Videos

Multiple Products. Materials, and Processes

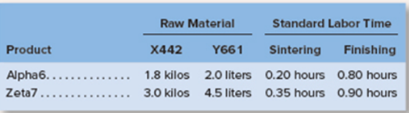

Mickley Corporation produces two products. Alpha’s and Zeta’s, which pass through two operations. Sintering and

Finishing. Each of the products uses two raw materials−X442 and Y661. The company uses a

Information relating to materials purchased and materials used in production during May follows:

The following additional information is available:

a. The company recognizes price variances when materials are purchased.

b. The standard labor rate is $19.80 per hour in Sintering and $19.20 per hour in Finishing.

c. During May, 1,200 direct labor-hours were worked in Sintering at a total labor cost of $27,000, and 2,850 direct labor-hours were worked in Finishing at a total labor cost of $59.850.

d. Production during May was 1,500 Alpha6s and 2.000 Zeta7s.

Required:

1. Prepare a standard cost card for each product, showing the standard cost of direct materials and direct labor.

2. Compute the materials price and quantity variances for each material.

3. Compute the labor rate and efficiency variances for each operation.

.

1

Standard cost card

A standard cost card contains all the information regarding standard quantities, rates, hours etc. It shows total cost of producing one unit.

To prepare: Standard cost card for both the given products, showing cost of direct materials and labor.

Answer to Problem 21P

Total standard cost of alpha6s is determined as $28.42 and of zeta7s is $41.01.

Explanation of Solution

Standard cost card of Alpha6s:

| Particulars | Standard Quantity or standard hours | Standard price or standard rate | Standard cost (in $) | ||

| Direct material (X442) | 1.8 | Kilos | $3.5 | Per kilo | 6.3 |

| Direct material (Y661) | 2.0 | Liters | $1.4 | Per liter | 2.8 |

| Direct labor (Sintering) | 0.2 | Hours | $19.8 | Per hour | 3.96 |

| Direct labor (Finishing) | 0.8 | Hours | $19.2 | Per hour | 15.36 |

| Total | 28.42 | ||||

Standard cost card of zeta7s:

| Particulars | Standard Quantity or standard hours | Standard price or standard rate | Standard cost (in $) | ||

| Direct material (X442) | 3.0 | Kilos | $3.5 | Per kilo | 10.5 |

| Direct material (Y661) | 4.5 | Liters | $1.4 | Per liter | 6.3 |

| Direct labor (Sintering) | 0.35 | Hours | $19.8 | Per hour | 6.93 |

| Direct labor (Finishing) | 0.9 | Hours | $19.2 | Per hour | 17.28 |

| Total | 41.01 | ||||

So, total standard cost of Alpha6s is $28.42 and of zeta7s is $41.01.

2

Variances

A variance shows difference between actual amount of cost incurred and the budgeted cost. Variances can either be favorable or unfavorable.

To calculate: Amount of material price variance and quantity variance.

Answer to Problem 21P

Material price variance for material X442 is $1,450 unfavorable and for material Y661 is $775 favorable.

material quantity variance for material X442 is $700 favorable and for material Y661 is $1,400 unfavorable.

Explanation of Solution

Formula to calculate material price variance is:

For material X442, actual price will be:

Standard price is given as $3.5 per kilo and actual quantity purchased is 14,500. So, material price variance will be:

For material Y661, actual price will be:

Standard price is given as $1.4 per liter and actual quantity purchased is 15,500. So, material price will be:

Formula to calculate material quantity variance is:

For material X442, actual quantity is given as 8,500 kilos and standard price is $3.5 per kilo. Standard quantity will be calculated as:

So, Material quantity variance will be:

For material Y661, actual quantity is given as 13,000 liters and standard price is $1.4 per liter. Standard quantity will be calculated as:

So, material quantity variance will be:

3

Variances

Variances related to labor show difference among actual cost incurred on labor and the standard cost. Variances are considered favorable when standard cost is more than that of actual cost.

Amount of labor rate and efficiency variances.

Answer to Problem 21P

Labor rate variance for sintering is $3,240 unfavorable and for finishing is $5,130 unfavorable.

Labor efficiency variance for sintering is $3,960 unfavorable and for finishing is $2,880 favorable.

Explanation of Solution

Formula to calculate labor rate variance is:

For sintering, standard rate is $19.80 per hour, actual hours worked are 1,200 and actual rate will be $22.5 per hour ($27,000/1,200). Labor rate variance will be:

For finishing, standard rate is $19.20 per hour, actual hours worked are 2,850 and actual rate will be $21 per hour ($59,850/2,850). So, labor rate variance will be:

Formula to calculate labor efficiency variance is:

For sintering, actual hours are 1,200, standard rate is $19.8 and standard hours will be 1,000 ((0.2*1,500)+(0.35*2,000)). So, the labor efficiency variance will be:

For finishing, actual hours are 2,850, standard rate is $19.2 and standard hours will be 3,000 ((0.8*1,500 + 0.9*2,000))

Want to see more full solutions like this?

Chapter 9 Solutions

Introduction To Managerial Accounting

- Medical Tape makes two products: Generic and Label. It estimates it will produce 423,694 units of Generic and 652,200 of Label, and the overhead for each of its cost pools is as follows: It has also estimated the activities for each cost driver as follows: How much is the overhead allocated to each unit of Generic and Label?arrow_forwardCicleta Manufacturing has four activities: receiving materials, assembly, expediting products, and storing goods. Receiving and assembly are necessary activities; expediting and storing goods are unnecessary. The following data pertain to the four activities for the year ending 20x1 (actual price per unit of the activity driver is assumed to be equal to the standard price): Required: 1. Prepare a cost report for the year ending 20x1 that shows value-added costs, non-value-added costs, and total costs for each activity. 2. Explain why expediting products and storing goods are non-value-added activities. 3. What if receiving cost is a step-fixed cost with each step being 1,500 orders whereas assembly cost is a variable cost? What is the implication for reducing the cost of waste for each activity?arrow_forwardKenkel, Ltd. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 80,000. b. Requisitioned raw materials to production, 80,000. c. Distributed direct labor costs, 10,000. d. Factory overhead costs incurred, 60,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 225,000, on account.arrow_forward

- Cassien Inc. manufactures products that pass through two or more processes. During June, equivalent units were computed using the weighted average method: Required: 1. Calculate the unit cost for June using the weighted average method. 2. Using the weighted average method, determine the cost of EWIP and the cost of the goods transferred out. 3. CONCEPTUAL CONNECTION Cassien had just finished implementing a series of measures designed to reduce the unit cost to 2.00 and was assured that this had been achieved and should be realized for Junes production. Yet, upon seeing the unit cost for June, the president of the company was disappointed. Can you explain why the full effect of the cost reductions may not show up in June? What can you suggest to overcome this problem?arrow_forwardGeneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forwardDavis Co. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 70,000. b. Requisitioned raw materials to production, 70,000. c. Distributed direct labor costs, 15,000. d. Factory overhead costs incurred, 45,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 195,000, on account. (Hint: Use a single account for raw materials and work in process.)arrow_forward

- A manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardThe following product costs are available for Kellee Company on the production of eyeglass frames: direct materials, $32,125; direct labor, $23.50; manufacturing overhead, applied at 225% of direct labor cost; selling expenses, $22,225; and administrative expenses, $31,125. The direct labor hours worked for the month are 3,200 hours. A. What are the prime costs? B. What are the conversion costs? C. What is the total product cost? D. What is the total period cost? E. If 6.425 equivalent units are produced, what is the equivalent material cost per unit? F. What is the equivalent conversion cost per unit?arrow_forwardPetrillo Company produces engine parts for large motors. The company uses a standard cost system for production costing and control. The standard cost sheet for one of its higher volume products (a valve) is as follows: During the year, Petrillo had the following activity related to valve production: a. Production of valves totaled 20,600 units. b. A total of 135,400 pounds of direct materials was purchased at 5.36 per pound. c. There were 10,000 pounds of direct materials in beginning inventory (carried at 5.40 per pound). There was no ending inventory. d. The company used 36,500 direct labor hours at a total cost of 656,270. e. Actual fixed overhead totaled 110,000. f. Actual variable overhead totaled 168,000. Petrillo produces all of its valves in a single plant. Normal activity is 20,000 units per year. Standard overhead rates are computed based on normal activity measured in standard direct labor hours. Required: 1. Compute the direct materials price and usage variances. 2. Compute the direct labor rate and efficiency variances. 3. Compute overhead variances using a two-variance analysis. 4. Compute overhead variances using a four-variance analysis. 5. Assume that the purchasing agent for the valve plant purchased a lower-quality direct material from a new supplier. Would you recommend that the company continue to use this cheaper direct material? If so, what standards would likely need revision to reflect this decision? Assume that the end products quality is not significantly affected. 6. Prepare all possible journal entries (assuming a four-variance analysis of overhead variances).arrow_forward

- Roberts Company produces two weed eaters: basic and advanced. The company has four activities: machining, engineering, receiving, and inspection. Information on these activities and their drivers is given below. Overhead costs: Required: 1. Calculate the four activity rates. 2. Calculate the unit costs using activity rates. Also, calculate the overhead cost per unit. 3. What if consumption ratios instead of activity rates were used to assign costs instead of activity rates? Show the cost assignment for the inspection activity.arrow_forwardActivity-based product costing Sweet Sugar Company manufactures three products (white sugar, brown sugar, and powdered sugar) in a continuous production process. Senior management has asked the controller to conduct an activity-based costing study. The controller identified the amount of factory overhead required by the critical activities of the organization as follows: The activity bases identified for each activity are as follows: The activity-base usage quantities and units produced for the three products were determined from corporate records and are as follows: Each product requires 0.5 machine hour per unit. Instructions Determine the activity rate for each activity. Determine the total and per-unit activity cost for all three products. Round to nearest cent. Why arent the activity unit costs equal across all three products since they require the same machine time per unit?arrow_forwardFor E2-17, prepare any journal entries that would have been different if the only trigger points had been the purchase of materials and the sale of finished goods. Davis Co. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 70,000. b. Requisitioned raw materials to production, 70,000. c. Distributed direct labor costs, 15,000. d. Factory overhead costs incurred, 45,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 195,000, on account. (Hint: Use a single account for raw materials and work in process.)arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,