Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

6th Edition

ISBN: 9780134486857

Author: Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 19, Problem 6SE

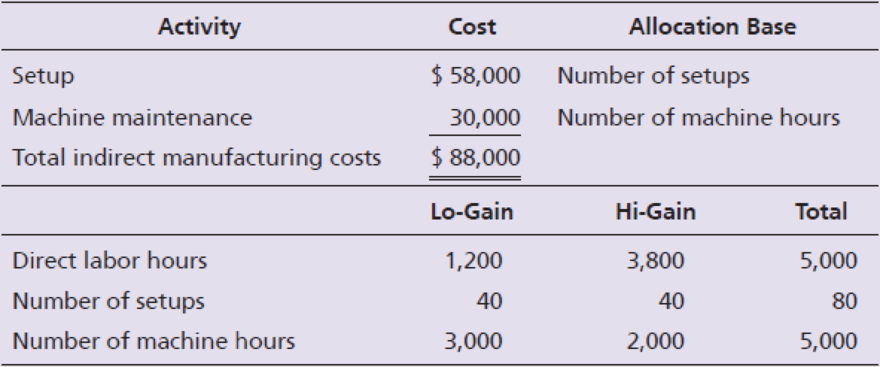

The following information is provided for Orbit Antenna Corp., which manufactures two products: Lo-Gain antennas and Hi-Gain antennas for use in remote areas.

Orbit Antenna plans to produce 125 Lo-Gain antennas and 225 Hi-Gain antennas.

Requirements

- 1. Compute the indirect

manufacturing cost per unit using direct labor hours for the single plant wide predeterminedoverhead allocation rate. - 2. Compute the ABC indirect manufacturing cost per unit for each product.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

SIMPly Power Inc., manufactures and sells two products: Product V9 and Product B1. Data concerning

the expected production of each product and the expected total direct labour-hours (DLHS) required to

produce that output appear below:

Product V9

Product B1

Total direct labour-hours

Product V9

Product B1

Activity Cost Pools

Labour-related

The direct labour rate is $27.40 per DLH. The direct materials cost per unit for each product is given

below:

Machine setups

General factory

Expected Production

300

The company is considering adopting an activity-based costing system with the following activity cost

pools, activity measures, and expected activity:

O $86.5 per unit

800

O $129.12 per unit

O $217.95 per unit

O $272.08 per unit

Activity Measures

DLHS

Direct Labour-Hours Per

Unit

5.0

3.0

setups

Direct Materials Cost per Unit

$176.90

$262.80

MHS

Estimated

Overhead Cost

$94,848

36,990

62,408

$194,246

Total Direct Labour-

Hours

1,500

2,400

3.900

Expected Activity

Product V9 Product B1 Total…

Vattes, Incorporated, manufactures and sells two products: Product 15 and Product U1. Data concerning the expected production of each product and the

expected total direct labor-hours (DLHs) required to produce that output appear below:

Product 15

Product U1

Direct

Labor-

Expected Hours Per

Production Unit

700

7.0

200

4.0

Activity Cost Pools

Labor-related

Machine setups

Order size

Product 15

Product U1

Total direct labor-hours

The direct labor rate is $22.00 per DLH. The direct materials cost per unit for each product is given below:

Direct

Materials

Cost per

Unit

$ 261.60

$ 121.60

Activity

Measures

DLHS

setups

MHS

The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity,

Expected Activity

Total

Direct

Labor-

Estimated

Overhead

Cost

$ 268,698

Hours

4,900

800

5,700

37,324

633,895

$939,917

Product 15 Product U1

4,900

300

4,900

800

400

4,800

Total

5,700

700

9,700

Casey Company has five activity cost pools and two products. It expects to

produce 200,000 units of its automobile scissors jack and 80,000 units of its truck

hydraulic jack. Having identified its activity cost pools and the cost drivers for

each cost pool, Casey Company accumulated the following data relative to those

activity cost pools and cost drivers.

Expected Use of

Cost Drivers per Product

Hydraulic

Jacks

Annual Overhead Data

Expected Use of Cost

Drivers per Activity

Estimated

Scissors

Activity Cost Pools

Ordering and receiving

Machine setup

Machining

Assembling

Inspecting and testing

Cost Drivers

Overhead

Jacks

$ 200,000

600,000

2,000,000

1,800,000

700,000

2,500 orders

1,200 setups

800,000 hours

1,500

700

500,000

1,200,000

15,000

Purchase orders

1,000

Setups

Machine hours

500

Parts

Tests

3,000,000 parts

35,000 tests

300,000

1,800,000

20,000

$5,300,000

Required: Using ABC Calculate Per Unit and Total cost of Both Products

also Comment?

Chapter 19 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Ch. 19 - The Santos Shirt Company manufactures shirts in...Ch. 19 - Prob. 2TICh. 19 - Prob. 3TICh. 19 - Prob. 4TICh. 19 - Prob. 5TICh. 19 - Prob. 6TICh. 19 - Prob. 7TICh. 19 - Prob. 8TICh. 19 - Prob. 9TICh. 19 - Prob. 10TI

Ch. 19 - Prob. 11TICh. 19 - Prob. 12TICh. 19 - Which statement is false? a. Using a single...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It can use ABC information for what...Ch. 19 - Prob. 6QCCh. 19 - Companies enjoy many benefits from using JIT....Ch. 19 - Which account is not used in JIT costing? a....Ch. 19 - The cost of lost future sales after a customer...Ch. 19 - Spending on testing a product before shipment to...Ch. 19 - What is the formula to compute the predetermined...Ch. 19 - How is the predetermined overhead allocation rate...Ch. 19 - Describe how a single plantwide overhead...Ch. 19 - Why is using a single plantwide overhead...Ch. 19 - Why is the use of departmental overhead allocation...Ch. 19 - What is activity-based management? How is it...Ch. 19 - How many cost pools are in an activity-based...Ch. 19 - What are the four steps to developing an...Ch. 19 - Why is ABC usually considered more accurate than...Ch. 19 - List two ways managers can use ABM to make...Ch. 19 - Define value engineering. How is it used to...Ch. 19 - Explain the difference between target price and...Ch. 19 - How can ABM be used by service companies?Ch. 19 - What is a just-in-time management system?Ch. 19 - Explain how the work cell manufacturing layout...Ch. 19 - What are the inventory accounts used in JIT...Ch. 19 - How is the Conversion Costs account used in JIT...Ch. 19 - Prob. 18RQCh. 19 - Which accounts are adjusted for the underallocated...Ch. 19 - Prob. 20RQCh. 19 - Prob. 21RQCh. 19 - Prevention is much cheaper than external failure....Ch. 19 - What are quality improvement programs?Ch. 19 - Prob. 24RQCh. 19 - Prob. 1SECh. 19 - The Oakman (Company (see Short Exercise S19-1) has...Ch. 19 - Activity-based costing requires four steps. List...Ch. 19 - Prob. 4SECh. 19 - Darby Corp. is considering the use of...Ch. 19 - The following information is provided for Orbit...Ch. 19 - Jaunkas Corp. manufactures mid-fi and hi-fi stereo...Ch. 19 - Spectrum Corp. makes two products: C and D. The...Ch. 19 - Refer to Short Exercise S19-8. Spectrum Corp....Ch. 19 - Haworth Company is a management consulting firm....Ch. 19 - Refer to Short Exercise S19-10. Haworth desires a...Ch. 19 - Prob. 12SECh. 19 - Prime Products uses a JIT management system to...Ch. 19 - Stegall, Inc. manufactures motor scooters. For...Ch. 19 - Koehler makes handheld calculators in two models:...Ch. 19 - Koehler (see Exercise E19-15) makes handheld...Ch. 19 - Koehler (see Exercise E19-15 and Exercise E19-16)...Ch. 19 - Franklin, Inc. uses activity-based costing to...Ch. 19 - Turbo Champs Corp. uses activity-based costing to...Ch. 19 - Eason Company manufactures wheel rims. The...Ch. 19 - Refer to Exercise E19-20. For 2019, Easons...Ch. 19 - Refer to Exercises E19-20 and E19-21. Controller...Ch. 19 - Treat Dog Collars uses activity-based costing....Ch. 19 - Western, Inc. is a technology consulting firm...Ch. 19 - Refer to Exercise E19-24. The president of Western...Ch. 19 - Prob. 26ECh. 19 - Refer to Exercise E19-26. Western desires a 20%...Ch. 19 - Lally, Inc. produces universal remote controls....Ch. 19 - Prob. 29ECh. 19 - Darrel Co. makes electronic components. Chris...Ch. 19 - Prob. 31ECh. 19 - Prob. 32ECh. 19 - Willitte Pharmaceuticals manufactures an...Ch. 19 - The Alright Manufacturing Company in Rochester,...Ch. 19 - Oscar, Inc. manufactures bookcases and uses an...Ch. 19 - Blanchette Plant Service completed a special...Ch. 19 - Low Range produces fleece jackets. The company...Ch. 19 - Stella, Inc. is using a costs-of-quality approach...Ch. 19 - Harcourt Pharmaceuticals manufactures an...Ch. 19 - The Alexander Manufacturing Company in Rochester,...Ch. 19 - Martin, Inc. manufactures bookcases and uses an...Ch. 19 - Rennie Plant Service completed a special...Ch. 19 - High Mountain produces fleece jackets. The company...Ch. 19 - Roxi, Inc. is using a costs-of-quality approach to...Ch. 19 - Download an Excel template for this problem online...Ch. 19 - This problem continues the Piedmont Computer...Ch. 19 - Prob. 1TIATCCh. 19 - Harris Systems specializes in servers for...Ch. 19 - Harris Systems has decided to adopt ABC. To remain...Ch. 19 - Prob. 1EICh. 19 - Anu Ghai was a new production analyst at RHI,...

Additional Business Textbook Solutions

Find more solutions based on key concepts

Analysis of inventory errors A2 Hallam Company’s financial statements show the following. The company recently ...

FINANCIAL ACCT.FUND.(LOOSELEAF)

For each of the following transactions, state which special journal (Sales Journal, Cash Receipts Journal, Cash...

Principles of Accounting Volume 1

This year, Prewer Inc. received a 160,000 dividend on its investment consisting of 16 percent of the outstandin...

PRINCIPLES OF TAXATION F/BUS.+INVEST.

1. For Frank’s Funky Sounds, straight-line depreciation on the trucks is a

Learning Objective 1

a. variable cos...

Horngren's Accounting (12th Edition)

Discussion Analysis A13-41 Discussion Questions 1. How do managers use the statement of cash flows? 2. Describ...

Managerial Accounting (5th Edition)

E6-14 Using accounting vocabulary

Learning Objective 1, 2

Match the accounting terms with the corresponding d...

Horngren's Accounting (11th Edition)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Larsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardMedical Tape makes two products: Generic and Label. It estimates it will produce 423,694 units of Generic and 652,200 of Label, and the overhead for each of its cost pools is as follows: It has also estimated the activities for each cost driver as follows: How much is the overhead allocated to each unit of Generic and Label?arrow_forwardThe following product costs are available for Stellis Company on the production of erasers: direct materials, $22,000; direct labor, $35,000; manufacturing overhead, $17,500; selling expenses, $17,600; and administrative expenses; $13,400. What are the prime costs? What are the conversion costs? What is the total product cost? What is the total period cost? If 13,750 equivalent units are produced, what is the equivalent material cost per unit? If 17,500 equivalent units are produced, what is the equivalent conversion cost per unit?arrow_forward

- Box Springs. Inc., makes two sizes of box springs: queen and king. The direct material for the queen is $35 per unit and $55 is used in direct labor, while the direct material for the king is $55 per unit, and the labor cost is $70 per unit. Box Springs estimates it will make 4,300 queens and 3,000 kings in the next year. It estimates the overhead for each cost pool and cost driver activities as follows: How much does each unit cost to manufacture?arrow_forwardPatterson Company produces wafers for integrated circuits. Data for the most recent year are provided: aCalculated using number of dies as the single unit-level driver. bCalculated by multiplying the consumption ratio of each product by the cost of each activity. Required: 1. Using the five most expensive activities, calculate the overhead cost assigned to each product. Assume that the costs of the other activities are assigned in proportion to the cost of the five activities. 2. Calculate the error relative to the fully specified ABC product cost and comment on the outcome. 3. What if activities 1, 2, 5, and 8 each had a cost of 650,000 and the remaining activities had a cost of 50,000? Calculate the cost assigned to Wafer A by a fully specified ABC system and then by an approximately relevant ABC approach. Comment on the implications for the approximately relevant approach.arrow_forwardWrappers Tape makes two products: Simple and Removable. It estimates it will produce 369,991 units of Simple and 146,100 of Removable, and the overhead for each of its cost pools is as follows: It has also estimated the activities for each cost driver as follows: Â How much is the overhead allocated to each unit of Simple and Removable?arrow_forward

- Rex Industries has two products. They manufactured 12,539 units of product A and 8.254 units of product B. The data are: What is the activity rate for each cost pool?arrow_forwardCool Pool has these costs associated with production of 20,000 units of accessory products: direct materials, $70; direct labor, $110; variable manufacturing overhead, $45; total fixed manufacturing overhead, $800,000. What is the cost per unit under both the variable and absorption methods?arrow_forwardSilven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forward

- Stacks manufactures two different levels of hockey sticks: the Standard and the Slap Shot. The total overhead of $600,000 has traditionally been allocated by direct labor hours, with 400,000 hours for the Standard and 200.000 hours for the Slap Shot. After analyzing and assigning costs to two cost pools, it was determined that machine hours is estimated to have $450.000 of overhead, with 30,000 hours used on the Standard product and 15,000 hours used on the Slap Shot product. It was also estimated that the inspection cost pool would have $150,000 of overhead, with 25,000 hours for the Standard and 5,000 hours for the Slap Shot. What is the overhead rate per product, under traditional and under ABC costing?arrow_forwardHercules Inc. manufactures elliptical exercise machines and treadmills. The products are produced in its Fabrication and Assembly production departments. In addition to production activities, several other activities are required to produce the two products. These activities and their associated activity rates are as follows: The activity-base usage quantities and units produced for each product were as follows: Use the activity rate and usage information to determine the total activity cost and activity cost per unit for each product.arrow_forwardEvans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Cost Accounting - Definition, Purpose, Types, How it Works?; Author: WallStreetMojo;https://www.youtube.com/watch?v=AwrwUf8vYEY;License: Standard YouTube License, CC-BY