Concept explainers

Videos

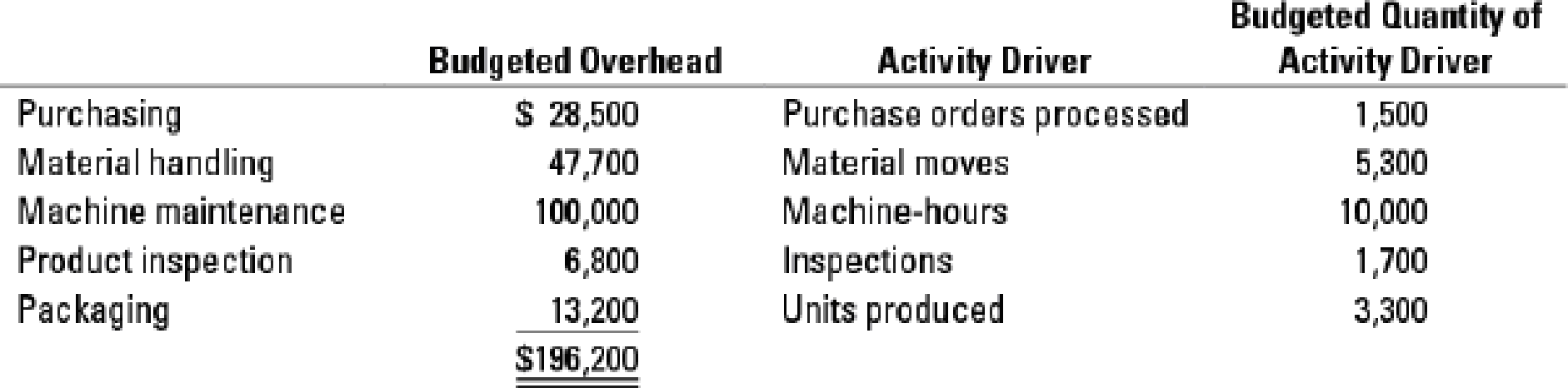

Activity-based costing. The

Information related to Job 220 and Job 330 follows. Job 220 incurs more batch-level costs because it uses more types of materials that need to be purchased, moved, and inspected relative to Job 330.

| Job 220 | Job 330 | |

| Number of purchase orders | 21 | 9 |

| Number of material moves | 18 | 6 |

| Machine-hours | 30 | 70 |

| Number of inspections | 10 | 2 |

| Units produced | 17 | 5 |

- 1. Compute the total overhead allocated to each job under a simple costing system, where overhead is allocated based on machine-hours.

Required

- 2. Compute the total overhead allocated to each job under an activity-based costing system using the appropriate activity drivers.

- 3. Explain why Melody’s Custom Framing might favor the ABC job-costing system over the simple job-costing system, especially in its bidding process.

Learn your wayIncludes step-by-step video

Chapter 5 Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Additional Business Textbook Solutions

Horngren's Accounting (12th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Intermediate Accounting

Financial Accounting

Managerial Accounting (4th Edition)

- For each of the following activities, select the most appropriate cost driver. Each cost driver may be used only once. Activity Cost Driver 1. Pay vendors Answer 2. Evaluate vendors Answer 3. Inspect raw materials Answer 4. Plan for purchases of raw materials Answer 5. Packaging Answer 6. Supervision Answer 7. Employee training Answer 8. Clean tables Answer 9. Machine maintenance Answer 10. Move in-process product from one work station to the next Answerarrow_forwardxterior door? job-costing system. Total budgeted costs in each indirect-cost pool and the budgeted quantity of activity The company is in the process of bidding on two jobs: Job 220, an order of 17 intricate personalized overhead allocated under the current simple job-costing system and a newly designed activity-based frames, and Job 330, an order of 5 standard personalized frames. The controller wants you to compare 5-29 Activity-based costing. The job-costing system at Melody's Custom Framing has five indirect cost pools (purchasing, material handling, machine maintenance, product inspection, and packaging). goods, milk and fruit juice, and frozen foods. It upermarkets (FS) operates at capacity and de- nformation from its activity-based costing system Fes that account for the store support costs, rs? vs: driver are as follows. $95 per purchase order $76 per delivery $19 per hour S 0.15 per item sold Budgeted Quantity of Activity Driver TET Budgeted Overhead Activity Driver Purchase…arrow_forwardUsing job order costing in a service company Bluebird Design, Inc. is a Web site design and consulting firm. The firm uses a job order costing system in which each client is a different job. Bluebird Design assigns direct labor, licensing costs, and travel costs directly to each job. It allocates indirect costs to jobs based on a predetermined overhead allocation rate, computed as a percentage of direct labor costs. At the beginning of 2018, managing partner Sally Simone prepared the following budget estimates: In November 2018, Bluebird Design served several clients. Records for two clients appear here: Requirements Compute Bluebird Designs direct labor rate and its predetermined overhead allocation rate for 2018. Compute the total cost of each job. If Simone wants to earn profits equal to 50% of service revenue, what fee should she charge each of these two clients? Why does Bluebird Design assign costs to jobs?arrow_forward

- Time-Driven Activity-Based Costing Saratoga Company manufactures jobs to customer specifications. The company is conducting a time-driven activity-based costing study in its Purchasing Department to better understand how Purchasing Department labor costs are consumed by individual jobs. To aid the study, the company provided the following data regarding its Purchasing Department and three of its many jobs: Required: 1. Calculate the cost per minute of the resource supplied in the Purchasing Department. 2. Calculate the time-driven activity rate for each of Saratoga’s three activities. 3. Calculate the total purchasing labor costs assigned to Job X, Job Y, and Job Z.arrow_forwardsolve questions d,e,f from the question given in the image. Bella Incorporated uses a job-order costing system and a predetermined overhead rate based on machine hours. Remaining question is in the images provided.arrow_forwardTwo years ago, company scientists developed an alloy with all of the properties of the raw materials used in XL-D that generates no wastewater. Some prototype components using the new material were produced and tested and found to be indistinguishable from the old components in every way relating to their fitness for use. The only difference is that the new alloy is more expensive than the old raw material. The company has been test-marketing the newer version of the component, referred to as XL-C, and is currently trying to decide its fate. Manufacturing of both components begins in the Production Department and is completed in the Assembly Department. No other products are produced in the plant. The following information relates to the two components: Units produced Raw material costs per unit Direct labor-hours per unit-Production Direct labor-hours per unit-Assembly Direct labor rate per hour-all labor Machine-hours per unit-Production Machine-hours per unit-Assembly Testing hours…arrow_forward

- Central Perk, LLC, a manufacturer of coffee beans, is considering switching its operations to an Activity Based Costing system. The following manufacturing overhead activities and cost drivers have been identified: Activity. Machine setup Machine assembly Product inspection Product movement General factory Cost Driver Number of machine setups Machine hours logged Inspection hours logged Number of moves Machine hours logged Based on the above descriptions, which of the following correctly pairs the activity with its appropriate cost level? O A. Product Inspection... batch level cost OB. Product Movement... facility level cost O C. Machine Assembly... unit level cost O D. General Factory... batch level cost O E. Machine Setup... unit level costarrow_forwardShalom Company uses traditional costing method in allocating overhead. When you presented the idea of activity-based costing, the manager became interested and showed you details of its current costing method: Overhead using Products Traditional Allocation Peace Piss Piece 460,000 540,000 920,000 Cost drivers 40,000 30,000 90,000 1,920,000 The manager wants a report that shows comparison of the two costing methods. You began your analysis and applied activity-based costing. What product line/s had an overstated overhead cost?arrow_forwardJob costing; variation on actual, normal, and variation from normal costing. Creative Solutions designs Web pages for clients in the education sector. The company’s job-costing system has a single direct cost category (Web-designing labor) and a single indirect cost pool composed of all overhead costs. Overhead costs are allocated to individual jobs based on direct labor-hours. The company employs six Web designers. Budgeted and actual information regarding Creative Solutions follows:arrow_forward

- Aresco Corporation manufactures two products: Product G51B and Product E48X. The company uses a plantwide overhead rate based on direct labor-hours. It is considering implementing an activity-based costing (ABC) system that allocates all of its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products G51B and E48X. Activity Cost Pool Machining Machine setups Product design Order size Activity Measure Machine-hours Number of setups Number of products Direct labor-hours Activity Measure Machine-hours Number of setups Number of products Direct labor-hours Product G51B 2,180 252 1 3,180 Total Cost $ 104,500 $ 304,500 $ 84,500 $ 381,500 Product E48X 2,820 248 1 6,820 Total Activity 5,000 MHS 500 setups 2 products 10,000 DLHS Required: a. Using the plantwide overhead rate, what percentage of the total overhead cost is allocated to Product G51B? b. Using the plantwide overhead rate, what percentage of the total…arrow_forwardHails Corporation manufactures two products: Product Q21F and Product H44W. The company uses a plantwide overhead rate based on direct labor- hours. It is considering implementing an activity-based costing (ABC) system that allocates its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products Q21F and H44W. Activity Cost Pool Machining Machine setups Product design Order size Machine-hours Number of setups Number of products Direct labor-hours 26.71% 50.00% 34.18% Activity Measure O 60.89% Machine-hours Number of setups Number of products Direct labor-hours Activity Measure Total Cost Total Activity $ 195,000 13,000 MHs 90,000 150 setups $ $ 64,000 $ 280,000 Product Q21F 9,000 80 1 6,000 Using the ABC system, the percentage of the total overhead cost that is assigned to Product Q21F is closest to: 2 products 10,000 DLHs Product H44W 4,000 70 1 4,000arrow_forwardJob-order costing is used to calculate the cost of producing a unique or custom-made product, whereas process costing is used for the production of standardized products. Job-order costing assigns costs to each job, while process costing assigns costs to each process or department. Job-order costing uses job cost sheets to accumulate costs for each job, while process costing uses departmental production reports to accumulate costs for each process. Job-order costing can have high variation in production costs per unit, while process costing typically results in more stable production costs per unit. Job-order costing is more suitable for small production runs, while process costing is more suitable for large-scale production. Job-order costing requires a higher level of record-keeping and tracking of costs for each job, while process costing requires tracking of costs for each department or process.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub