Concept explainers

Videos

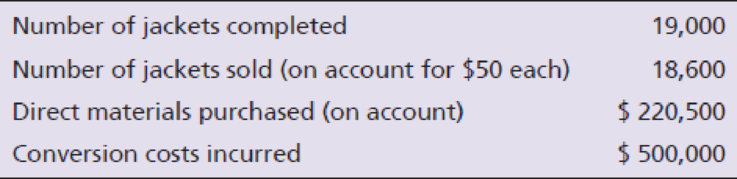

High Mountain produces fleece jackets. The company uses JIT costing for its JIT production system.

High Mountain has two inventory accounts: Raw and In-Process Inventory and Finished Goods Inventory. On April 1, 2018, the account balances were Raw and In-Process Inventory, $10,000; Finished Goods Inventory, $2,100.

The

Requirements

- 1. What are the major features of a JIT production system such as that of High Mountain?

- 2. Prepare summary

journal entries for April. Underallocated or overallocated conversion costs are adjusted to Cost of Goods Sold monthly. - 3. Use a T-account to determine the April 30, 2018, balance of Raw and In-Process Inventory.

Want to see the full answer?

Check out a sample textbook solution

Chapter 19 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Additional Business Textbook Solutions

Financial Accounting (11th Edition)

Horngren's Accounting (11th Edition)

Managerial Accounting

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Financial Accounting

Fundamentals Of Financial Accounting

- Webster Company uses backflush costing to account for its manufacturing costs. The trigger points for recording inventory transactions are the purchase of materials, the completion of products, and the sale of completed products. Required: 1. Prepare journal entries, if needed, to account for the followingtransactions. a. Purchased raw materials on account, 135,000. b. Requisitioned raw materials to production, 135,000. c. Distributed direct labor costs, 20,000. d. Incurred manufacturing overhead costs, 80,000. (Use Various Credits for the credit part of the entry.) e. Cost of products completed, 235,000. f. Completed products sold for 355,000, on account. 2. Prepare any journal entries that would be different from theabove, if the only trigger points were the purchase of materialsand the sale of finished goods.arrow_forwardKenkel, Ltd. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 80,000. b. Requisitioned raw materials to production, 80,000. c. Distributed direct labor costs, 10,000. d. Factory overhead costs incurred, 60,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 225,000, on account.arrow_forwardChassen Company, a cracker and cookie manufacturer, has the following unit costs for the month of June: A total of 100,000 units were manufactured during June, of which 10,000 remain in ending inventory. Chassen uses the first-in, first-out (FIFO) inventory method, and the 10,000 units are the only finished goods inventory at June 30. Under the absorption costing concept, the value of Chassens June 30 finished goods inventory would be: a. 50,000. b. 70,000. c. 85,000. d. 145,000.arrow_forward

- Davis Co. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 70,000. b. Requisitioned raw materials to production, 70,000. c. Distributed direct labor costs, 15,000. d. Factory overhead costs incurred, 45,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 195,000, on account. (Hint: Use a single account for raw materials and work in process.)arrow_forwardThe GreenEarth Aluminum Company uses a process cost accounting system to record the costs of manufacturing rolled aluminum. The manufacturing process consists of three processes. The goods-in-process inventory of one of the processes (the rolling department) on September 1, 2018 and debits to the account for September are summarized below: Beginning balance—5,100 units, 1/3 completed: Direct materials (5,100 x 38.70)$ 197,370 Conversion costs (5,100 x 1/3 x 11.72) 19,924 Total beginning balance 217,294 Additional debits during the month: Costs from Smelting Department (162,000 units) 6,240,000 Direct Labor 765,800 Factory Overhead 1,144,000 During the month of September, the 5,100 units in process at the beginning of the month were completed, and of the 162,000 units entering the department from Smelting, all were completed except 5,400 units that were 4/5 completed (hint—remember the materials are the items transferred from the Smelting Department). A) Determine the number of units…arrow_forwardCetaphil Manufacturing Company uses a Raw and in Process (RIP) inventory account and charged to cost of sales all conversion costs. At the end of each month, all inventories are counted, their conversion costs components are estimated and inventory account balances are adjusted accordingly. backflushed from RIP to Finished goods. The following information is noted for Raw materials is the current month. • Beginning balance of RIP account, including P1,400 conversion costs, P31,200 Raw materials purchased on account, P367,000 Ending RIP inventory including P1,800 conversion cost, P33,000. 12. Give the final entry to adjust the accounts to their correct balances.arrow_forward

- Pasay Manufacturing Company manufactures fire extinguishers and uses FIFO method for process and inventory costing. In valuing the finished goods inventory, the costs of units completed from the WIP beginning are kept separate from the costs of those started and completed during the period. The total manufacturing costs for the month of June were P924,000. There were 5,500 units that were completed during the month. All costs were uniformly applied to production. At the beginning of the period, there were 2,500 units in process that were 20% incomplete with a total cost of P448,000 and 1200 of completed fire extinguishers with a total cost of P268,800. At the end of the month, there were 1,000 units in process that were 50% complete and 1,400 of completed fire extinguishers. The cost of goods sold for the month isarrow_forwardSelected production and cost data of Amy's Craft Co. follow for May: View the production and cost data. On May31the Mixing Department ending Work-in-Process Inventory was 758omplete for materials and 25%omplete for conversion costs. The Heating Department ending Work-in-Process Inventory was 65%omplete for materials and 30%omplete for conversion costs. The company uses the weighted-average method. Read the requirements. Requirement 1. Compute the equivalent units of production for direct materials and for conversion costs for the Mixing Department. Complete the partial production cost report below for the Mixing Department, showing the equivalent units of production for direct materials and for conversion costs. Amy's Craft Co. Production Cost Report - Mixing Department (Partial) Month Ended May 31 UNITS Units accounted for: Total units accounted for Physical Units Equivalent Units Direct Materials Conversion Costs Production and Cost Data Units to account for: Beginning…arrow_forwardDash Company adopted a standard costing system several years ago. The standard costs for the prime costs (i.e., direct materials and direct labor) of its single product are: Material (5 kilograms × $5.00 per kilogram) $ 25.00 Labor (6 hours × $19.50 per hour) 117.00 All materials are added at the beginning of processing. The following data were taken from the company’s records for November: In-process beginning inventory None In-process ending inventory 800 units, 70% complete as to direct labor Units completed 6,400 units Budgeted output 6,800 units Purchases of materials 58,000 kilograms Total actual direct labor costs $ 750,000 Actual direct labor hours 41,000 hours Materials usage variance $ 2,300 Unfavorable Total materials variance $ 850 Unfavorable Required: 1. Compute for November: a. The direct labor efficiency variance. Is this variance favorable (F) or unfavorable (U)? b. The direct labor rate…arrow_forward

- Dash Company adopted a standard costing system several years ago. The standard costs for the prime costs (i.e., direct materials and direct labor) of its single product are: Material (5 kilograms × $5.00 per kilogram) $ 25.00 Labor (6 hours × $19.50 per hour) 117.00 All materials are added at the beginning of processing. The following data were taken from the company’s records for November: In-process beginning inventory None In-process ending inventory 800 units, 70% complete as to direct labor Units completed 6,400 units Budgeted output 6,800 units Purchases of materials 58,000 kilograms Total actual direct labor costs $ 750,000 Actual direct labor hours 41,000 hours Materials usage variance $ 2,300 Unfavorable Total materials variance $ 850 Unfavorable Required: 1. Compute for November: a. The direct labor efficiency variance. Is this variance favorable (F) or unfavorable (U)? b. The direct labor rate…arrow_forwardCAVS Inc. employs weighted average process costing system regarding its cross-over protector product. The following data are provided for the year-ended December 31, 2020. a. The January 1, 2020 work-in-process inventory consists of 4,000 units which have the following costs: P100,000-direct material, P250,000-direct labor and P150,000-factory overhead. The beginning inventory is 60% incomplete as to conversion cost. b. The units started during the year totaled 6,000 units while the units completed during the period totaled 5,000 units. c. The December 31, 2020 work-in-process inventory consists of 3,000 units which is 90% complete as to conversion cost. d. The normal spoilage for the company is 20% of units started. e. The total manufacturing costs added during the year consist of P2M-direct material, P1.5M-direct labor, and P1M-factory overhead. f. The company inspects the products when the percentage of completion in conversion cost is 70%. g. The company adds direct labor and…arrow_forwardLakers Inc. employs weighted average process costing system regarding its cross-over protector product. The following data are provided for the year ended December 31, 2016: a. The January 1, 2016 work-in-process inventory consists of 4,000 units which have the following costs: P100,000-direct material, P250,000-direct labor and P150,000-factory overhead. The beginning inventory is 60% incomplete as to conversion cost.b. The units started during the year totaled 6,000 units while the units completed during the period totaled 5,000 units.c. The December 31, 2016 work-in-process inventory consists of 3,000 units which is 90% complete as to conversion cost.d. The normal spoilage for the company is 20% of units started.e. The total manufacturing costs added during the year consist of P2M-direct material, P1.5M –direct labor and P1M-factory overhead.f. The company inspects the products when the percentage of completion in conversion cost is 70%.g. The…arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning