Concept explainers

Videos

Variable and Absorption Costing Unit Product Costs and Income Statements; Explanation of Difference in Net Operating Income L07—1, L07—2, L07—3

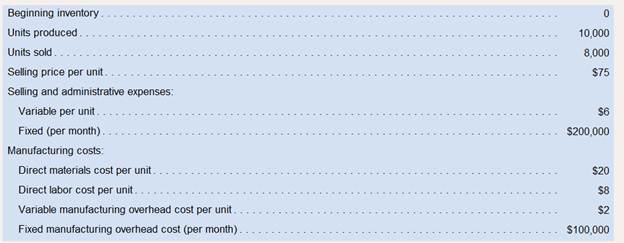

High Country, Inc., produces and sells many recreational products. The company has just opened a new plant to produce a folding camp cotthat will be marketed throughout the United States. The following cost and revenue data relate to May, the first month of the plant’s operation:

Management is anxious to assess the profitability of the new camp cot during the month of May.

Management is anxious to assess the profitability of the new camp cot during the month of May.

Required:

Assume that the company uses absorption costing.

a. Determine the unit product cost.

b. Prepare an income statement for May.

Assume that the company uses variable costing.

a. Determine the unit product cost.

b. Prepare a contribution format income statement for May.

Explain the reason for any difference in the ending inventory balances under the two costing methods and the impact of this differenceon reported net operating income.

Answer 1:

Absorption Costing: is also known as Full costing method. In this method, those costs which vary directly with production are considered in product cost. Also, fixed Manufacturing Expenses are treated as product cost only. Selling Expenses (since they do not vary with production), both variable and fixed, are charged off completely in the period in which the expenses get incurred.

Unit product Cost and Income statement for May.

Answer to Problem 20P

Solution:

| Computation of Unit Product Cost under Absorption Costing | |

| Particulars | Per unit cost |

| Direct Material | $ 20 |

| Direct Labour | $ 8 |

| Variable Manufacturing Overhead | $ 2 |

| Fixed Manufacturing Overhead | $ 27 |

| Total Product Cost | $ 57 |

| Income Statement under Absorption Costing | ||

| May | ||

| A | Sales(Sales Volume X Sales Price) | $ 600,000 |

| B | Less: Cost of Goods Sold | |

|

C | Beginning Inventory

Opening Inventory Quantity X Unit Product Cost of previous year | $ - |

| D | Add: Cost of Goods Manufactured

Production Quantity X Unit Product Cost | 570,000 |

| E | Less: Closing Inventory

Closing Inventory Quantity X Unit Product Cost of current year | $ 114,000 |

| B | Cost of Goods Sold (C+D-E) | $ 456,000 |

| F | Gross Margin (A - B) | $ 144,000 |

| G | Variable Selling & Admin Expenses

(Sales quantity X Variable selling cost per unit) | $ 48,000 |

| H | Fixed Selling Overhead | $ 130,000 |

| I | Net Operating Income (F - G - H) | $ (34,000) |

| Working Notes:

| ||

| May | Remarks | |

| Sales Volume | 8,000 | (as given in question) |

| Production Volume | 10,000 | (as given in question) |

| Opening Stock | - | (Closing Stock of previous period) |

| Closing Stock | 2,000 | (Opening Stock + Production - Sales) |

| Selling Price per unit | $ 75 | (as given in question) |

| Fixed Manufacturing Cost | $ 270,000 | |

| Fixed Manufacturing Cost per unit | $ 27 | (Fixed manufacturing cost / Production Qty) |

| Variable Selling Cost | $ 6 |

Explanation of Solution

- In absorption costing, direct material, direct labour, variable manufacturing expenses and fixed manufacturing cost per unit are considered for unit product cost;

- The income statement under this method requires following computations:

Cost of Goods Sold comprises of variable as well as fixed manufacturing cost

Total selling expenses comprise of variable as well as fixed selling cost

Given:

Sales volume, production volume and selling price per unit are given in the question.

Formulas:

Cost of Goods Sold:

Note: Unit product cost here is unit cost computed as per absorption costing.

Answer 2:

Variable Costing: is also known as Direct costing method. In this method, those costs which vary directly with production are considered in product cost. Fixed Manufacturing Expenses are treated as period cost and not product cost. Selling Expenses (since they do not vary with production), both variable and fixed, are charged off completely in the period in which the expenses get incurred.

Unit product Cost and Income statement May

Answer to Problem 20P

Solution:

| Computation of Unit Product Cost under Variable Costing | |

| Direct Material | $ 20 |

| Direct Labour | $ 8 |

| Variable Manufacturing Overhead | $ 2 |

| Total Product Cost | $ 30 |

| Income Statement under Variable Costing | ||

| May | ||

| A | Sales(Sales Volume X Sales Price) | 600,000 |

| B | Less: Cost of Goods Sold | |

| C | Beginning Inventory

Opening Inventory Quantity X Unit Product Cost of previous year | $ - |

| D | Add: Variable Manufacturing Cost

Production Quantity X Unit Product Cost | 300,000 |

| E | Less: Closing Inventory

Closing Inventory Quantity X Unit Product Cost of current year | $ 60,000 |

| B | Cost of Goods Sold (C+D-E) | $ 240,000 |

| F | Variable Selling & Admin Expenses(Sales quantity X Variable selling cost per unit) | $ 48,000 |

| G | Contribution Margin (A-B-F) | $ 312,000 |

| Sales Value - (Cost of Goods Sold + Variable selling expenses) | ||

| H | Fixed Manufacturing Overhead | $ 270,000 |

| I | Fixed Selling Overhead | $ 130,000 |

| J | Net Operating Income | $ (88,000) |

| Working Notes:

| ||

| May | Remarks | |

| Sales Volume | 8,000 | (as given in question) |

| Production Volume | 10,000 | (as given in question) |

| Opening Stock | - | (as given in question) |

| Closing Stock | 2,000 | (Opening Stock + Production - Sales) |

| Selling Price per unit | $75 | (as given in question) |

| Variable Selling Cost per unit | $6 |

Explanation of Solution

- In variable costing, direct material, direct labour and variable manufacturing expenses are considered for unit product cost;

- The income statement under this method requires following computations:

Variable cost comprises of variable cost of goods sold and variable selling expenses

Fixed cost comprises of fixed manufacturing cost and fixed selling cost

Given:

Sales volume, production volume, opening stock and selling price per unit are given in the question.

Formulas:

Variable Cost of Goods Sold:

Note: Unit product cost here is unit cost computed as per variable costing.

Answer 3

The difference between the ending inventory values under two costing methods would be on account of fixed cost element on inventory.

Under Variable costing, the inventory is valued at Unit product cost as per variable costing method which is direct material plus direct labour plus variable manufacturing expenses.

Whereas

Under Absorption costing, the inventory is valued at Unit product cost as per absorption costing method which is direct material plus direct labour plus variable manufacturing expenses plus fixed cost per unit.

Due to the inclusion of fixed cost in inventory in absorption costing, following is the impact:

- Opening inventory is higher resulting in decrease in profit

- Closing inventory is higher resulting in increase in profit

Reasons for differences in ending inventory

Explanation of Solution

| Ending inventory value under absorption costing | $ 114,000 |

| Ending inventory value under variable costing | $ 60,000 |

| Difference in inventory values | $ 54,000 |

| Closing Stock Quantity | 2,000 units |

| Fixed manufacturing cost per unit

(considered in unit product cost in absorption costing method) | $ 27 |

| Fixed manufacturing cost absorbed on closing stock

(2,000 units X $ 27 per unit) | 54,000 |

| Profit under absorption costing | $ (34,000) |

| Profit under variable costing | $ (88,000) |

| Difference | $ 54,000 |

As clear from above, the amount of Fixed manufacturing cost absorbed on closing stock is equal to the difference between inventory values under two costing methods.

Also, since closing stock is higher under absorption costing, as a result, loss is also less by

$ 54,000 as compared to variable costing.

Want to see more full solutions like this?

Chapter 7 Solutions

Introduction To Managerial Accounting

- Segment variable costing income statement and effect on operating income of change in operations Valdespin Company manufactures three sizes of camping tentssmall (S), medium (M), and large (L). The income statement has consistently indicated a net loss for the M size, and management is considering three proposals: (1) continue Size M, (2) discontinue Size M and reduce total output accordingly, or (3) discontinue Size M and conduct an advertising campaign to expand the sales of Size S so that the entire plant capacity can continue to be used. If Proposal 2 is selected and Size M is discontinued and production curtailed, the annual fixed production costs and fixed operating expenses could be reduced by 46,080 and 32,240, respectively. If Proposal 3 is selected, it is anticipated that an additional annual expenditure of 34,560 for the rental of additional warehouse space would yield an additional 130% in Size S sales volume. It is also assumed that the increased production of Size S would utilize the plant facilities released by the discontinuance of Size M. The sales and costs have been relatively stable over the past few years, and they are expected to remain so for the foreseeable future. The income statement for the past year ended June 30, 20Y9, is as follows: Instructions 1. Prepare an income statement for the past year in the variable costing format. Use the following headings: Data for each size should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin, as reported in the Total column, to determine operating income. 2. Based on the income statement prepared in (1) and the other data presented, determine the amount by which total annual operating income would be reduced below its present level if Proposal 2 is accepted. 3. Prepare an income statement in the variable costing format, indicating the projected annual operating income if Proposal 3 is accepted. Use the following headings: Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin as reported in the Total column. For purposes of this problem, the expenditure of 34,560 for the rental of additional warehouse space can be added to the fixed operating expenses. 4. By how much would total annual operating income increase above its present level if Proposal 3 is accepted? Explain.arrow_forwardStep Costs, Relevant Range Bellati Inc. produces large industrial machinery. Bellati has a machining department and a group of direct laborers called machinists. Each machinist can machine up to 500 units per year. Bellati also hires supervisors to develop machine specification plans and oversee production within the machining department. Given the planning and supervisory work, a supervisor can oversee, at most, three machinists. Bellatis accounting and production history shows the following relationships between number of units produced and the annual costs of supervision and materials handling (by machinists): Required: 1. Prepare a graph that illustrates the relationship between direct labor cost and number of units produced in the machining department. (Let cost of direct labor be the vertical axis and number of units be the horizontal axis.) Would you classify this cost as a strictly variable cost, a fixed cost, or a step cost? 2. Prepare a graph that illustrates the relationship between the cost of supervision and the number of units produced. (Let cost of supervision be the vertical axis and number of units be the horizontal axis.) Would you classify this cost as a strictly variable cost, a fixed cost, or a step cost? 3. Suppose that the normal range of production is between 1,400 and 1,500 units and that the exact number of machinists is currently hired to support this level of activity. Further suppose that production for the next year is expected to increase by an additional 500 units. What is the increase in the cost of direct labor? Cost of supervision?arrow_forwardProduct Mix Decision, Single Constraint Norton Company produces two products (Juno and Hera) that use the same material input. Juno uses two pounds of the material for every unit produced, and Hera uses five pounds. Currently, Norton has 16,000 pounds of the material in inventory. All of the material is imported. For the coming year, Norton plans to import an additional 8,000 pounds to produce 2,000 units of Juno and 4,000 units of Hera. The unit contribution margin is 30 for Juno and 60 for Hera. Also, assume that Nortons marketing department estimates that the company can sell a maximum of 2,000 units of Juno and 4,000 units of Hera. Norton has received word that the source of the material has been shut down by embargo. Consequently, the company will not be able to import the 8,000 pounds it planned to use in the coming years production. There is no other source of the material. Required: 1. Compute the total contribution margin that the company would earn if it could manufacture 2,000 units of Juno and 4,000 units of Hera. 2. Determine the optimal usage of the companys inventory of 16,000 pounds of the material. Compute the total contribution margin for the product mix that you recommend.arrow_forward

- Functional-Based versus Activity-Based Costing For years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindo added a line of duffel bags. With this addition, the company began assigning overhead costs by using departmental rates. (Prior to this, the company used a predetermined plantwide rate based on units produced.) Surprisingly, after the addition of the duffel-bag line and the switch to departmental rates, the costs to produce the backpacks increased, and their profitability dropped. Josie, the marketing manager, and Steve, the production manager, both complained about the increase in the production cost of backpacks. Josie was concerned because the increase in unit costs led to pressure to increase the unit price of backpacks. She was resisting this pressure because she was certain that the increase would harm the companys market share. Steve was receiving pressure to cut costs also, yet he was convinced that nothing different was being done in the way the backpacks were produced. After some discussion, the two managers decided that the problem had to be connected to the addition of the duffel-bag line. Upon investigation, they were informed that the only real change in product-costing procedures was in the way overhead costs are assigned. A two-stage procedure was now in use. First, overhead costs are assigned to the two producing departments, Patterns and Finishing. Second, the costs accumulated in the producing departments are assigned to the two products by using direct labor hours as a driver (the rate in each department is based on direct labor hours). The managers were assured that great care was taken to associate overhead costs with individual products. So that they could construct their own example of overhead cost assignment, the controller provided them with the information necessary to show how accounting costs are assigned to products: The controller remarked that the cost of operating the accounting department had doubled with the addition of the new product line. The increase came because of the need to process additional transactions, which had also doubled in number. During the first year of producing duffel bags, the company produced and sold 100,000 backpacks and 25,000 duffel bags. The 100,000 backpacks matched the prior years output for that product. Required: (Note: Round rates and unit cost to the nearest cent.) 1. CONCEPTUAL CONNECTION Compute the amount of accounting cost assigned to a backpack before the duffel-bag line was added by using a plantwide rate approach based on units produced. Is this assignment accurate? Explain. 2. Suppose that the company decided to assign the accounting costs directly to the product lines by using the number of transactions as the activity driver. What is the accounting cost per unit of backpacks? Per unit of duffel bags? 3. Compute the amount of accounting cost assigned to each backpack and duffel bag by using departmental rates based on direct labor hours. 4. CONCEPTUAL CONNECTION Which way of assigning overhead does the best jobthe functional-based approach by using departmental rates or the activity-based approach by using transactions processed for each product? Explain. Discuss the value of ABC before the duffel-bag line was added.arrow_forwardVariable costing income statement for a service company East Coast Railroad Company transports commodities among three routes (city-pairs): Atlanta/Baltimore, Baltimore/Pittsburgh, and Pittsburgh/Atlanta. Significant costs, their cost behavior, and activity rates for April are as follows: Operating statistics from the management information system reveal the following for April: A. Prepare a contribution margin by route report for East Coast Railroad Company for the month of April. Compute the contribution margin ratio in whole percents, rounded to one decimal place. B. Evaluate the route performance of the railroad using the report in (A).arrow_forwardIncome Statements under Absorption and Variable Costing In the coming year, Kalling Company expects to sell 28,700 units at 32 each. Kallings controller provided the following information for the coming year: Required: 1. Calculate the cost of one unit of product under absorption costing. 2. Calculate the cost of one unit of product under variable costing. 3. Calculate operating income under absorption costing for next year. 4. Calculate operating income under variable costing for next year.arrow_forward

- Assume a company has two divisions, Division B and Division C. Division B has provided the following information regarding the one product that it manufactures and sells on the outside market: Selling price per unit (on the outside market) $ 60 Variable cost per unit $ 44 Fixed costs per unit (based on capacity) $ 8 Capacity in units 20,000 Division C could use Division B’s product as a component part in the manufacture of 4,000 units of its own newly-designed product. Division C has received a quote of $58 from an outside supplier for a component part that is comparable to the one that Division B makes. If the company’s divisional managers are evaluated based on their division’s profits and Division B is currently selling 15,000 units on the outside market, what is Division C’s highest acceptable transfer price if it were to buy 4,000 units from Division B? Multiple Choice $48 $52 $44 $58arrow_forwardVariable and Absorption Costing Unit Product Costs and Income Statements Walsh Company manufactures and sells one product. The following information pertains to each of the company’s first two years of operations: During its first year of operations. Walsh produced 50,000 units and sold 40,000 units. During its second year of operations, it produced 40,000 units and sold 50,000 units. The selling price of the company’s product is $60 per unit. Required: 1. Assume the company uses variable costing: a. Compute the unit product cost for Year 1 and Year 2. b. Prepare an income statement for Year I and Year 2. 2. Assume the company uses absorption costing: a. Compute the unit product cost for Year I and Year 2. b. Prepare an income statement tor Year 1 and Year 2. 3. Explain the difference between variable costing and absorption costing net operating income in Year 1. Also, explain why the two net operating incomes differ in Year 2.arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,