, or greater than 14%? I. less than 14% II. greater than 14% III. equal to 14%arrow_forward

- Which one of the following statements is correct? Multiple Choice The risk-free rate of return has a risk premium of 1.0. The reward for bearing risk is called the standard deviation. Risks and expected return are inversely related. The higher the expected rate of return, the wider the distribution of returns. Risk premiums are inversely related to the standard deviation of returns.arrow_forwardAssume the standard deviation of the market return is 0.2, the standard deviation of asset k is 0.45 and the beta of asset k is 0.675. The correlation coefficient between the return from asset k and the return from the market is: A. 0.473 OB. 0.900 OC. No answer OD. 0.290arrow_forwardSuppose you want to establish a bullish spread strategy. The are two call options. The first one has X1=$50 and C1=$5. The second one has X2=$42 and C2=$6. When the underlying asset price is S(t)=$45, what is the profit from the strategy? What is the maximum profit of the strategy? What is the minimum payoff of the strategy?arrow_forward

- Three decision makers have assessed utilities for the following decision problem (payoff in dollars): The indifference probabilities are as follows: Plot the utility function for money for each decision maker. Classify each decision maker as a risk avoider, a risk taker, or risk-neutral. For the payoff of 20, what is the premium that the risk avoider will pay to avoid risk? What is the premium that the risk taker will pay to have the opportunity of the high payoff?arrow_forwarda) Discuss the difference between a price-weighted index and a value-weighted index. Give one example for the price-weighted index and one example for the value-weighted index and discuss any problems/advantages associated with the specific indices. b) We assume that investors use mean-variance utility: U = E(r) – 0.5 × Ao², where E(r) is the expected return, A is the risk aversion coefficient and o? is the variance of returns. Given that the optimal proportion of the risky asset in the complete port- folio is given by the equation y* = E , where r; is the risk-free rate, E(rp) is the expected returm of the risky portfolio, o, is variance of returns, and A is the risk aversion coefficient. For each of the variables on the right side of the equation, discuss the impact of the variable's effect on y* and why the nature of the relationship makes sense intuitively. Assume the investor is risk averse. Aoarrow_forwardAlternatives A C D E alternatives have the following returns and standard deviations of returns. Alternatives A B C D E Returns: Expected Value $ 1,460 1,370 10,300 1,180 67,600 Coefficient of Variation Standard Deviation Calculate the coefficient of variation and rank the five alternatives from the lowest risk to the highest risk by using the coefficient of variation. (Round your answers to 3 decimal places.) Rank $ 780 1,490 9,100 1,060 21,500 1469 47 meldarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...

Statistics

ISBN:9781305627734

Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:Cengage Learning

Portfolio return, variance, standard deviation; Author: MyFinanceTeacher;https://www.youtube.com/watch?v=RWT0kx36vZE;License: Standard YouTube License, CC-BY