Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

6th Edition

ISBN: 9780134486857

Author: Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 19, Problem 44BP

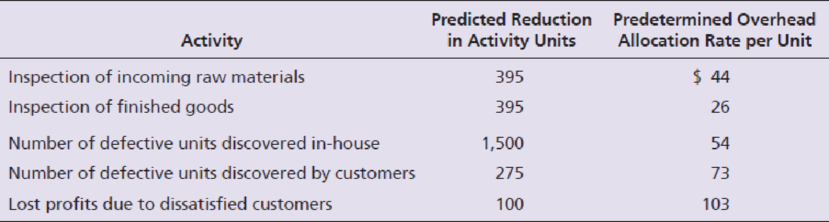

Roxi, Inc. is using a costs-of-quality approach to evaluate design engineering efforts for a new skateboard. Roxi’s senior managers expect the engineering work to reduce appraisal, internal failure, and external failure activities. The predicted reductions in activities over the two-year life of the skateboards follow. Also shown are the predetermined

Requirements

- 1. Calculate the predicted quality cost savings from the design engineering work.

- 2. Roxi spent $106,000 on design engineering for the new skateboard. What is the net benefit of this “preventive” quality activity?

- 3. What major difficulty would Roxi’s managers have in implementing this costs-of-quality approach? What alternative approach could they use to measure quality improvement?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Analyzing costs of quality

Stella, Inc. is using, a costs-of-quality approach to evaluate design engineering efforts for a new skateboard. Stella’s senior managers expect the engineering work to reduce appraisal, internal failure and external failure activities. The predicted reductions in activities over the two-year life of the skateboards follow. Also shown are the predeter—mined overhead allocation rates for each activity.

Requirements

Calculate the predicted quality cost savings from the design engineering Work.

Stella spent $103,000 on design engineering for the new skateboard. What is the net benefit of this “preventive” quality activity?

What major difficulty would Stella’s managers have in implementing this costs-of-quality approach? What alternative approach could they use to measure quality improvement?

Robotic Construction Toys Corp. is using a costs-of-quality approach to evaluate design engineering efforts for a new toy robot. The company's senior

managers expect the engineering work to reduce appraisal, internal failure, and external failure activities. The predicted reductions in activities over

the two-year life of the toy robot follow. Also shown are the cost allocation rates for the activities.

(Click on the icon to view the information.)

Data table

Activity

Inspection of incoming materials

Inspection of finished goods....

Number of defective units discovered in-house.

Number of defective units discovered by customers..

Lost sales to dissatisfied customers

Requirements

......

****

Predicted

Reduction in

Activity Units

3. What major difficulty would management have had in implementing

this costs-of-quality approach? What alternative approach could it use to

measure quality improvement?

300 $

300 $

3,200 $

900 $

320 $

-

1. Calculate the predicted quality cost savings from the…

Kagle design engineers are in the process of developing a new “green” product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed $550 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit- and activity-based accounting information (made possible by a recent pilot study producing the activity-based data).

Unit-based system:Variable conversion activity rate: $100 per direct labor hourMaterial usage rate: $20 per partABC system:Labor usage: $15 per direct labor hourMaterial usage (direct materials): $20 per partMachining: $75 per machine hourPurchasing activity: $150 per purchase orderSetup activity: $3,000 per setup hourWarranty…

Chapter 19 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Ch. 19 - The Santos Shirt Company manufactures shirts in...Ch. 19 - Prob. 2TICh. 19 - Prob. 3TICh. 19 - Prob. 4TICh. 19 - Prob. 5TICh. 19 - Prob. 6TICh. 19 - Prob. 7TICh. 19 - Prob. 8TICh. 19 - Prob. 9TICh. 19 - Prob. 10TI

Ch. 19 - Prob. 11TICh. 19 - Prob. 12TICh. 19 - Which statement is false? a. Using a single...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It can use ABC information for what...Ch. 19 - Prob. 6QCCh. 19 - Companies enjoy many benefits from using JIT....Ch. 19 - Which account is not used in JIT costing? a....Ch. 19 - The cost of lost future sales after a customer...Ch. 19 - Spending on testing a product before shipment to...Ch. 19 - What is the formula to compute the predetermined...Ch. 19 - How is the predetermined overhead allocation rate...Ch. 19 - Describe how a single plantwide overhead...Ch. 19 - Why is using a single plantwide overhead...Ch. 19 - Why is the use of departmental overhead allocation...Ch. 19 - What is activity-based management? How is it...Ch. 19 - How many cost pools are in an activity-based...Ch. 19 - What are the four steps to developing an...Ch. 19 - Why is ABC usually considered more accurate than...Ch. 19 - List two ways managers can use ABM to make...Ch. 19 - Define value engineering. How is it used to...Ch. 19 - Explain the difference between target price and...Ch. 19 - How can ABM be used by service companies?Ch. 19 - What is a just-in-time management system?Ch. 19 - Explain how the work cell manufacturing layout...Ch. 19 - What are the inventory accounts used in JIT...Ch. 19 - How is the Conversion Costs account used in JIT...Ch. 19 - Prob. 18RQCh. 19 - Which accounts are adjusted for the underallocated...Ch. 19 - Prob. 20RQCh. 19 - Prob. 21RQCh. 19 - Prevention is much cheaper than external failure....Ch. 19 - What are quality improvement programs?Ch. 19 - Prob. 24RQCh. 19 - Prob. 1SECh. 19 - The Oakman (Company (see Short Exercise S19-1) has...Ch. 19 - Activity-based costing requires four steps. List...Ch. 19 - Prob. 4SECh. 19 - Darby Corp. is considering the use of...Ch. 19 - The following information is provided for Orbit...Ch. 19 - Jaunkas Corp. manufactures mid-fi and hi-fi stereo...Ch. 19 - Spectrum Corp. makes two products: C and D. The...Ch. 19 - Refer to Short Exercise S19-8. Spectrum Corp....Ch. 19 - Haworth Company is a management consulting firm....Ch. 19 - Refer to Short Exercise S19-10. Haworth desires a...Ch. 19 - Prob. 12SECh. 19 - Prime Products uses a JIT management system to...Ch. 19 - Stegall, Inc. manufactures motor scooters. For...Ch. 19 - Koehler makes handheld calculators in two models:...Ch. 19 - Koehler (see Exercise E19-15) makes handheld...Ch. 19 - Koehler (see Exercise E19-15 and Exercise E19-16)...Ch. 19 - Franklin, Inc. uses activity-based costing to...Ch. 19 - Turbo Champs Corp. uses activity-based costing to...Ch. 19 - Eason Company manufactures wheel rims. The...Ch. 19 - Refer to Exercise E19-20. For 2019, Easons...Ch. 19 - Refer to Exercises E19-20 and E19-21. Controller...Ch. 19 - Treat Dog Collars uses activity-based costing....Ch. 19 - Western, Inc. is a technology consulting firm...Ch. 19 - Refer to Exercise E19-24. The president of Western...Ch. 19 - Prob. 26ECh. 19 - Refer to Exercise E19-26. Western desires a 20%...Ch. 19 - Lally, Inc. produces universal remote controls....Ch. 19 - Prob. 29ECh. 19 - Darrel Co. makes electronic components. Chris...Ch. 19 - Prob. 31ECh. 19 - Prob. 32ECh. 19 - Willitte Pharmaceuticals manufactures an...Ch. 19 - The Alright Manufacturing Company in Rochester,...Ch. 19 - Oscar, Inc. manufactures bookcases and uses an...Ch. 19 - Blanchette Plant Service completed a special...Ch. 19 - Low Range produces fleece jackets. The company...Ch. 19 - Stella, Inc. is using a costs-of-quality approach...Ch. 19 - Harcourt Pharmaceuticals manufactures an...Ch. 19 - The Alexander Manufacturing Company in Rochester,...Ch. 19 - Martin, Inc. manufactures bookcases and uses an...Ch. 19 - Rennie Plant Service completed a special...Ch. 19 - High Mountain produces fleece jackets. The company...Ch. 19 - Roxi, Inc. is using a costs-of-quality approach to...Ch. 19 - Download an Excel template for this problem online...Ch. 19 - This problem continues the Piedmont Computer...Ch. 19 - Prob. 1TIATCCh. 19 - Harris Systems specializes in servers for...Ch. 19 - Harris Systems has decided to adopt ABC. To remain...Ch. 19 - Prob. 1EICh. 19 - Anu Ghai was a new production analyst at RHI,...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Toledo Tool Company plans to introduce a new product. The company also considers adopting a new computer-assisted manufacturing system. The new product can be manufactured by either the new computer assisted system or its traditional labor-intensive production system. The company can achieve the same quality of the product regardless of which the production system employed. The estimated product costs by the two production systems are as follows: Traditional Labor-Intensive Production Systems New Computer-Assisted Manufacturing Systems Direct Material (per unit) $10.5 $8.4 Direct Labor (per unit) $14.0 $9.0 Variable overhead (per unit) $5.5 $3.4 Fixed overhead $2M $3.5M The marketing department recommends that the unit selling price of the new product be at $65, and the company expects the selling expenses for the new product to be $830,000 annually plus $4 for each unit sold. The company is currently subject to a 40% income tax rate.…arrow_forwardClarke, Inc. manufactures door panels. Suppose Clarke, Inc. is considering spending the following amounts on a new total quality management (TQM) program: View the spending amounts. Clarke, Inc. expects the new program would save costs through the following: View the savings amounts. Requirements 1. Classify each cost as a prevention cost, an appraisal cost, an internal failure cost, or an external failure cost. 2. Should Clarke, Inc. implement the new quality program? Give your reason. Requirement 1. Classify each cost as a prevention cost, an appraisal cost, an internal failure cost, or an external failure cost. Type of Cost Strength-testing one item from each batch of panels Training employees in TQM Training suppliers in TQM Identifying suppliers who commit to on-time delivery of perfect-quality materials Lost profits from lost sales due to disappointed customers Rework and spoilage Inspection of raw materials Warranty costs Savings Avoid lost profits from lost sales due to…arrow_forwardKagle design engineers are in the process of developing a new green product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed 550 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit-and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system: Variable conversion activity rate: 100 per direct labor hour Material usage rate: 20 per part ABC system: Labor usage: 15 per direct labor hour Material usage (direct materials): 20 per part Machining: 75 per machine hour Purchasing activity: 150 per purchase order Setup activity: 3,000 per setup hour Warranty activity: 500 per returned unit (usually requires extensive rework) Customer repair cost: 25 per repair hour (average) Required: 1. Select the lower-cost design using unit-based costing. Are logistical and post-purchase activities considered in this analysis? 2. Select the lower-cost design using ABC analysis. Explain why the analysis differs from the unit-based analysis. 3. What if the post-purchase cost was an environmental contaminant and amounted to 10 per unit for Design A and 40 per unit for Design B? Assume that the environmental cost is borne by society. Now which is the better design?arrow_forward

- Silven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardJohnson Filtration. Inc., provides maintenance service for water filtration systems throughout southern Florida. Customers contact Johnson with requests for maintenance service on their water filtration systems. To estimate the service time and the service cost. Johnson’s managers want to predict the repair time necessary for each maintenance request. Hence, repair time in hours is the dependent variable. Repair time is believed to be related to three factors: the number of months since the last maintenance service, the type of repair problem (mechanical or electrical), and the repairperson who performs the repair (Donna Newton or Bob Jones). Data for a sample of 10 service calls are reported in the following table: Develop the simple linear regression equation to predict repair time given the number of months since the last maintenance service, and use the results to test the hypothesis that no relationship exists between repair time and the number of months since the last maintenance service at the 0.05 level of significance. What is the interpretation of this relationship? What does the coefficient of determination tell you about this model? Using the simple linear regression model developed in part (a), calculate the predicted repair time and residual for each of the 10 repairs in the data. Sort the data in ascending order by value of the residual. Do you see any pattern in the residuals for the two types of repair? Do you see any pattern in the residuals for the two repairpersons? Do these results suggest any potential modifications to your simple linear regression model? Now create a scatter chart with months since last service on the x-axis and repair time in hours on the y-axis for which the points representing electrical and mechanical repairs are shown in different shapes and/or colors. Create a similar scatter chart of months since last service and repair time in hours for which the points representing repairs by Bob Jones and Donna Newton are shown in different shapes and/or colors. Do these charts and the results of your residual analysis suggest the same potential modifications to your simple linear regression model? Create a new dummy variable that is equal to zero if the type of repair is mechanical and one if the type of repair is electrical. Develop the multiple regression equation to predict repair time, given the number of months since the last maintenance service and the type of repair. What are the interpretations of the estimated regression parameters? What does the coefficient of determination tell you about this model? Create a new dummy variable that is equal to zero if the repairperson is Bob Jones and one if the repairperson is Donna Newton. Develop the multiple regression equation to predict repair time, given the number of months since the last maintenance service and the repairperson. What are the interpretations of the estimated regression parameters? What does the coefficient of determination tell you about this model? Develop the multiple regression equation to predict repair time, given the number of months since the last maintenance service, the type of repair, and the repairperson. What are the interpretations of the estimated regression parameters? What does the coefficient of determination tell you about this model? Which of these models would you use? Why?arrow_forward

- Jolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was 20 per unit. The following cost formula was developed: Y=200,000+10X1 where X1=Machinehours(Theproductisexpectedtouseonemachinehourforeveryunitproduced.) Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be 50,000. This produced a gross profit of 2 per unit, well below the targeted gross profit of 4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least 50,000 so that the target profit could be met. Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from 10 per machine hour to 8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controllers cost formula. He suggested a more careful assessment of the proposed designs effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z). Y=140,000+8X1+5,000X2+2,000X3 where X1=MachinehoursX2=NumberofbatchesX3=Numberofengineeringchangeorders Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the products life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders. This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by 2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from 5,000 to 3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by 40,000, reducing the fixed cost component in the equation by this amount. Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated 0.70 per unit sold to 0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease). Required: 1. Calculate the expected gross profit per unit for Design Z using the controllers original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineers revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management? 2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management. 3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?arrow_forwardBumblebee Mobiles manufactures a line of cell phones. The management has identified the following overhead costs and related cost drivers for the coming year. The following were incurred in manufacturing two of their cell phones, Bubble and Burst, during the first quarter. REQUIREMENT Review the worksheet called ABC that follows these requirements. You have been asked to determine the cost of each product using an activity-based cost system. Note that the problem information is already entered into the Data Section of the ABC worksheet.arrow_forwardThe controller of Emery, Inc. has computed quality costs as a percentage of sales for the past 5 years (20X1 was the first year the company implemented a quality improvement program). This information is as follows: Required: 1. Prepare a trend graph for total quality costs. Comment on what the graph has to say about the success of the quality improvement program. 2. Prepare a graph that shows the trend for each quality cost category. What does the graph have to say about the success of the quality improvement program? Does this graph supply more insight than the total cost trend graph does? 3. Prepare a graph that compares the trend in relative control costs versus relative failure costs. Comment on the significance of this trend.arrow_forward

- Green Manufacturing is a traditional manufacturing company located in the midwestern United States. The company’s operations manager is developing a strategy to become more CSR-oriented. In an effort to evaluate possible areas where CSR initiatives can be implemented, the manager has gathered the following data regarding three potential CSR activities: Initialadded cost Variable cost Variable savings Recycle and reuse production material $5,000 $0.10 per lb. of recycled material $0.15 per lb. of recycled material Add solar panels as a source of power 700,000 $1,000 per year $33,000 per year Replace assembly room light fixtures with natural light 120,000 $180 per month $220 per month The recycling activity would carry on indefinitely. The solar panels would have a useful life of 30 years. The replacement of assembly room light fixtures with natural light is assumed to have an 80-year effect. a. Determine if it is viable to recycle and use…arrow_forwardGreen Manufacturing is a traditional manufacturing company located in the midwestern United States. The company's operations manager is developing a strategy to become more CSR-oriented. In an effort to evaluate possible areas where CSR initiatives can be implemented, the manager has gathered the following data regarding three potential CSR activities: Initial Added Cost Variable Cost Variable Savings Recycle and reuse production materials $ 5,000 $0.10 per lb. of recycled material $0.15 per lb. of recycled material Add solar panels as a source of power 700,000 $ 1,000 per year $ 33,000 per year Replace assembly room light fixtures with natural light 120,000 $ 180 per month $ 220 per month The recycling activity would carry on indefinitely. The solar panels would have a useful life of 30 years. The replacement of assembly room light fixtures with natural light is assumed to have an 80-year effect. a. Identify which CSR activities Green Manufacturing should…arrow_forwardGreen Manufacturing is a traditional manufacturing company located in the midwestern United States. The company's operations manager is developing a strategy to become more CSR-oriented. In an effort to evaluate possible areas where CSR initiatives can be implemented, the manager has gathered the following data regarding three potential CSR activities: Initial Added Cost Variable Cost Variable Savings Recycle and reuse production materials $ 5,000 $0.10 per lb. of recycled material $0.15 per lb. of recycled material Add solar panels as a source of power 700,000 $ 1,000 per year $ 33,000 per year Replace assembly room light fixtures with natural light 120,000 $ 180 per month $ 220 per month The recycling activity would carry on indefinitely. The solar panels would have a useful life of 30 years. The replacement of assembly room light fixtures with natural light is assumed to have an 80-year effect. a. Identify which CSR activities Green Manufacturing should…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...

Statistics

ISBN:9781305627734

Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Inspection and Quality control in Manufacturing. What is quality inspection?; Author: Educationleaves;https://www.youtube.com/watch?v=Ey4MqC7Kp7g;License: Standard youtube license