Concept explainers

Videos

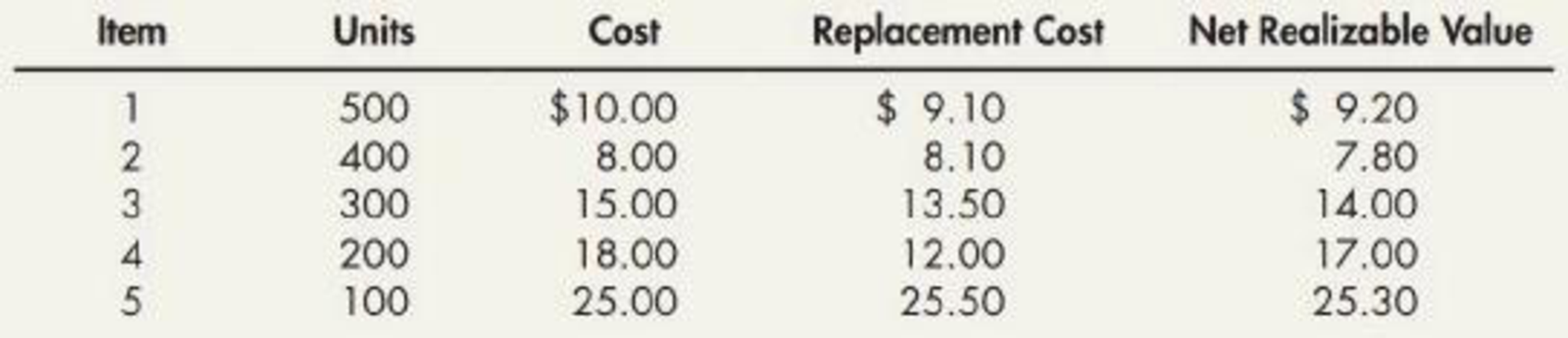

Inventory Write-Down Palmquist Company has five different inventory items and applies the

Required:

- 1. Assume that Palmquist uses the FIFO cost flow assumption. Compute the correct inventory value under the lower of cost or net realizable value rule.

- 2. Assume that Palmquist uses the LIFO cost flow assumption. Compute the correct inventory value under the lower of cost or market rule.

- 3. Assume that Palmquist uses IFRS. Compute the correct inventory value under the lower of cost or net realizable value rule.

- 4. Next Level Explain the differences between the inventory valuations reported under IFRS and U.S. GAAP.

1.

Calculate the correct value of inventory under LCM or NRV rule (if P uses FIFO method).

Explanation of Solution

Inventory Write-Downs: If the utilizing capacity of inventory by the company drops down below the acquisition cost of inventory, the inventory write-downs occur.

The following are the two situations for the inventory write-downs:

- When the inventory is damaged or is in non-salable state

- When the market value of inventory has dropped below the acquisition cost

FIFO: Under this inventory method, the units that are purchased first are sold first. Thus, it starts from the selling of the beginning inventory, followed by the units purchased in a chronological order of their purchases took place during a particular period.

Calculate the correct value of inventory under LCM or NRV rule (if P uses FIFO method):

If FIFO method is used:

| Case | Cost | Net realizable value | Lower of cost or NRV | |

| ($) | ($) | ($) | ||

| 1 | 10.00 | 9.20 | 9.20 | (NRV) |

| 2 | 8.00 | 7.80 | 7.80 | (NRV) |

| 3 | 15.00 | 14.00 | 14.00 | (NRV) |

| 4 | 18.00 | 17.00 | 17.00 | (NRV) |

| 5 | 25.00 | 25.30 | 25.00 | (Cost) |

Table (1)

If LCNRV rule is used:

| Item | Units | Valuation | Total |

| 1 | 500 | 9.20 | 4,600 |

| 2 | 400 | 7.80 | 3,120 |

| 3 | 300 | 14.00 | 4,200 |

| 4 | 200 | 17.00 | 3,400 |

| 5 | 100 | 25.00 | 2,500 |

| Total inventory valuation | $17,820 | ||

Table (2)

2.

Calculate the correct value of inventory under LCM or NRV rule (if P uses LIFO method).

Explanation of Solution

LIFO: Under this inventory method, the units that are purchased last are sold first. Thus, it starts from the selling of the units recently purchased and ending with the beginning inventory.

Calculate the correct value of inventory under LCM or NRV rule (if P uses LIFO method):

If LIFO method is used:

| Case | Cost | Replacement | NRV | NRV less normal profit margin | Lower of cost or Market |

| ($) | ($) | ($) | ($) | ($) | |

| 1 | 10.00 | 9.10 | 9.20 | 7.20 | 9.10 |

| 2 | 8.00 | 8.10 | 7.80 | 6.20 | 7.80 |

| 3 | 15.00 | 13.50 | 14.00 | 11.00 | 13.50 |

| 4 | 18.00 | 12.00 | 17.00 | 13.40 | 13.40 |

| 5 | 25.00 | 25.50 | 25.30 | 20.30 | 25.00 |

Table (3)

If LCM rule is used:

| Item | Units | Valuation | Total |

| 1 | 500 | 9.10 | 4,550 |

| 2 | 400 | 7.80 | 3,120 |

| 3 | 300 | 13.50 | 4,050 |

| 4 | 200 | 13.40 | 2,680 |

| 5 | 100 | 25.00 | 2,500 |

| Total inventory valuation | $16,900 | ||

Table (4)

Working note 1:

Calculate NRV less profit margin for item 1.

Working note 2:

Calculate NRV less profit margin for item 2.

Working note 3:

Calculate NRV less profit margin for item 3.

Working note 4:

Calculate NRV less profit margin for item 4.

Working note 5:

Calculate NRV less profit margin for item 5.

3.

Calculate the correct value of inventory under lower of cost or market rule (If P uses IFRS):

Explanation of Solution

Lower-of-cost-or-market: The lower-of-cost-or-market (LCM) is a method which requires the reporting of the ending merchandise inventory in the financial statement of a company, either at current market value or at historical cost price of the inventory, whichever is less.

If P uses IFRS:

| Item | Cost | NRV | LCM | |

| ($) | ($) | ($) | ||

| 1 | 10.00 | 9.20 | 9.20 | (NRV) |

| 2 | 8.00 | 7.80 | 7.80 | (NRV) |

| 3 | 15.00 | 14.00 | 14.00 | (NRV) |

| 4 | 18.00 | 17.00 | 17.00 | (NRV) |

| 5 | 25.00 | 25.30 | 25.00 | (Cost) |

Table (5)

If LCNRV rule is used:

| Item | Units | Valuation | Total |

| (a) | (b) | (c = a*b) | |

| 1 | 500 | 9.20 | 4,600 |

| 2 | 400 | 7.80 | 3,120 |

| 3 | 300 | 14.00 | 4,200 |

| 4 | 200 | 17.00 | 3,400 |

| 5 | 100 | 25.00 | 2,500 |

| Total inventory value | $17,820 | ||

Table (6)

4.

Describe the difference between the inventory valuation under U.S. GAAP and IFRS.

Explanation of Solution

Differences between the inventory valuation under U.S. GAAP and IFRS:

- If FIFO method is used, there would not be any difference between IFRS and U.S GAAP. However, the use of LIFO is not allowed by IFRS.

- Hence, IFRS would show the result in market value corresponding to the inventory valuation which is greater than the U.S. GAAP.

- FIFO method will result in lower inventory cost in the balance sheet relative to LIFO. As the inventory price is increasing, the inventory purchased last will have higher price than the inventory purchased first. Thus, under this method, the inventory purchased last with higher price will be sold first, thereby increasing the cost of goods sold. However, FIFO method gives lowest cost of goods sold and highest ending inventory since cost of goods are lower in the beginning because purchases are at lower rate and ending inventory is highest as the ending purchases are at higher rate.

Want to see more full solutions like this?

Chapter 8 Solutions

Intermediate Accounting: Reporting And Analysis

- Inventory Write-Down Stiles Corporation uses the FIFO cost flow assumption and is in the process of applying the LCNRV rule for each of two products in its ending inventory. A profit margin of 30% on the selling price is considered normal for each product. Specific data for each product are as follows:arrow_forwardInventory Costing Methods Crandall Distributors uses a perpetual inventory system and has the following data available for inventory, purchases, and sales for a recent year. Required: 1. Compute the cost of ending inventory and the cost of goods sold using the specific identification method. Assume the ending inventory is made up of 40 units from beginning inventory, 30 units from Purchase 1, 80 units from Purchase 2, and 40 units from Purchase 3. 2. Compute the cost of ending inventory and cost of goods sold using the FIFO inventory costing method. 3. Compute the cost of ending inventory and cost of goods sold using the LIFO inventory costing method. 4. Compute the cost of ending inventory and cost of goods sold using the average cost inventory costing method. ( Note: Use four decimal places for per-unit calculations and round all other numbers to the nearest dollar.) 5. CONCEPTUAL CONNECTION Compare the ending inventory and cost of goods sold computed under all four methods. What can you conclude about the effects of the inventory costing methods on the balance sheet and the income statement?arrow_forwardLower-of-cost-or market inventory Data on the physical inventory of Moyer Company as of December 31, 20Y9, are presented below. Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost and at the lower of cost or market, using the first-in, first-out method. Record the appropriate unit costs on an inventory sheet and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed below as an example.arrow_forward

- Retail method; gross profit method Selected data on inventory, purchases, and sales for Jaffe Co. and Coronado Co. are as follows: Instructions 1. Determine the estimated cost of the inventory of Jaffe Co. on February 28 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the inventory of Coronado Co. on October 31 by the gross profit method, presenting details of the computations. b. Assume that Coronado Co. took a physical inventory on October 31 and discovered that 366,500 of inventory was on hand. What was the estimated loss of inventory due to theft or damage during May through October?arrow_forwardInventory Write-Down Byron Company has five products in its inventory and uses the FIFO cost flow assumption. Specific data for each product are as follows: Required: 1. What is the correct inventory value, assuming the LCNRV rule is applied to each item of inventory? 2. What is the correct inventory value, assuming the LCNRV rule is applied to the total of inventory? 3. Next Level Comment on any differences that result from applying the LCNRV rule to individual items compared to the total of inventory.arrow_forwardLIFO and Inventory Pools On January 1, 2016, Grover Company changed its inventory cost flow method to the LIFO cost method from the FIFO cost method for its raw materials inventory. It made the change for both financial statement and income tax reporting purposes. Grover uses the multiple-pools approach under which it groups substantially identical raw materials into LIFO inventory pools. It uses weighted average costs in valuing annual incremental layers. The composition of the December 31, 2018, inventory for the Class F inventory pool is as follows: Inventory transactions for the Class F inventory pool during 2019 were as follows: On March 2, 2019, 4,800 units were purchased at a unit cost of 13.50 for 64,800. On September 1, 2019, 7,200 units were purchased at a unit cost of 14.00 for 100,800. A total of 15,000 units were used for production during 2019. The following transactions for the Class F inventory pool took place during 2020: On January 11, 2020, 7,500 units were purchased at a unit cost of 14.50 for 108,750. On May 14, 2020, 5,500 units were purchased at a unit cost of 15.50 for 85,250. On December 29, 2020, 7,000 units were purchased at a unit cost of 16.00 for 112,000. A total of 16,000 units were used for production during 2020. Required: 1. Prepare a schedule to compute the inventory (units and dollar amounts) of the Class F inventory pool at December 31, 2019. Show supporting computations in good form. 2. Prepare a schedule to compute the cost of Class F raw materials used in production for the year ended December 31, 2019. 3. Prepare a schedule to compute the inventory (units and dollar amounts) of the Class F inventory pool at December 31, 2020. Show supporting computations in good form.arrow_forward

- Discounts Nelson Company bought inventory for 50,000 on terms of 2/15, n/60. It pays for the first 37,500 of inventory purchased within the discount period and pays for the remaining 12,500 two months later. Required: 1. Prepare the journal entries to record the purchase and the payment under both the (a) gross price and (b) net price methods. Assume that Nelson uses the periodic inventory system. 2. Next Level Which of the two methods yields a conceptually preferable valuation of inventory?arrow_forwardInventory Valuation Specific identification method Weighted average cost method FIFO method LIFO method LIFO liquidation LIFO conformity rule LIFO reserve Replacement cost Inventory profit Lower-of-cost-or-market (LCM) rule Inventory turnover ratio Number of days sales in inventory Moving average (Appendix) The name given to an average cost method when a weighted average cost assumption is used with a perpetual inventory system. An inventory costing method that assigns the same unit cost to all units available for sale during the period. A conservative inventory valuation approach that is an attempt to anticipate declines in the value of inventory before its actual sale. An inventory costing method that assigns the most recent costs to ending inventory. The current cost of a unit of inventory. An inventory costing method that assigns the most recent costs to cost of goods sold. A measure of how long it takes to sell inventory. The IRS requirement that when LIFO is used on a tax return, it must also be used in reporting income to stockholders. An inventory costing method that relies on matching unit costs with the actual units sold. The portion of the gross profit that results from holding inventory during a period of rising prices. The result of selling more units than are purchased during the period, which can have negative tax consequences if a company is using LIFO. The excess of the value of a companys inventory stated at FIFO over the value stated at LIFO. A measure of the number of times inventory is sold during the period.arrow_forwardBlack Corporation uses the LIFO cost flow assumption. Each unit of its inventory has a net realizable value of 300, a normal profit margin of 35, and a current replacement cost of 250. Determine the amount per unit that should be used as the market value to apply the lower of cost or market rule to determine Blacks ending inventory.arrow_forward

- Calculate the cost of goods sold dollar value for B74 Company for the sale on November 20, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average (AVG).arrow_forwardCalculate the cost of goods sold dollar value for A74 Company for the sale on March 11, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average (AVG).arrow_forwardAnalyzing Inventory The recent financial statements of McLelland Clothing Inc. include the following data: Required: 1. Calculate McLellands gross profit ratio (rounded to two decimal places), inventory turnover ratio (rounded to three decimal places), and the average days to sell inventory (assume a 365-day year and round to two decimal places) using the FIFO inventory costing method. Be sure to explain what each ratio means. 2. Calculate McLellands gross profit ratio (rounded to two decimal places), inventory turnover ratio (rounded to three decimal places), and the average days to sell inventory (assume a 365-day year and round to two decimal places) using the LIFO inventory costing method. Be sure to explain what each ratio means. 3. CONCEPTUAL CONNECTION Which ratios-the ones computed using FIFO or LIFO inventory values-provide the better indicator of how successful McLelland was at managing and controlling its inventory?arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,  Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,