Managerial Accounting: The Cornerstone of Business Decision-Making

7th Edition

ISBN: 9781337115773

Author: Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 6, Problem 45E

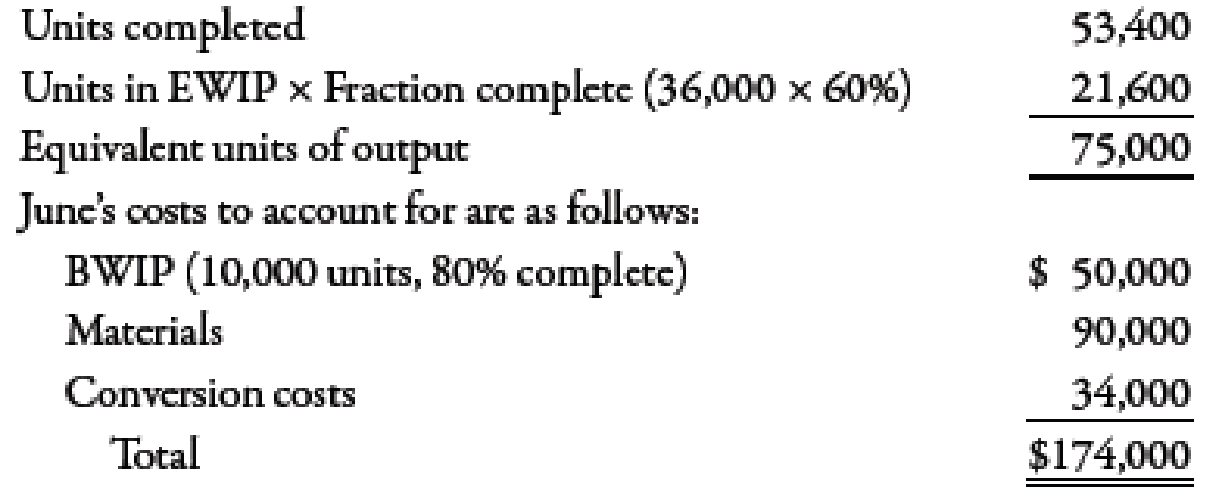

Cassien Inc. manufactures products that pass through two or more processes. During June, equivalent units were computed using the weighted average method:

Required:

- 1. Calculate the unit cost for June using the weighted average method.

- 2. Using the weighted average method, determine the cost of EWIP and the cost of the goods transferred out.

- 3. CONCEPTUAL CONNECTION Cassien had just finished implementing a series of measures designed to reduce the unit cost to $2.00 and was assured that this had been achieved and should be realized for June’s production. Yet, upon seeing the unit cost for June, the president of the company was disappointed. Can you explain why the full effect of the cost reductions may not show up in June? What can you suggest to overcome this problem?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Step by step answer

I need this question answer general accounting question

Assets turnover??

Chapter 6 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

Ch. 6 - Describe the differences between process costing...Ch. 6 - Prob. 2DQCh. 6 - What are the similarities in and differences...Ch. 6 - Prob. 4DQCh. 6 - How would process costing for services differ from...Ch. 6 - How does the adoption of a JIT approach to...Ch. 6 - What are equivalent units? Why are they needed in...Ch. 6 - Under the weighted average method, how are...Ch. 6 - Prob. 9DQCh. 6 - Prob. 10DQ

Ch. 6 - Prob. 11DQCh. 6 - How is the equivalent unit calculation affected...Ch. 6 - Prob. 13DQCh. 6 - Prob. 14DQCh. 6 - Process costing works well whenever a....Ch. 6 - Job-order costing works well whenever a....Ch. 6 - Prob. 3MCQCh. 6 - To record the transfer of costs from a prior...Ch. 6 - The costs transferred from a prior process to a...Ch. 6 - During the month of May, the grinding department...Ch. 6 - Use the following information for Multiple-Choice...Ch. 6 - Use the following information for Multiple-Choice...Ch. 6 - Use the following information for Multiple-Choice...Ch. 6 - During May, Kimbrell Manufacturing completed and...Ch. 6 - During June, Kimbrell Manufacturing completed and...Ch. 6 - For August, Kimbrell Manufacturing has costs in...Ch. 6 - For September, Murphy Company has manufacturing...Ch. 6 - During June, Faust Manufacturing started and...Ch. 6 - During July, Faust Manufacturing started and...Ch. 6 - Assume for August that Faust Manufacturing has...Ch. 6 - For August, Lanny Company had 25,000 units in...Ch. 6 - When materials are added either at the beginning...Ch. 6 - With nonuniform inputs, the cost of EWIP is...Ch. 6 - Transferred-in goods are treated by the receiving...Ch. 6 - Basic Cost Flows Gardner Company produces 18-ounce...Ch. 6 - Equivalent Units, No Beginning Work in Process...Ch. 6 - Unit Cost, Valuing Goods Transferred Out and EWIP...Ch. 6 - Weighted Average Method, Unit Cost, Valuing...Ch. 6 - Physical Flow Schedule Golding Inc. just finished...Ch. 6 - Production Report, Weighted Average Manzer Inc....Ch. 6 - Nonuniform Inputs, Weighted Average Carter Inc....Ch. 6 - Transferred-In Cost Powers Inc. produces a protein...Ch. 6 - Use the following information for Brief Exercises...Ch. 6 - Use the following information for Brief Exercises...Ch. 6 - Basic Cost Flows Hardy Company produces 18-ounce...Ch. 6 - Equivalent Units, No Beginning Work in Process...Ch. 6 - Unit Cost, Valuing Goods Transferred Out and EWIP...Ch. 6 - Weighted Average Method, Unit Cost, Valuing...Ch. 6 - Physical Flow Schedule Craig Inc. just finished...Ch. 6 - Production Report, Weighted Average Washburn Inc....Ch. 6 - Nonuniform Inputs, Weighted Average Ming Inc. had...Ch. 6 - Transferred-In Cost Vigor Inc. produces an energy...Ch. 6 - Use the following information for Brief Exercises...Ch. 6 - Use the following information for Brief Exercises...Ch. 6 - Basic Cost Flows Linsenmeyer Company produces a...Ch. 6 - Journal Entries, Basic Cost Flows In December,...Ch. 6 - Equivalent Units, Unit Cost, Valuation of Goods...Ch. 6 - Weighted Average Method, Equivalent Units Goforth...Ch. 6 - Cassien Inc. manufactures products that pass...Ch. 6 - Weighted Average Method, Unit Costs, Valuing...Ch. 6 - Physical Flow Schedule The following information...Ch. 6 - Physical Flow Schedule Nelrok Company manufactures...Ch. 6 - Production Report, Weighted Average Mino Inc....Ch. 6 - Nonuniform Inputs, Equivalent Units Terry Linens...Ch. 6 - Unit Cost and Cost Assignment, Nonuniform Inputs...Ch. 6 - Nonuniform Inputs, Transferred-In Cost Drysdale...Ch. 6 - Transferred-In Cost Goldings finishing department...Ch. 6 - (Appendix 6A) First-In, First-Out Method;...Ch. 6 - (Appendix 6A) First-In, First-Out Method; Unit...Ch. 6 - Basic Flows, Equivalent Units Thayn Company...Ch. 6 - Steps in Preparing a Production Report Recently,...Ch. 6 - Recently, Stillwater Designs expanded its market...Ch. 6 - Equivalent Units, Unit Cost, Weighted Average...Ch. 6 - Production Report Refer to the information for...Ch. 6 - Mimasca Inc. manufactures various holiday masks....Ch. 6 - Use the following information for Problems 6-62...Ch. 6 - Use the following information for Problems 6-62...Ch. 6 - Weighted Average Method, Separate Materials Cost...Ch. 6 - Seacrest Company uses a process-costing system....Ch. 6 - Required: 1. Using the FIFO method, prepare the...Ch. 6 - Benson Pharmaceuticals uses a process-costing...Ch. 6 - (Appendix 6A) First-In, First-Out Method Refer to...Ch. 6 - Golding Manufacturing, a division of Farnsworth...Ch. 6 - AKL Foundry manufactures metal components for...Ch. 6 - Consider the following conversation between Gary...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Don't Use Aiarrow_forwardFinancial Accounting Question no. 2 : You own 560 shares of Maslyn Tours stock that sells for $64.57 per share. If the stock has a dividend yield of 3.7 percent, how much do you expect to receive next year in dividend income from this investment? a. $1,337.89 b. $1,382.49 c. $1,303.05 d. $1.486.54 e. $1,421.51arrow_forwardWhat is champion total assets turnover?arrow_forward

- Need help with this accounting questionsarrow_forwardAt the beginning of the year, Crane Ltd. had total assets of $710,000 and total liabilities of $400,000. If Crane's total assets decreased by $90,000 during the year and shareholders' equity increased by $125,000, what is the amount of total liabilities at the end of the year?arrow_forwardHi teacher please help me this question general accountingarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

Cost Accounting - Definition, Purpose, Types, How it Works?; Author: WallStreetMojo;https://www.youtube.com/watch?v=AwrwUf8vYEY;License: Standard YouTube License, CC-BY