EBK CFIN

6th Edition

ISBN: 9781337671743

Author: BESLEY

Publisher: CENGAGE LEARNING - CONSIGNMENT

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Question

Chapter 8, Problem 3PROB

Summary Introduction

Expected

Standard deviation is the financial measure of risk and stability on the

Coefficient of variance is a measure used to calculate the total risk per unit of return of an investment.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

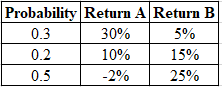

Compute the (a) expected return, (b) standard deviation, and (c) coefficient of variation for investments with the following probability distributions:

Probability r/A r/B

0.3 30.0% 5.0%

0.2 10.0 15.0

0.5 -2.0 25.0

Calculate the (a) expected return, (b) standard deviation, and (c) coefficient of variation for an investment with the following probability distribution:

Probability Payoff

0.45 32.0%

0.35 -4.0%

0.20 -20.0%

Calculate the expected return for an investment with the following probability distribution.

Return (%)

Probability (%)

-10

20

5

20

10

20

17

30

26

10

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The expected rate of return of an investment ________. a. equals one of the possible rates of return for that investment b. equals the required rate of return for the investment c. is the mean value of the probability distribution of possible returns d. is the median value of the probability distribution of possible returns e. is the mode value of the probability distribution of possible returnsarrow_forwardAn investment has probabilities 0.15, 0.34, 0.44, 0.67, 0.2 and 0.15 of giving returns equal to 50%, 39%, -4%, 20%, -25%, and 42%. What are the expected returns and the standard deviations of returns?arrow_forwardSupposing the return from an investment has the following probability distribution Return Probability R (%) 8 0.2 10 0.2 12 0.5 14 0.1 Required: What is the expected return of the investment? What is the risk as measured by the standard deviation of expected returns?arrow_forward

- Assuming that the rates of return associated with a given asset investment are normally distributed; that the expected return, r, is 18.7%; and that the coefficient of variation, CV, is 1.88, answer the following questions: a. Find the standard deviation of returns, sigma Subscript rσr. b. Calculate the range of expected return outcomes associated with the following probabilities of occurrence: (1) 68%, (2) 95%, (3) 99%.arrow_forwardThe standard deviation of return on investment a is 0.10, while the standard deviation of return on investment b is 0.04. If the correlation coefficient between the returns on A and B is_____________. A. -0.0447 B. -0.0020 C. 0.0020 D. 0.0447arrow_forwardTwo investments generated the following annual returns (refer to image): a. What is the average annual return on each investment?b. What is the standard deviation of the return on investments X and Y?c. Based on the standard deviation, which investment was riskier?arrow_forward

- Consider two assets. Suppose that the return on asset 1 has expected value 0.05 and standard deviation 0.1 and suppose that the return on asset 2 has expected value 0.02 and standard deviation 0.05. Suppose that the asset returns have correlation 0.4.Consider a portfolio placing weight w on asset 1 and weight 1-w on asset 2; let Rp denote the return on the portfolio. Find the mean and variance of Rp as a function of w.arrow_forwardAssuming the following returns and corresponding probabilities for Asset D: Rate of Return Probability 10% 30% 15% 40% 20% 30% Compute for: a. Expected rate of return b. The standard deviation c. The coefficient of variationarrow_forwardGiven the following probability distribution of returns: Probability Return 0.1 -15.0% 0.25 0.0% 0.3 8.5% 0.25 12.0% 0.1 32.0% what is the expected return?arrow_forward

- Possible returns and their probabilities for an asset is given in the table below. The expected return is 30.25%. Calculate the standard deviation of the asset's return. Probability 0.40 0.45 0.15 13.92% O 17.84 % 18.55% O 19.09% 16.59% Return 0.52 0.17 0.12arrow_forwardAn asset has normally-distributed returns, with mean of 10.6% and standard deviation of 14.8%. What is the 2% VaR (value at risk) return? Enter answer in percents.arrow_forwardSuppose the gain from an investment is a normal random variable with mean 2 and standard deviation1.25. Compute the VaR for this investment.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Portfolio return, variance, standard deviation; Author: MyFinanceTeacher;https://www.youtube.com/watch?v=RWT0kx36vZE;License: Standard YouTube License, CC-BY