EBK CFIN

6th Edition

ISBN: 9781337671743

Author: BESLEY

Publisher: CENGAGE LEARNING - CONSIGNMENT

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Question

Chapter 8, Problem 4PROB

Summary Introduction

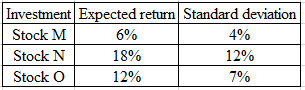

Expected

Standard deviation is the financial measure of risk and stability on the

Coefficient of variance is a measure used to calculate the total risk per unit of return of an investment.

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Calculate the coefficients of variation for the following stocks:

Stock

Expected return

Standard deviation of return

1

0.065

0.25

2

0.06

0.17

3

0.14

0.24

What is the coefficient of variation for stock 1?

What is the coefficient of variation for stock 2?

What is the coefficient of variation for stock 3?

f you want to get the best risk-to-reward trade-off, which stock should you buy?

Stock 2

Stock 3

Stock 1

Questions:

a. Compute the expected return for stock X and for stock Y

b. Compute the standard deviation for stock X and for stock Y.

c. Determine the best course to take for investing.

The additional return over the risk-free rate needed to compensate investors for assuming an

average amount of risk.

a.

Market Risk Premium

b.

Risk-free rate

С.

Stock's beta

O d.

Security Market Line

e.

Required Return on Stock

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Problem 1 You are given the following information about stock X and the market portfolio, M: Riskless Asset (f) Stock X Market Portfolio (M) E(r) 0.04 (4%) ? 0.10 σ 0.00 0.30 0.20 You are not given the expected return of stock X. The correlation of the returns on the stock X and the market portfolio is equal to 0.4. a) What is the beta (6) of stock X? b) Assuming the CAPM holds, what is the expected return on stock X? c) You have $1,000 to invest in some combination of the risk-free asset, stock X, and the market portfolio. You are thinking of investing $300 in the risk free asset, $400 in stock X, and $300 in the market portfolio. What is the overall expected return, standard deviation and beta of this portfolio?arrow_forwardRISK AND RETURN: Stock A and Stock B have the following distribution of rates of return:State of the economy Probability Stock A returns Stock B returnsRecession 0.10 -20% 30%Normal 0.60 10 20Boom 0.30 70 50a. What are the expected returns and standard deviations of these two shares?b. As an investment analyst with Gold Coast Securities Ltd, which of these stocks wouldyou recommend to a risk avoider investor?arrow_forwarda) The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the risk- return characteristics of a portfolio consisting of only stocks A and B, and explain why? E(R) E(R) E(R) A A A (A) (B) (C) b) found to be half of the required return (Rs) on stock B. The risk-free rate (R) is one-fourth of the required Assume that using the Security Market Line (SML) the required rate of return (RA) on stock A is return on A. Return on market portfolio is denoted by RM. Find the ratio of beta of A (DA) to beta of B (OB). c) Assume that the short-term risk-free rate is 3%, the market index S&P500 is expected to pay returns of 15% with the standard deviation equal to 20%. Asset A pays on average 5%, has standard deviation equal to 20% and is NOT correlated with the S&P500. Asset B pays on average 8%, also has standard deviation equal to 20% and has correlation of 0.5 with…arrow_forward

- The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the risk-return characteristics of a portfolio consisting of only stocks A and B, and explain why? E(R) E(R) E(R) В В A A А (A) (B) (C)arrow_forwardK (Expected rate of return and risk) Syntex, Inc. is considering an investment in one of two common stocks. Given the information that follows, which investment is better, based on the risk (as measured by the standard deviation) and return? Common Stock A Probability 0.20 0.60 0.20 Common Stock B Return 13% 17% 18% Probability 0.10 0.40 0.40 0.10 (Click on the icon in order to copy its contents into a spreadsheet.) Return -7% 5% 16% 21% www a. Given the information in the table, the expected rate of return for stock A is 16.40 %. (Round to two decimal places.) The standard deviation of stock A is 1.74 %. (Round to two decimal places.) b. The expected rate of return for stock B is 9.8 %. (Round to two decimal places.) The standard deviation for stock B is 6.12 %. (Round to two decimal places.)arrow_forwardSuppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock A B Expected Return 11% 17 Correlation -1 Risk-free rate Standard Deviation 6% 9 Suppose that it is possible to borrow at the risk-free rate, r. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) (Do not round intermediate calculations. Round your answer to 3 decimal places.) %arrow_forward

- Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Expected Return 11% 17 Correlation = -1 Stock A B Standard Deviation 6% 9 Suppose that it is possible to borrow at the risk-free rate, rf. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) Note: Do not round intermediate calculations. Round your answer to 3 decimal places. Risk-free ratearrow_forwardSuppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock A B Expected Return 9% 19 Correlation = -1 Standard Deviation 5% 12 Suppose that it is possible to borrow at the risk-free rate, rf. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) (Do not round intermediate calculations. Round your answer to 3 decimal places.) Risk-free rate %arrow_forwardConsider the following stocks with equal probabilities of return: Outcome | Return (Stock A) | Return (Stock B) 1 -5% 2% 2 10% 12% 3 18% 15% Compute the expected returns of stock A and B. Compute the total risk and relative risk of stock A and B. Which stock is risky? Ignoring the probabilities, what is the total risk and relative risk of stock A and B? Which stock is risky? Round-off final answers only to two decimal places.arrow_forward

- b) The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the risk-return characteristics of a portfolio consisting of only stocks A and B, and explain why? E(R) E(R) E(R) B. B. A. A (A) (В) (C)arrow_forwardAn investor is considering to buy one of the following stocks: Stock Expected rate of return Risk W 15% 3.0% X 20% 5.0% Y 18% 3.6% Which stock he should buy? Select one: O a. Stock W or stock Y, both are indifference. O b. Stock W O c. Stock X O d. Stock Yarrow_forwardSuppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock Expected Return Standard Deviation A 11 % 7 % B 17 11 Correlation = –1 Suppose that it is possible to borrow at the risk-free rate, rf. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.) (Do not round intermediate calculations. Round your answer to 3 decimal places.)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Portfolio return, variance, standard deviation; Author: MyFinanceTeacher;https://www.youtube.com/watch?v=RWT0kx36vZE;License: Standard YouTube License, CC-BY