ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

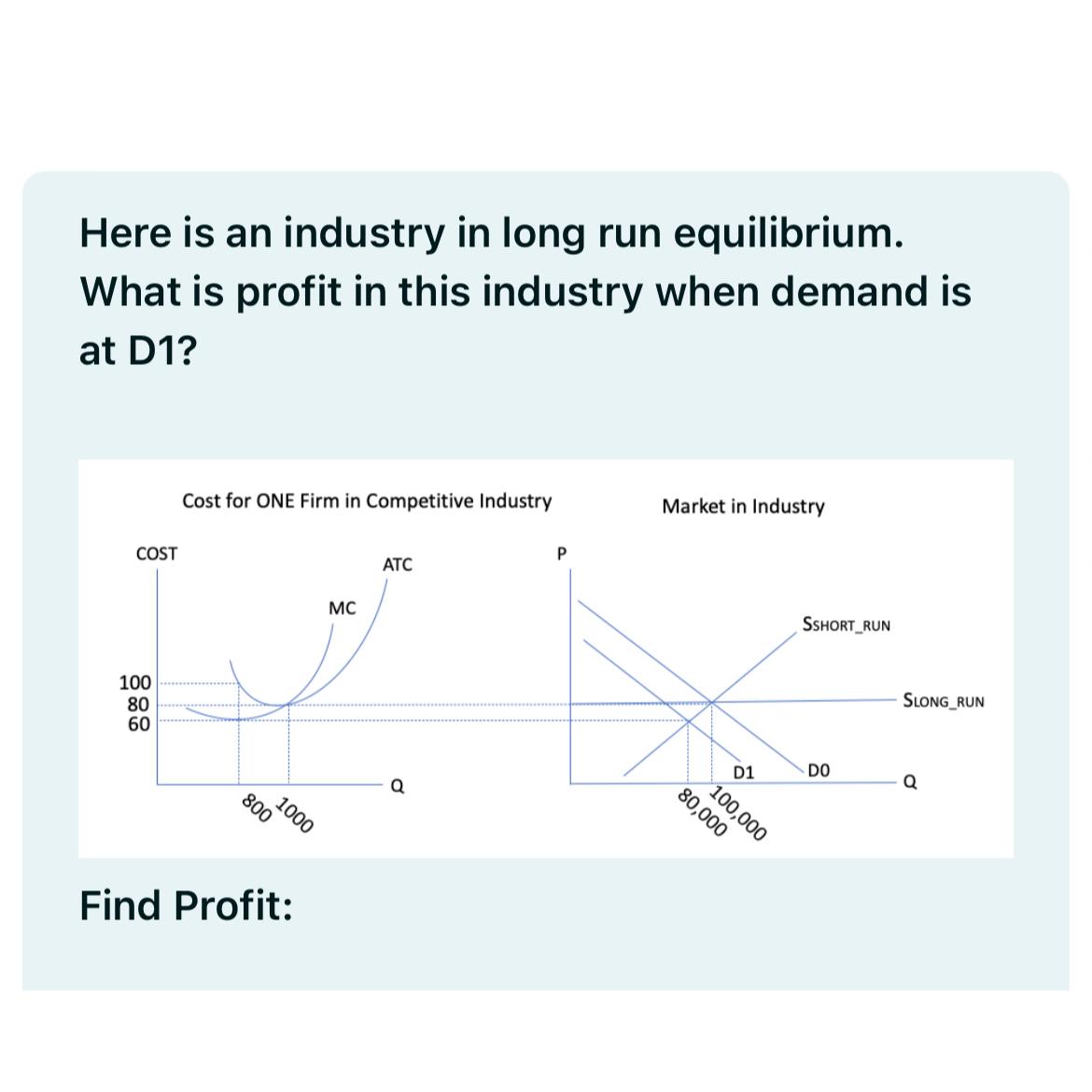

Transcribed Image Text:Here is an industry in long run equilibrium.

What is profit in this industry when demand is

at D1?

COST

100

80

60

Cost for ONE Firm in Competitive Industry

800

1000

Find Profit:

MC

ATC

Q

P

Market in Industry

D1

100,000

80,000

SSHORT RUN

DO

SLONG RUN

O

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Required information The following figure shows the costs for a perfectly competitive producer: AVC, ATC, MC $46 235 30 25 20 15 10 5 0 MC 10 20 30 40 50 60 70 80 90 100 ATC AVC Output per period Refer to the above figure to answer this question. If the price of the product is $10, what is the profit-maximizing (or loss-minimizing) output?arrow_forwardQuestion 12 Examine the graph below. Assume this firm is producing at its profit-maximizing output. In the long run, if prices remain as shown here, this firm will SA MC ATC 13 12 11 10 AVC 6 6 0 3 8 0 12 15 18 21 q stay in the market and make a profit have zero economic profit O exit the market shut down have losses equal to fixed costs 9 B 7arrow_forwardMICROECONOMICS - PROBLEM SET 4 MARKET STRUCTURE 1. The inverse demand curve for the product of a perfectly competi- tive industry is given by P = 160-0.5Q, where P is the price per unit and Q is the quantity. The short-run industry inverse supply curve (for a given number of firms) is P = 100+ 0.25Q. (a) Calculate the equilibrium price and quantity, and hence cal- culate the consumers' surplus and producers' surplus. A tax of 15 per unit sold is now imposed on every unit sold. Calculate the new short-run equilibrium price (including tax) and quantity, and hence calculate the revenue raised. What is the deadweight loss (excess burden) of the tax?arrow_forward

- t of 40 40 35 55 30 25 25 20 15 10 5 MC, AC MC AC 9 0 100 200 300 400 500 The graph shows average and marginal cost curves for a typical firm in a perfectly competitive industry in LONG-RUN equilibrium. The long-run equilibrium price of the product is $ In long-run equilibrium the firm will produce units. In long-run equilibrium the firm will earn $ economic profit.arrow_forward$11.00 MC| $10.00 $9.00 ATC $8.00 $7.00 TRAVCI $6.00 $5.00 $4.00 $3.00 2 3 7 9 10 Quantity of Output (q) Pierre is a photographer in a perfectly competitive market. The graph shown above gives his MC, ATC and AVC curves. Suppose the market price is $10.50. How much profit does Pierre make? 22.5 24 20 O18 S per unitarrow_forwardA firm on competitive market has the data about cost as below Q,0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14 TC 100160208254290320340355370390430475525580640 a. Form a table with numbers about: total revenue, average cost, average variable cost and marginal cost of this firm. Determine the quantity that this firm will shutdown b. To maximize the profit, what will be the output of this firm if the price of product is 45 and if the price is 50. c. Determine the supply curve of this firm 3. A firm on competitive market has the data about cost as below Q 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 TC 100 160 208 254 290 320 340 355 370 390 430 475 525 580 640 a. Form a table with numbers about: total revenue, average cost, average variable cost and marginal cost of this firm. Determine the quantity that this firm will shutdown b. To maximize the profit, what will be the output of this firm if the price of product is 45 and if the price is 50. C. Determine the supply curve of this firmarrow_forward

- At the marketplace $8 per bushel.....please answerarrow_forwardThe figure is not finished but how will you draw the long run equilbirum at the price of $100 on this?arrow_forwardt of 35 45 40 30 25 255 15 20 10 5 MC, AC MC AC 9 0 100 200 300 400 500 The graph shows average and marginal cost curves for a typical firm in a perfectly competitive industry in LONG-RUN equilibrium. The long-run equilibrium price of the product is $ In long-run equilibrium the firm will produce units. In long-run equilibrium the firm will earn $ economic profit.arrow_forward

- The graph below depicts the cost curves faced by all firms in a particular industry. While the second graph show the total market demand (in thousands). Initially there are 500 firms. 10 B N 5 20 40 60 80 100 120 140 160 180 200 9 50 100 150 200 250 300 350 400 450 500 Demand in thousands What is the SR profit per firm? -80 240 0300 400arrow_forwardI don't need your AI answer plsarrow_forwardPlease answer fast please arjent help pleasearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education