Concept explainers

Videos

Gigabyte, Inc. manufactures three products for the computer industry:

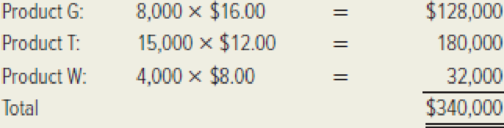

Gismos (product G): annual sales, 8,000 units

Thingamajigs (product T): annual sales, 15,000 units

Whatchamacallits (product W): annual sales, 4,000 units

The company uses a traditional, volume-based product-costing system with manufacturing overhead applied on the basis of direct-labor dollars. The product costs have been computed as follows:

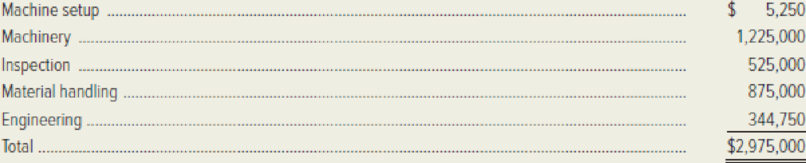

*Calculation of predetermined overhead rate:

Manufacturing overhead budget:

Direct-labor budget (based on budgeted annual sales):

Gigabyte’s pricing method has been to set a target price equal to 150 percent of full product cost. However, only the thingamajigs have been selling at their target price. The target and actual current prices for all three products are the following:

Gigabyte has been forced to lower the price of gismos in order to get orders. In contrast, Gigabyte has raised the price of whatchamacallits several times, but there has been no apparent loss of sales. Gigabyte, Inc. has been under increasing pressure to reduce the price even further on gismos. In contrast, Gigabyte’s competitors do not seem to be interested in the market for whatchamacallits. Gigabyte apparently has this market to itself.

Required:

- 1. Is product G the company’s least profitable product?

- 2. Is product W a profitable product for Gigabyte, Inc.?

- 3. Comment on the reactions of Gigabyte’s competitors to the firm’s pricing strategy. What dangers does Gigabyte, Inc. face?

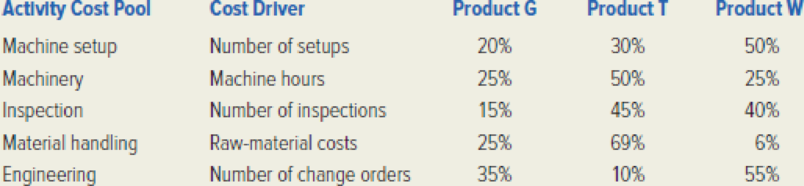

- 4. Gigabyte’s controller, Nan O’Second, recently attended a conference at which activity-based costing systems were discussed. She became convinced that such a system would help Gigabyte’s management to understand its product costs better. She got top management’s approval to design an activity-based costing system, and an ABC project team was formed. In stage one of the ABC project, each of the overhead items listed in the overhead budget was placed into its own activity cost pool. Then a cost driver was identified for each activity cost pool. Finally, the ABC project team compiled data showing the percentage of each cost driver that was consumed by each of Gigabyte’s product lines. These data are summarized as follows:

Show how the controller determined the percentages given above for raw-material costs. (Round to the nearest whole percent.)

- 5. Develop product costs for the three products on the basis of an activity-based costing system. (Round to the nearest cent.)

- 6. Calculate a target price for each product, using Gigabyte’s pricing formula. Compare the new target prices with the current actual selling prices and previously reported product costs.

- 7. Build a spreadsheet: Construct an Excel spreadsheet to solve requirements (5) and (6) above. Show how the solution will change if the inspection activity was divided among the three products in the following manner: product G, 20%; product T, 40%, and product W, 40%.

Want to see the full answer?

Check out a sample textbook solution

Chapter 5 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

- The following product costs are available for Stellis Company on the production of erasers: direct materials, $22,000; direct labor, $35,000; manufacturing overhead, $17,500; selling expenses, $17,600; and administrative expenses; $13,400. What are the prime costs? What are the conversion costs? What is the total product cost? What is the total period cost? If 13,750 equivalent units are produced, what is the equivalent material cost per unit? If 17,500 equivalent units are produced, what is the equivalent conversion cost per unit?arrow_forwardMedical Tape makes two products: Generic and Label. It estimates it will produce 423,694 units of Generic and 652,200 of Label, and the overhead for each of its cost pools is as follows: It has also estimated the activities for each cost driver as follows: How much is the overhead allocated to each unit of Generic and Label?arrow_forwardLarsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forward

- The following product Costs are available for Haworth Company on the production of chairs: direct materials, $15,500; direct labor, $22.000; manufacturing overhead, $16.500; selling expenses, $6,900; and administrative expenses, $15,200. What are the prime costs? What are the conversion costs? What is the total product cost? What is the total period cost? If 7,750 equivalent units are produced, what is the equivalent material cost per unit? If 22,000 equivalent units are produced, what is the equivalent conversion cost per unit?arrow_forwardBrees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for 66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows: Prior to making a decision, the companys CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following: 3 setups1,160 each (The setups would be avoided, and total spending could be reduced by 1,160 per setup.) One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is 12,300 and could be totally avoided if the part were purchased. Engineering work: 470 hours, 45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.) 75 fewer material moves at 30 per move. Required: 1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier. 2. Now, using the special study data, repeat the analysis. 3. Discuss the qualitative factors that would affect the decision, including strategic implications. 4. After reviewing the special study, the controller made the following remark: This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs? Is the controller right?arrow_forwardWrappers Tape makes two products: Simple and Removable. It estimates it will produce 369,991 units of Simple and 146,100 of Removable, and the overhead for each of its cost pools is as follows: It has also estimated the activities for each cost driver as follows: Â How much is the overhead allocated to each unit of Simple and Removable?arrow_forward

- A manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardCool Pool has these costs associated with production of 20,000 units of accessory products: direct materials, $70; direct labor, $110; variable manufacturing overhead, $45; total fixed manufacturing overhead, $800,000. What is the cost per unit under both the variable and absorption methods?arrow_forwardGeneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forward

- The following product costs are available for Kellee Company on the production of eyeglass frames: direct materials, $32,125; direct labor, $23.50; manufacturing overhead, applied at 225% of direct labor cost; selling expenses, $22,225; and administrative expenses, $31,125. The direct labor hours worked for the month are 3,200 hours. A. What are the prime costs? B. What are the conversion costs? C. What is the total product cost? D. What is the total period cost? E. If 6.425 equivalent units are produced, what is the equivalent material cost per unit? F. What is the equivalent conversion cost per unit?arrow_forwardCarla Vista Manufacturing manufactures a single product. Annual production costs incurred in the manufacturing process are shown below for the production of 2,900 units. The company's Utilities and Maintenance costs are mixed costs. The fixed portions of these costs are $390 and $290, respectively. Calculate the expected costs to be incurred when production is 4,900 units. Use your knowledge of cost behavior to determine which of the other costs are foxed or variable. Production in Units Production Costs a. Direct Materials b. Direct Labor c. Utilities d. Rent e. Indirect Labor f. Supervisory Salaries & Maintenance 2,900 $ 8,961 23,461 1,666 3,900 6,351 2,400 1,711 Costs Incurred $ 4,900 Type of cost 10 0000 Farrow_forwardBarkes, Incorporated, manufactures and sells two products: Product BO and Product B5. Data concerning the expected production of each product and the expected total direct labor-hours (DLHs) required to produce that output appear below: Product B0 Product B5 Total direct labor-hours Total Direct Expected Hours Per Labor- Production Unit Hours 400 7.0 500 4.0 Activity Cost Pools Labor-related Production orders Order size Direct Labor- The direct labor rate is $22.10 per DLH. The direct materials cost per unit is $288.10 for Product BO and $118.90 for Product B5. The company has an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Expected Activity Estimated Overhead Cost Activity Measures DLHs orders MHS 2,800 2,000 4,800 $ 136,944 64,629 588,294 $ 789,867 Product B0 Product B5 2,800 2,000 500 400 3,300 3,000 Total 4,800 900 6,300 The total overhead applied to Product BO under activity-based costing is closest to: (Round your…arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning