ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:Question Help

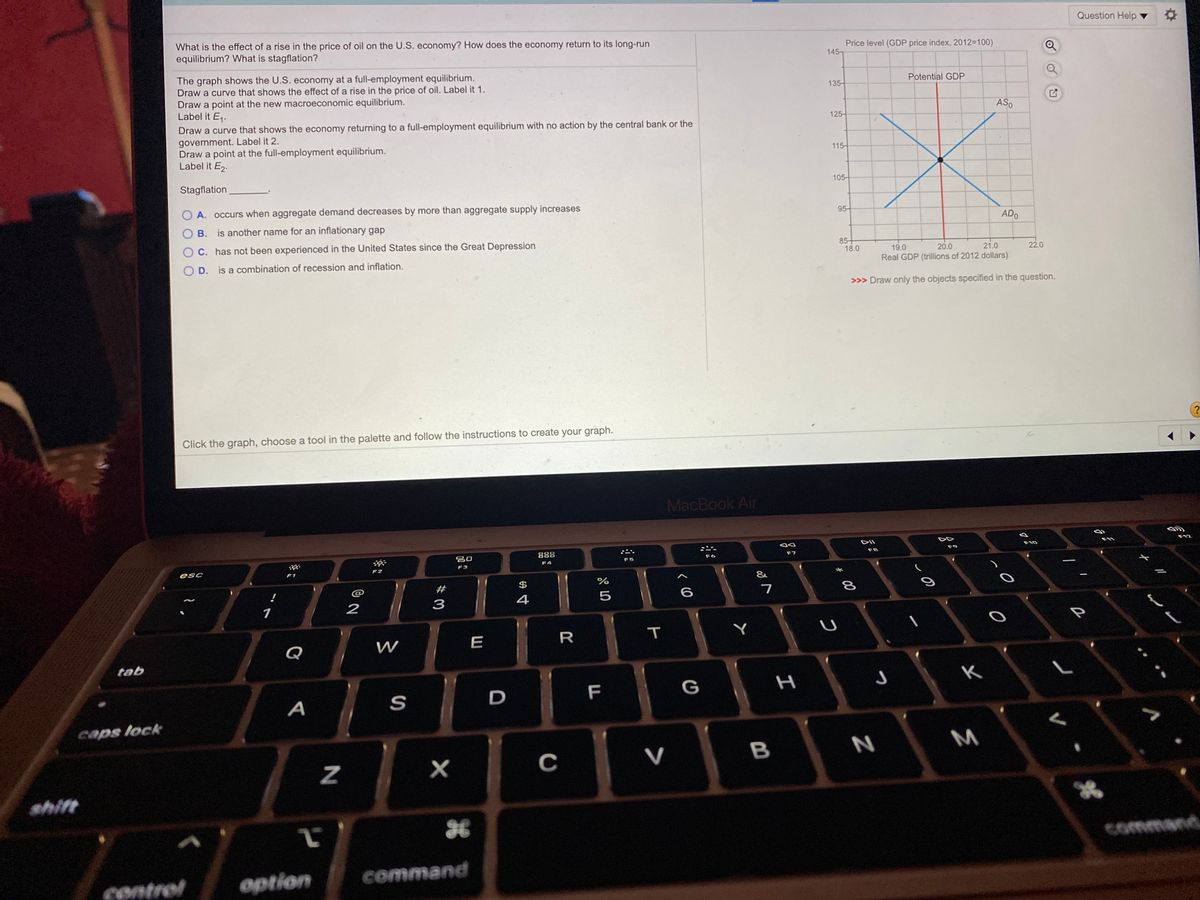

What is the effect of a rise in the price of oil on the U.S. economy? How does the economy return to its long-run

equilibrium? What is stagflation?

Price level (GDP price index, 2012=D100)

145-

The graph shows the U.S. economy at a full-employment equilibrium.

Draw a curve that shows the effect of a rise in the price of oil. Label it 1.

Draw a point at the new macroeconomic equilibrium.

Label it E1.

Potential GDP

135-

ASO

Draw a curve that shows the economy returning to a full-employment equilibrium with no action by the central bank or the

125-

government. Label it 2.

Draw a point at the full-employment equilibrium.

Label it E2.

115-

Stagflation

105-

O A. occurs when aggregate demand decreases by more than aggregate supply increases

95-

O B. is another name for an inflationary gap

ADO

O C. has not been experienced in the United States since the Great Depression

85-

18.0

19.0

20.0

21.0

22.0

O D. is a combination of recession and inflation.

Real GDP (trillions of 2012 dollars)

>>> Draw only the objects specified in the question.

Click the graph, choose a tool in the palette and follow the instructions to create your graph.

MacBook Air

DII

F12

吕口

888

F10

F9

F7

F8

F5

F4

F3

esc

F2

F1

&

#

$

%

!

8

4

1

2

P

E

R

Y

Q

tab

S

D

F

G

caps lock

V

B

M

C

shift

command

contrel

option

command

.の

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- On the following graph, use the purple line (diamond symbol) to plot this economy's long-run aggregate supply (LRAS) curve. Then use the orange line segments (square symbol) to plot the economy's short-run aggregate supply (AS) curve at each of the following price levels: 100, 105, 110, 115, and 120. PRICE LEVEL 125 120 115 + 110 105 100 95 90 85 80 75 0 10 20 30 40 50 60 70 OUTPUT (Billions of dollars) 80 90 100 0 AS LRAS ? The short-run quantity of output supplied by firms will fall short of the natural level of output when the actual price level level that people expected. the pricearrow_forwardThe following graph shows an economy's short-run aggregate supply curve (SRAS), current equilibrium aggregate price level (P₁), and real GDP ( Q₁). The economy currently has Natural Real GDP (QN) of $8 trillion. Use this information to place the orange long-run aggregate supply curve (LRAS, square symbols) in the correct position on the graph. PRICE LEVEL 10 P₁ 8 2 0 0 2 4 6 8 10 REAL GDP (Trillions of dollars) SRAS 12 Q₁ 14 LRASarrow_forwardSuppose firms become very optimistic about future business conditions and invest heavily in new capital equipment. (a) Draw an AD-AS diagram to show the short-run effect of this optimism on the economy. Label the new levels of prices and output. (b) Use the diagram from part (a) to show the new long-run equilibrium of the economy. Explain in words why how the new long-run equilibrium is achieved.arrow_forward

- The following graph shows the aggregate demand (AD) and aggregate supply (AS) curves for the United States in 1941. Shift one of the curves on the following graph to illustrate the effect of increased U.S. government spending during World War II.arrow_forwardThe graphs illustrate an initial equilibrium for some economy. Suppose that the economy experiences a rise in aggregate demand. Use the graphs to illustrate the new positions of AD, SRAS, and LRAS as well as the new short-run and long-run equilibria resulting from this change. Short-Run Graph Long-Run Graph LRAS LRAS SRAS SRAS Equilibrium point Equilibrium point AD AD Real GDP Real GDP Aggregate price level Aggregate price levelarrow_forwardNow adjust the graph to show the new long-run equilibrium. What causes the economy to move from its short-run equilibrium to its long-run equilibrium? The government increases taxes to curb aggregate demand. Nominal wages, prices, and perceptions adjust downward to this new price level. O Nominal wages, prices, and perceptions adjust upward to this new price level. O The government increases spending to increase aggregate demand. Which of the following is true according to the sticky-wage theory of aggregate supply as a result of the decrease in the money supply? Check all that apply. Nominal wages at the initial equilibrium are equal to nominal wages at the new short-run equilibrium. Nominal wages at the initial equilibrium are greater than nominal wages at the new long-run equilibrium. Real wages at the initial equilibrium are greater than real wages at the new short-run equilibrium. Real wages at the initial equilibrium are equal to real wages at the new long-run equilibrium.…arrow_forward

- 9arrow_forwardThe following graph shows the aggregate demand (AD) curve in a hypothetical economy. At point A, the price level is 140, and the quantity of output demanded is $300 billion. Moving down along the aggregate demand curve from point A to point B, the price level falls to 120, and the quantity of output demanded rises to $500 billion. 170 100 180 140 130 120 110 AD 100 00 100 200 300 400 B00 700 OUTPUT (Billians of dollars) As the price level falls, the cost of borrowing money will , causing the quantity of output demanded to Additionally, as the price level falls, the impact on the domestic interest rate will cause the real value of the dollar to in foreign exchange markets. The number of domestic products purchased by foreigners (exports) will therefore and the number of foreign products purchased by domestic consumers and firms (imports) will Net exports will therefore causing the quantity of domestic output demanded toarrow_forwardConsider the long-run equilibrium output, the potential output, the full-employment output, and the natural rate of output. Are their output levels the same or different?arrow_forward

- On the following graph, use the black point (cross symbol) to show the short-run equilibrium. Then use the grey point (star symbol) to show the long- run equilibrium. PRICE LEVEL 120 110 100 1 LRAS REAL GOP In the short run, the price level is Natural Real GDP SRAS, SRAS, AD SRAS, AD AD₂ and Real GDP is ++ Short-Run Equilibrium ✡ Long-Run Equilibrium ? Natural Real GDP. In the long run, the price level is and Real GDP is Aarrow_forwardThe uncertainty surrounding the COVID-19 pandemic led firms to reduce their desired investment in 2020. What are the short-run and long run effects on the equilibrium price and output levels? Please explain in words.arrow_forwardSuppose the people of Canada has reduced their spending on goods and services from the United States. What will be the effect on real GDP and the price level in the short run? In the long run? Show your results graphically.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education