Videos

The Mega Supply Corporation has three divisions: Commercial Products, Consumer Products, and Corporate Offices, which are located in Hatfield, South Carolina; Palo Alto, California; and Tulsa, Oklahoma, respectively. The Commercial Products division deals exclusively in sales of industrial products and supplies to business organizations. The Consumer Products division sells nonindustrial products to private consumers. Both divisions have dedicated inventory warehouses at their respective locations in Hatfield and Palo Alto. Because of the dissimilar nature of the commercial and consumer division product lines, they do not share customers or vendors.

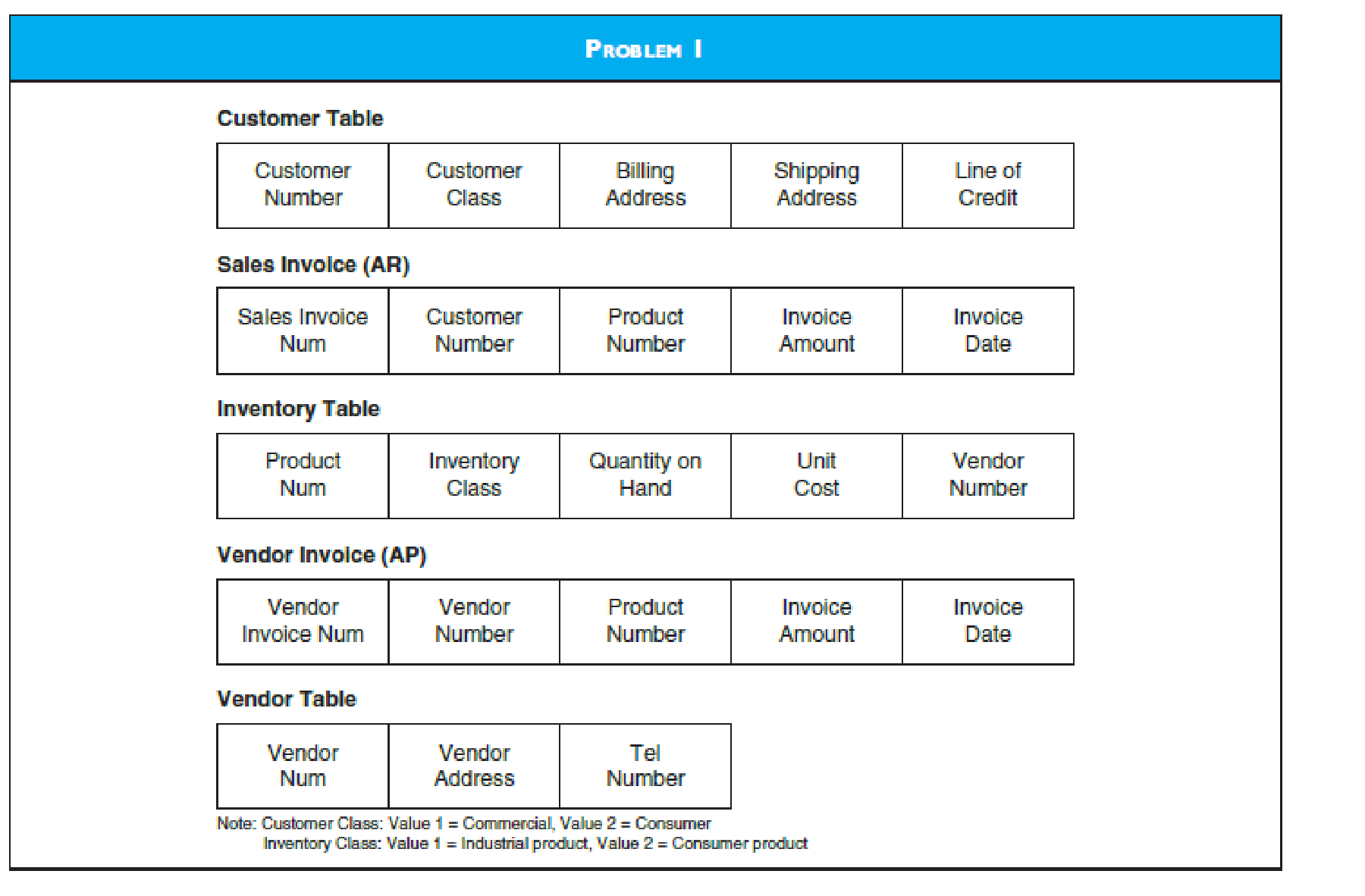

Currently Mega Supply uses a centralized database, which is located at their Corporate Division in Tulsa. Some relevant database tables and attributes are presented in the figure designated Problem 1.

When customers contact their respective sales division, the sales clerk logs into the corporate database, checks credit, determines product availability, and creates a sales invoice. The corporate office typically bills the customer within 3 or 4 days and extends terms of net 30. Inventory control,

Due to Mega’s rapid growth, the company has seen a significant increase in sales and purchase transactions, which has resulted in excessive delays in processing transactions from the central database. Since customer service, including rapid response to customer inquiries and sales order processing, is a cornerstone of Mega’s business model, these delays are unacceptable.

Required

Mega wants to improve response time by distributing some parts of the corporate database while keeping other parts of it centralized.

- (A) Develop a schema for distributing Mega Supply Corporation’s database. Add new tables and attributes as needed but limit the schema to the tables needed to support sales, cash receipts, purchases/AP, and cash disbursements. In your schema, indicate whether tables are centralized, replicated, or partitioned.

- (B) Explain how the new system will operate.

Trending nowThis is a popular solution!

Chapter 9 Solutions

Accounting Information Systems

- Phoenix Inc., a cellular communication company, has multiple business units, organized as divisions. Each division’s management is compensated based on the division’s operating income. Division A currently purchases cellular equipment from outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside customers—but not to division A at this time. Division A’s manager approaches division B’s manager with a proposal to buy the equipment from division B. If it produces the cellular equipment that division A desires, division B will incur variable manufacturing costs of $60 per unit. Relevant Information about Division B Sells 90,000 units of equipment to outside customers at $130 per unit Operating capacity is currently 80%; the division can operate at 100% Variable manufacturing costs are $70 per unit Variable marketing costs are $8 per unit Fixed manufacturing costs are $900,000 Income per Unit for Division A…arrow_forwardLessing Toy and Hobby (LTH) is a chain of hobby and craft stores in the Southeast. LTH operates multiple stores and is organized into two divisions: Northern and Southern. Individual stores are placed in one or the other division based on geography. Recent demographic changes in the Northern Division area have led to declining foot traffic and sales in the LTH stores. Senior corporate executives have been asking whether the chain should close those stores and focus on the stores in the Southern Division. The most recent income statement for the Northern Division follows. LESSING TOY & HOBBY Northern Division For the Year Ending January 31 ($000) Sales revenue Costs Cost of goods sold Advertising Administrative salaries Sales commissions Rent and occupancy expense Allocated corporate support Total costs Net loss before tax benefit Tax benefit at 25% Net loss $ 12,040 $ 6,020 490 810 1,624 2,058 1,330 $ 12,332 $ (292) (73) $ (219) The managers of Lessing Toy & Hobby (LTH) have decided to…arrow_forwardThe Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forward

- The Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forwardCable Network System Bhd (CNS) is a supplier of equipment to telecommunication companies such as Maxis, Celcom and Astro. It has two division, Component Division and the Equipment Division. CNS adopts a decentralized management system where managers are essentially free to determine whether goods will be transferred internally and what would be the internal transfer prices. CNS policy is that for all internal transfers between divisions, the transfer price be expressed on a full cost basis. The markup in the full cost arrangement is left to the discretion of divisional managers. The managers of the two division held a meeting to discuss on the pricing arrangement for a mini- antennae produced by the component division. Production of the mini-antennae is currently at full capacity. The Component Division can sell the mini-antennae for RM 46.50 to outside customers. The Equipment Division can also buy the mini-antennae from external sources for the same price. The manager of the…arrow_forwardThe Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forward

- Lenox Manufacturing Co. produces and sells specialized equipment used in the petroleum industry. The company is organized into three separate operating branches: Division A, which manufactures and sells heavy equipment; Division B, which manufactures and sells hand tools; and Division C, which makes and sells electric motors. Each division is housed in a separate manufacturing facility. Company headquarters is located in a separate building. In recent years, Division B has been operating at a net loss and is expected to continue to do so. Income statements for the three divisions for year 2 follow. Division A Division B Division C Sales $1,000,000 $ 300,000 $1,250,000 Less: Cost of goods sold Unit-level manufacturing costs Rent on manufacturing facility Gross margin Less: Operating expenses Unit-level selling and administrative expenses Division-level fixed selling and administrative (600,000) (135,000) 265,000 (200,000) (75,000) 25,000 (750,000) (100,000) 400,000 (62,500) (14,000)…arrow_forwardSimon Forest Corporation operates two divisions, the Timber Division and the Consumer Division. The Timber Division manufactures and sells logs to paper manufacturers. The Consumer Division operates retail lumber mills which sell a variety of products in the do-it-yourself homeowner market. The company is considering disposing of the Consumer Division since it has been consistently unprofitable for a number of years. The income statements for the two divisions for the year ended December 31, 2002 are presented below: Timber Division Consumer Division Total Sales P1,500,000 P500,000 P2,000,000 Cost of goods sold 900,000 350.000 1.250.000 Gross profit Selling & admin expenses 600,000 150,000 750,000 250,000 180,000 430,000 Net income P 350,000 P(30,000) P 320,000 In the Consumer Division, 70% of the cost of goods sold are variable costs and 30% of selling and administrative expenses are variable costs. The management of the company feels it can save P60,000 of fixed cost of goods sold…arrow_forwardCable Network System Bhd (CNS) is a supplier of equipment to telecommunication companies such as Maxis, Celcom and Astro. It has two division, Component Division and the Equipment Division. CNS adopts a decentralized management system where managers are essentially free to determine whether goods will be transferred internally and what would be the internal transfer prices. CNS policy is that for all internal transfers between divisions, the transfer price be expressed on a full cost basis. The markup in the full cost arrangement is left to the discretion of divisional managers. The managers of the two division held a meeting to discuss on the pricing arrangement for a mini- antennae produced by the component division. Production of the mini-antennae is currently at full capacity. The Component Division can sell the mini-antennae for RM 46.50 to outside customers. The Equipment Division can also buy the mini-antennae from external sources for the same price. The manager of the…arrow_forward

- Universal Auto is a large multinational corporation headquartered in the United States. For segment reporting purposes, the company is engaged in two businesses: production of motor vehicles and information processing services.The motor vehicle business is by far the larger of Universal’s two segments. It consists mainly of domestic U.S. passenger car production, but it also includes small truck manufacturing operations in the United States and passenger car production in other countries. This segment of Universal has had weak operating results for the past several years, including a large loss in 2017. Although the company does not reveal the operating results of its domestic passenger car segments, that part of Universal’s business is generally believed to be primarily responsible for the weak performance of its motor vehicle segment.Idata, the information processing services segment of Universal, was started by Universal about 15 years ago. This business has shown strong, steady…arrow_forwardMulti-Store Limited is a small regional chain of supermarkets in the Northern Cape. Thechain manages their accounting per store but in addition they run the Deli, Butchery andGoods sections as separate reporting cost centres. In addition they have two servicedepartments the Finance Department that deals with the financial administration and theInventory Department that deals with the ordering, delivery and warehousing of goods.They are currently reviewing the profitability and efficiency of the three cost centres andhave adopted an Activity-Based-Costing (ABC) approach. The following information hasbeen extracted from their accounting and activity records:The following Overheads are to be apportioned: Cost R Basis of allocation to cost centres Ordering costs 250 000 Number of order issued Goods Received Costs 320 000 Number of Goods Received Notes issued Management and AdministrationCosts 1 200000 Rand value turnover Property costs 850 000 Square meters occupied…arrow_forwardMulti-Store Limited is a small regional chain of supermarkets in the Northern Cape. Thechain manages their accounting per store but in addition they run the Deli, Butchery andGoods sections as separate reporting cost centres. In addition they have two servicedepartments the Finance Department that deals with the financial administration and theInventory Department that deals with the ordering, delivery and warehousing of goods.They are currently reviewing the profitability and efficiency of the three cost centres andhave adopted an Activity-Based-Costing (ABC) approach. The following information hasbeen extracted from their accounting and activity records:The following Overheads are to be apportioned: Cost R Basis of allocation to cost centres Ordering costs 250 000 Number of order issued Goods Received Costs 320 000 Number of Goods Received Notes issued Management and AdministrationCosts 1 200000 Rand value turnover Property costs 850 000 Square meters occupied…arrow_forward

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub