Videos

Effect of activity level and opportunity cost on segment elimination decision

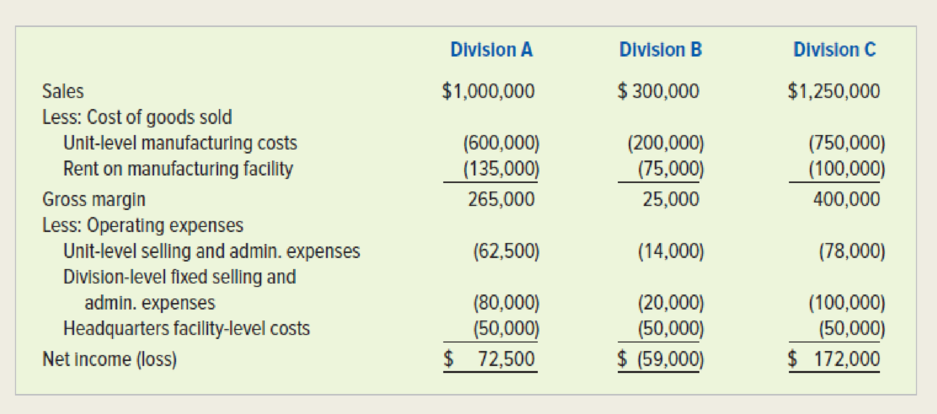

Lenox Manufacturing Co. produces and sells specialized equipment used in the petroleum industry. The company is organized into three separate operating branches: Division A, which manufactures and sells heavy equipment; Division B, which manufactures and sells hand tools; and Division C, which makes and sells electric motors. Each division is housed in a separate manufacturing facility. Company headquarters is located in a separate building. In recent years, Division B has been operating at a net loss and is expected to continue to do so. Income statements for the three divisions for 2017 follow:

Required

- a. Based on the preceding information, recommend whether to eliminate Division B. Support your answer by preparing companywide income statements before and after eliminating Division B.

- b. During 2017, Division B produced and sold 20,000 units of hand tools. Would your recommendation in response to Requirement a change if sales and production increase to 30,000 units in 2018? Support your answer by comparing differential revenue and avoidable cost for Division B, assuming that it sells 30,000 units.

- c. Suppose that Lenox could sublease Division B’s manufacturing facility for $160,000. Would you operate the division at a production and sales volume of 30,000 units, or would you close it? Support your answer with appropriate computations.

a.

Identify whether Division B is eliminated or not.

Explanation of Solution

Special order decisions: Special order decisions include circumstances in which the board must choose whether to acknowledge abnormal customer orders. These requests or orders normally necessitate special dispensation or include a demand for lesser price.

Outsourcing: It can be termed as conveying all or part of an activity to a supplier or a provider. While outsourcing was initially limited to fundamental activities, it as of now invades the administration of numerous organizations.

Opportunity cost: Opportunity cost is the forfeit of certain benefits such as cost savings, incomes, which is surrendered by not picking an option. Opportunity costs are applicable in decisions where the acknowledgment of one option disqualifies the likelihood of selecting different alternatives.

Determine the contribution to profit

Therefore the contribution to profit is ($9,000).

Prepare the companywide income statement before and after eliminating Division B.

The company wide income statement before eliminating Division B is as follows:

| Companywide Income Statement before Division B is eliminated | |

| Sales | S2,550,000 |

| Less: Cost of goods sold | |

| Unit level manufacturing costs | $1,550,000 |

| Rent on manufacturing facility | $310,000 |

| Gross margin | $690,000 |

| Less: Operating expenses | |

| Unit level selling & administrative costs | $154,500 |

| Division level fixed selling & administrative costs | $200,000 |

| Headquarters facility-level costs | $150,000 |

| Net income (loss) | $185,500 |

Table (1)

The company wide income statement after eliminating Division B is as follows:

| Companywide Income Statement after Division B is eliminated | |

| Sales | $2,250,000 |

| Less: Cost of goods sold | |

| Unit level manufacturing costs | $ 1,350,000 |

| Rent on manufacturing facility | $235,000 |

| Gross margin | $665,000 |

| Less: Operating expenses | |

| Unit level selling & administrative costs | $140,500 |

| Division level fixed selling & administrative costs | $180,000 |

| Headquarters facility-level costs | $ 150,000 |

| Net income (loss) | $194,500 |

Table (2)

From the results obtained above, the contribution to profit is negative at ($9,000). Hence the Division B should be eliminated.

Therefore, Division B should be eliminated.

b.

Identify whether the recommendations in Requirement A changes if the units increased to 30,000 units by comparing Division B’s differential avoidable costs and revenue.

Explanation of Solution

Initiate by calculating the cost price per unit and the selling per unit that will change in respect to the quantity of units produced and traded. The result is divided with the total cost for respective group by 20,000 units to get cost per unit. The headquarters facility-level costs are not considered from the investigation since these costs are not avoidable.

Determine the selling price per unit

Therefore, the selling price per unit is $15.

Determine the unit level manufacturing costs

Therefore, the unit level manufacturing costs is $10.

Determine the unit level selling and administrative costs

Therefore, the unit level selling and administrative costs is $0.70.

Determine the contribution to profit

The comparison between differential revenue and avoidable cost is determined in the below step.

Therefore, the contribution to profit is $34,000.

From the results obtained above, the profit contributed by Division B would be 30,000 units. Hence the division should not be eliminated. Additionally, it is vital to contemplate development prospective before choosing to eliminate a segment.

Therefore, Division B should not be eliminated.

c.

Identify whether to operate the division with volume of 30,000 units or it should be closed.

Explanation of Solution

Determine the profit or loss of the division

Therefore, the loss of the division is $51,000.

The reasons on whether to operate the division with volume of 30,000 units or it should be closed is as follows:

- It is mentioned that Company LM is paying $75,000 to lease the manufacturing facility for Division B.

- The business could earn $85,000

- By operating the division, the organization is allowing up the chance to sublease the office.

- This is an opportunity cost that would be avoidable by eradicating Division B.

- Consequently, it must be incorporated into the investigation. If the volume is 30,000 units Division B contributes $34,000 as profit.

When considering opportunity cost, the profit turns into a loss of $51,000. According to these conditions, Division B should be eliminated.

Therefore, Division B should be eliminated.

Want to see more full solutions like this?

Chapter 13 Solutions

Survey Of Accounting

- The Mega Supply Corporation has three divisions: Commercial Products, Consumer Products, and Corporate Offices, which are located in Hatfield, South Carolina; Palo Alto, California; and Tulsa, Oklahoma, respectively. The Commercial Products division deals exclusively in sales of industrial products and supplies to business organizations. The Consumer Products division sells nonindustrial products to private consumers. Both divisions have dedicated inventory warehouses at their respective locations in Hatfield and Palo Alto. Because of the dissimilar nature of the commercial and consumer division product lines, they do not share customers or vendors. Currently Mega Supply uses a centralized database, which is located at their Corporate Division in Tulsa. Some relevant database tables and attributes are presented in the figure designated Problem 1. When customers contact their respective sales division, the sales clerk logs into the corporate database, checks credit, determines product availability, and creates a sales invoice. The corporate office typically bills the customer within 3 or 4 days and extends terms of net 30. Inventory control, AR processing, cash receipts, purchases from vendors and AP processing, and cash disbursements are performed by the corporate office. Due to Megas rapid growth, the company has seen a significant increase in sales and purchase transactions, which has resulted in excessive delays in processing transactions from the central database. Since customer service, including rapid response to customer inquiries and sales order processing, is a cornerstone of Megas business model, these delays are unacceptable. Required Mega wants to improve response time by distributing some parts of the corporate database while keeping other parts of it centralized. (A) Develop a schema for distributing Mega Supply Corporations database. Add new tables and attributes as needed but limit the schema to the tables needed to support sales, cash receipts, purchases/AP, and cash disbursements. In your schema, indicate whether tables are centralized, replicated, or partitioned. (B) Explain how the new system will operate.arrow_forwardCode Incorporated has three divisions (Entertainment, Plastics, and Video Card), each of which is considered an investment center for performance evaluation purposes. The Entertainment Division manufactures video arcade equipment using products produced by the other two divisions, as follows: 1. The Entertainment Division purchases plastic components from the Plastics Division that are considered unique (i.e., they are made exclusively for the Entertainment Division). In addition, the Plastics Division makes less-complex plastic components that it sells externally, to other producers. 2. The Entertainment Division purchases, for each unit it produces, a video card from Code's Video Card Division, which also sells this video card externally (to other producers). The per-unit manufacturing costs associated with each of the above two items, as incurred by the Plastic Components Division and the Video Card Division, respectively, are: Plastic Components Video Cards Direct…arrow_forwardTrump Forest Corporation operates two divisions, the Timber Division and the Consumer Division. The Timber Division manufactures and sells logs to paper manufacturers. The Consumer Division operates retail lumber mills which sell a variety of products in the do-it-yourself homeowner market. The company is considering disposing of the Consumer Division since it has been consistently unprofitable for a number of years. The income statements for the two divisions for the year ended December 31, 2019 are presented below: Timber Division Consumer Division Total Sales $1,500,000 $500,000 $2,000,000 Cost of goods sold 900,000 350,000…arrow_forward

- The composting division has identified a source of additional compostable waste at a price of $205 per ton. What would be the impact on the company as a whole if the 400 tons of material is purchased from the outside supplier? As a decentralized unit, what decision would the composting division make regarding the additional material?arrow_forwardCleene Division of Soaphen Corporation produces soap, 20% of which are sold to Bubbly Division of Soaphen Corporation. The remainder is sold to outside customers. Soaphen treats its divisions as profit centers and allows division managers to choose their sources of sale and supply. Corporate policy requires that all interdivisional sales and purchases be recorded at variable cost at transfer price. Cleene Division’s estimated sales and standard cost data for the year ending December 31, 2000, based on capacity of 100,000 units are as follows: BUBBLY OUTSIDERS Sales 900,000 8,000,000 Variable Costs (900,000) (3,600,000) Fixed costs (300,000) (1,200,000) Gross Margin (300,000) (320,000) Unit Sales 20,000 80,000 Cleene has an opportunity to sell the 20,000 units shown above to an outside customer at a price of P75 per unit. Bubbly can purchase its requirements from an outside supplier at a price of P85 per unit.…arrow_forwardGarcon Inc. manufactures electronic products, with two operating divisions, Consumer and Commercial. Condensed divisional income statements, which involve no intracompany transfers and which include a breakdown of expenses into variable and fixed components, are as follows: (refer to pic) The Consumer Division is presently producing 14,400 units out of a total capacity of 17,280 units. Materials used in producing the Commercial Division’s product are currently purchased from outside suppliers at a price of $150 per unit. The Consumer Division is able to produce the materials used by the Commercial Division. Except for the possible transfer of materials between divisions, no changes are expected in sales and expenses. 5A What is the range of possible negotiated transfer prices that would be acceptable for Garcon Inc.? 5B Assuming that the managers of the two divisions cannot agree on a transfer price, what price would you suggest as the transfer price? Would the market price…arrow_forward

- TAC Industries, Inc. sells heavy equipment to large corporations and federal, state, and local governments. Corporate sales are the result of a competitive bidding process, where TAC competes against other companies based on selling price. Sales to the government are determined on a cost plus basis, where the selling price is determined by adding a fixed markup percentage to the total job cost. Tandy Lane is the cost accountant for the Equipment Division of TAC Industries Inc. The division is under pressure from senior management to improve operating income. As Tandy reviewed the division's job cost sheets, she realized that she could increase the division's operating income by moving a portion of direct labor hours that had been assigned to the job cost sheets of corporate customers onto the job order cost sheets of government customers. She believed that this would create a "win-win" for the division by (1) reducing the cost of corporate jobs, and (2) increasing the cost of…arrow_forwardBath Bath Co is a company specialising in the manufacture and sale of baths. Each bath consists of a main unit plus a set of bath fittings. The company is split into two divisions, A and B. Division B manufactures the bath and Division A manufactures sets of bath fittings, which are both sold externally and transferred to Division B. Both of the divisions are treated as profit centres. The following data is available for both divisions: Division A Division B External selling price of items £80 £450 Transfer price £75 Internal standard variable costs per item £20 £245 Annual fixed costs £4,400,000 £7,440,000 Annual production capacity 200,000 80,000 Maximum external demand 180,000 80,000 The transfer price charged by Division A to Division B was negotiated some years ago between the previous divisional managers, who have both now been replaced by new managers. Head Office only allows Division B to purchase its fittings…arrow_forwardPhoenix Inc., a cellular communication company, has multiple business units, organized as divisions. Each division’s management is compensated based on the division’s operating income. Division A currently purchases cellular equipment from outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside customers—but not to division A at this time. Division A’s manager approaches division B’s manager with a proposal to buy the equipment from division B. If it produces the cellular equipment that division A desires, division B will incur variable manufacturing costs of $60 per unit. Relevant Information about Division B Sells 90,000 units of equipment to outside customers at $130 per unit Operating capacity is currently 80%; the division can operate at 100% Variable manufacturing costs are $70 per unit Variable marketing costs are $8 per unit Fixed manufacturing costs are $900,000 Income per Unit for Division A…arrow_forward

- T-Comm makes a variety of products. It is organized in two divisions, North and South. The managers for each division are paid, in part, based on the financial performance of their divisions. The South Division normally sells to outside customers but, on occasion, also sells to the North Division. When it does, corporate policy states that the price must be cost plus 15 percent to ensure a “fair” return to the selling division. South received an order from North for 600 units. South’s planned output for the year had been 2,400 units before North’s order. South’s capacity is 3,000 units per year. The costs for producing those 2,400 units follow. Total Per Unit Materials $ 480,000 $ 200 Direct labor 230,400 96 Other costs varying with output 153,600 64 Fixed costs (do not vary with output) 2,016,000 840 Total costs $ 2,880,000 $ 1,200 Required: a. If you are the manager of the South Division, what unit cost would you ask…arrow_forwardT-Comm makes a variety of products. It is organized in two divisions, North and South. The managers for each division are paid, in part, based on the financial performance of their divisions. The South Division normally sells to outside customers but, on occasion, also sells to the North Division. When it does, corporate policy states that the price must be cost plus 15 percent to ensure a “fair” return to the selling division. South received an order from North for 600 units. South’s planned output for the year had been 2,400 units before North’s order. South’s capacity is 3,000 units per year. The costs for producing those 2,400 units follow.arrow_forwardCommunicationTAC Industries sells heavy equipment to large corporations and to federal, state, and local governments. Corporate sales are the result of a competitive bidding process, where TAC competes against other companies based on selling price. Sales to the government, however, are determined on a cost plus basis, where the selling price is determined by adding a fixed markup percentage to the total job cost.Tandy Lane is the cost accountant for the Equipment Division of TAC Industries Inc. The division is under pressure from senior management to improve income from operations.As Tandy reviewed the division’s job cost sheets, she realized that she could increase the division’s income from operations by moving a portion of the direct labor hours that had been assigned to the job order cost sheets of corporate customers onto the job order costs sheets of government customers. She believed that this would create a win-win for the division by (1) reducing the cost of corporate jobs…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,