EBK CFIN

6th Edition

ISBN: 9781337671743

Author: BESLEY

Publisher: CENGAGE LEARNING - CONSIGNMENT

expand_more

expand_more

format_list_bulleted

Question

Chapter 8, Problem 9PROB

Summary Introduction

Expected

Standard deviation is the financial measure of risk and stability on the

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

An investiment portfolio consists of two securities, X and Y. The weight of X is 30%.

Asset X's expected return is 15% and the standard deviation is 28%.

Asset Y's expected return is 23% and the standard deviation is 33%.

Assume the correlation coefficient between X and Y is 0.37.

A. Calcualte the expected return of the portfolio.

B. Calculate the standard deviation of the portfolio return.

C. Suppose now the investor decides to add some risk free assets into this portfolio.

The new weights of X, Y and risk free assets are 0.21, 0.49 and 0.30. What is the standard deviation of the new portfolio?

The following portfolios are being considered for investment. During the period under consideration, RFR = 0.07.Portfolio Return Beta σiA 0.15 1.0 0.05B 0.20 1.5 0.10C 0.10 0.6 0.03D 0.17 1.1 0.06Market 0.13 1.0 0.04

a. Compute the Sharpe measure for each portfolio and the market portfolio.

b. Compute the Treynor measure for each portfolio and the market portfolio.

c. Rank the portfolios using each measure, explaining the cause for any differences you find in the rankings.

The following portfolios are being considered for investment. During the period under consideration, RFR = 0.08.

Portfolio

Return

Beta

σi

P

0.14

1.00

0.05

Q

0.20

1.30

0.11

R

0.10

0.60

0.03

S

0.17

1.20

0.06

Market

0.12

1.00

0.04

Compute the Sharpe measure for each portfolio and the market portfolio. Round your answers to three decimal places.

Portfolio

Sharpe measure

P

Q

R

S

Market

Compute the Treynor measure for each portfolio and the market portfolio. Round your answers to three decimal places.

Portfolio

Treynor measure

P

Q

R

S

Market

Knowledge Booster

Similar questions

- The following portfolios are being considered for investment. During the period under consideration, RFR =0.07 Porfolio Return Beta P 0.15 1.00 0.05 Q 0.20 1.50 0.1 R 0.10 0.60 0.03 S 0.17 1.10 0.06 Market 0.13 1.00 0.04 Compute the Sharpe measure for each portfolio and the market portfolio Compute the Treynor measure for each portfolio and the market portfolio Rank the portfolios using each measure explaining the cause for any differences you find in the rankings.arrow_forwardConsider the following information for four portfolios, the market, and the risk-free rate (RFR): Portfolio Return Beta SD A1 0.15 1.25 0.182 A2 0.1 0.9 0.223 A3 0.12 1.1 0.138 A4 0.08 0.8 0.125 Market 0.11 1 0.2 RFR 0.03 0 0 Refer to Exhibit 18.6. Calculate the Jensen alpha Measure for each portfolio. a. A1 = 0.014, A2 = -0.002, A3 = 0.002, A4 = -0.02 b. A1 = 0.002, A2 = -0.02, A3 = 0.002, A4 = -0.014 c. A1 = 0.02, A2 = -0.002, A3 = 0.002, A4 = -0.014 d. A1 = 0.03, A2 = -0.002, A3 = 0.02, A4 = -0.14 e. A1 = 0.02, A2 = -0.002, A3 = 0.02, A4 = -0.14arrow_forwardThe following portfolios are being considered for investment. During the period under consideration, RFR = 0.07. Portfolio Return Beta P 0.15 1.00 0.05 Q 0.09 0.50 0.03 R. 0.21 1.30 0.10 0.18 1.20 0.06 Market 0.12 1.00 0.04 a. Compute the Sharpe measure for each portfolio and the market portfolio. Round your answers to three decimal places. Portfolio Sharpe measure P Q R Market b. Compute the Treynor measure for each portfolio and the market portfolio. Round your answers to three decimal places. Portfolio Treynor measure P Q R Market c. Rank the portfolios using each measure, explaining the cause for any differences you find in the rankings. Portfolio Rank (Sharpe measure) Rank (Treynor measure) P |-Select- v |-Select- v Q -Select- v -Select- V R. -Select- V -Select- v -Select- v -Select- v Market -Select- v -Select- v -Select- v is poorly diversified since it has a high ranking based on the -Select- but a much lower ranking with the -Select-arrow_forward

- An investment has probabilities 0.15, 0.34, 0.44, 0.67, 0.2 and 0.15 of giving returns equal to 50%, 39%, -4%, 20%, -25%, and 42%. What are the expected returns and the standard deviations of returns?arrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Y Z Market Risk-free Rp 16.00% бр 32.00% 15.00 27.00 7.30 17.00 11.30 5.80 22.00 0 Bp 1.90 1.25 0.75 1.00 0 Assume that the tracking error of Portfolio X is 13.40 percent. What is the information ratio for Portfolio X? Note: A negative value should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to 4 decimal places. Information ratioarrow_forwardConsider two assets. Suppose that the return on asset 1 has expected value 0.05 and standard deviation 0.1 and suppose that the return on asset 2 has expected value 0.02 and standard deviation 0.05. Suppose that the asset returns have correlation 0.4.Consider a portfolio placing weight w on asset 1 and weight 1-w on asset 2; let Rp denote the return on the portfolio. Find the mean and variance of Rp as a function of w.arrow_forward

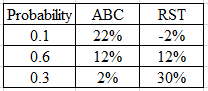

- Following is the portfolio weights, w, percentage expected return in (%), R, vectors and variance-covariance matrix, VC, for a three-asset portfolio: 0.4 12 100 -45 10 w = [0.3], R = [10] and VC = [-45 64 10] 0.3 8 10 10 36 a. Calculate the expected return and standard deviation of the portfolio. b. Suppose an investor requires a target standard deviation of 4% for the portfolio; using the solver function in Excel, find the portfolio weights w to maximise the expected return subject to the constraints Op = 4 and wi + w2 + w3 = 1|arrow_forwardCompute the (a) expected return, (b) standard deviation, and (c) coefficient of variation for investments with the following probability distributions: Probability r/A r/B 0.3 30.0% 5.0% 0.2 10.0 15.0 0.5 -2.0 25.0arrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: 8p 1.70 1.30 0.85 1.00 Portfolio X Y Z Market Risk-free Rp 11.5% 10.5 7.2 10.9 4.6 R-squared op 38.00% 33.00 23.00 28.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 0.76. What percentage of Portfolio Y's return is driven by the market? Note: Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places.arrow_forward

- Suppose the risk-free rate is 6 percent and the market portfolio has an expected return of 12 percent. The market portfolio has a standard deviation of 7 percent. Portfolio Z has a correlation coefficient with the market of 0.35 and standard deviation of 6 percent. According to the capital asset pricing model, what is the expected return on portfolio Z a. 12.6 percent b. 7.8 percent c. 9.87 percent d. 12.05 percentarrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Y Z Market Risk-free Rp 13.5% бр 35.00% 12.5 30.00 7.1 20.00 10.6 4.4 25.00 0 Вр 1.55 1.20 0.80 1.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 0.70. What percentage of Portfolio Y's return is driven by the market? Note: Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places. × Answer is complete but not entirely correct. R-squared 0.9785arrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio X Y Z Market Risk-free Rp 14.0% 13.0 .8.5 12.0 7.2 Ор 39.00% 34.00 24.00 29.00 0 Bp 1.50 1.15 0.90 1.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 0.90. What percentage of Portfolio Y's return is driven by the market? Note: Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places. R-squaredarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT