Concept explainers

Videos

(Appendix 4B) Support Department Cost Allocation

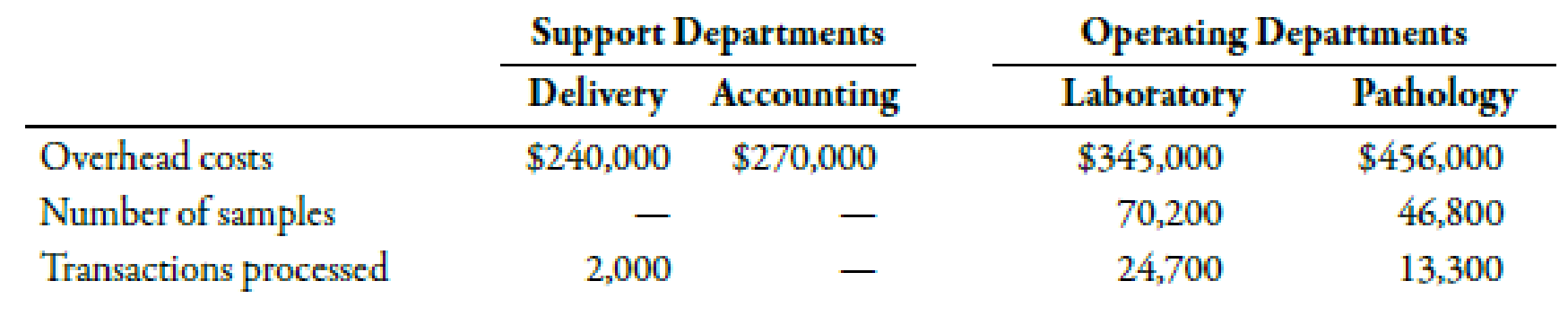

MedServices Inc. is divided into two operating departments: Laboratory and Tissue Pathology. The company allocates delivery and accounting costs to each operating department. Delivery costs include the costs of a fleet of vans and drivers that drive throughout the state each day to clinics and doctors’ offices to pick up samples and deliver them to the centrally located laboratory and tissue pathology offices. Delivery costs are allocated on the basis of number of samples. Accounting costs are allocated on the basis of the number of transactions processed. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data:

Required:

- 1. Assign the support department costs by using the direct method. (Note: Round allocation ratios to four decimal places.)

- 2. Assign the support department costs by using the sequential method, allocating accounting costs first. (Note: Round allocation ratios to four decimal places.)

1.

Calculate the assigned cost of support departments by using direct method.

Explanation of Solution

Direct Method:

Direct method implies that the unit cost must include all the factory costs. It states that the cost of support departments should not be added in the unit cost if it is not included in operating departments’ cost because they do not play any role in selling the unit or product.

Use the following formula to calculate assignment ratios on the basis of number of samples:

Laboratory department:

Substitute 70,200 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for laboratory department is 0.60.

Pathology department:

Substitute 46,800 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for pathology department is 0.40.

Use the following formula to calculate assignment ratios on the basis of transactions processed:

Laboratory department:

Substitute 24,700 for transactions processed in laboratory and 38,000 for total transactions processed in operating department in the above formula.

Therefore, the assignment ratio for laboratory department is 0.65.

Pathology department:

Substitute 13,300 for transactions processed in laboratory and 38,000 for total transactions processed in operating department in the above formula.

Therefore, the assignment ratio for pathology department is 0.35.

Assign cost of support departments to the operating departments:

| Support departments | Operating departments | |||

| Delivery($) | Accounting($) | Laboratory($) | Pathology($) | |

| Direct costs | 240,000 | 270,000 | 345,000 | 456,000 |

| Delivery1 | -240,000 | 144,000 | 96,000 | |

| Accounting1 | -270,000 | 175,500 | 94,500 | |

| Total | 0 | 0 | 664,500 | 646,500 |

Table (1)

Working Note:

1. Calculation of assigned cost of support department to operating department:

| Account Title |

Assignment ratio A |

Support department cost($) B |

Assigned cost($) |

| Delivery cost: | |||

| Laboratory | 0.6000 | 240,000 | 144,000 |

| Pathology | 0.4000 | 240,000 | 96,000 |

| Accounting: | |||

| Laboratory | 0.65 | 270,000 | 175,500 |

| Pathology | 0.35 | 270,000 | 94,500 |

Table (2)

2.

Calculate the assigned cost of support departments by using sequential method and allocate accounting costs first.

Explanation of Solution

Sequential Method:

Sequential method recognizes that there is possible interaction between the support departments. However, it does not account for such interaction in full which makes it more accurate as compared to the direct method.

Use the following formula to calculate cost assignment ratios on the basis of number of transactions processed:

Delivery:

Substitute 2,000 for transactions processed in delivery and 40,000 for total transactions processed in the above formula.

Therefore, the cost assignment ratio for delivery is 0.0500.

Laboratory department:

Substitute 24,700 for transactions processed in laboratory and 40,000 for total transactions processed in the above formula.

Therefore, the cost assignment ratio for laboratory department is 0. 6175.

Pathology department:

Substitute 13,300 for transactions processed in pathology and 40,000 for total transactions processed in the above formula.

Therefore, the cost assignment ratio for pathology department is 0.3325.

Use the following formula to calculate assignment ratios on the basis of number of samples:

Laboratory department:

Substitute 70,200 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for laboratory department is 0.60.

Pathology department:

Substitute 46,800 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for pathology department is 0.40.

Assign cost of support departments to the operating departments:

| Support departments | Operating departments | |||

| Delivery($) | Accounting($) | Laboratory($) | Pathology($) | |

| Direct costs | 240,000 | 270,000 | 345,000 | 456,000 |

| Accounting2 | 13,500 | 166,725 | 89,775 | |

| Delivery2 | -253,500 | -270,000 | 152,100 | 101,400 |

| Total | 0 | 0 | 663,825 | 647,175 |

Table (3)

Working Note:

2. Calculation of assigned cost of support department:

| Account Title |

Assignment ratio A |

Support department cost($) B |

Assigned cost($) |

| Accounting: | |||

| Delivery | 0.0500 | 270,000 | 13,500 |

| Laboratory | 0.6175 | 270,000 | 166,725 |

| Pathology | 0.3325 | 270,000 | 89,775 |

| Delivery cost: | |||

| Laboratory | 0.60 | 253,500 | 152,100 |

| Pathology | 0.40 | 253,500 | 101,400 |

Table (4)

Want to see more full solutions like this?

Chapter 4 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- Varney Corporation, a manufacturer of electronics and communications systems, allocates Computing and Communications Services Department (CCS) costs to profit centers. The following table lists the types of services and cost drivers for each service. The table also includes the budgeted cost and quantity for each service for August. CCS ServiceCategory Cost Drivers Budgeted Cost Budgeted Quantityof Services Help desk Number of calls $50,400 2,800 Network center Number of devices monitored 170,100 2,100 Electronic mail Number of user accounts 151,700 4,100 Smartphone support Number of smartphones issued 115,600 3,400 One of the profit centers for Varney Corporation is the Communication Systems (COMM) sector. Assume the following information for COMM: • COMM has 2,400 employees, of whom 40% are office employees. • All the office employees have been issued a smartphone, and 92% of them have a computer on the network. • Ninety percent of the employees with a…arrow_forwardVarney Corporation, a manufacturer of electronics and communications systems, allocates Computing and Communications Services Department (CCS) costs to profit centers. The following table lists the types of services and cost drivers for each service. The table also includes the budgeted cost and quantity for each service for August. CCS Services Cost Drivers Budgeted Cost Budgeted Quantityof Services Help desk Number of calls $90,000 3,600 Network center Number of devices 120,000 1,500 Electronic mail Number of user accounts 160,000 5,000 Smartphone support Number of smartphones issued 72,000 4,000 One of the profit centers for Varney Corporation is the Communication Systems (COMM) division. Assume the following information for COMM: COMM has 2,500 employees, of whom 20% are office employees. All of the office employees have been issued a smartphone, and 95% of them have a computer on the network. One hundred percent of the employees with a computer also…arrow_forwardMiddler Corporation, a manufacturer of electronics and communications systems, uses a service department charge system to charge profit centers with Computing and Communications Services (CCS) service department costs. The following table identifies an abbreviated list of service categories and activity bases used by the CCS department. The table also includes some assumed cost and activity base quantity information for each service for October. CCS ServiceCategory Activity Base Budgeted Cost Budgeted ActivityBase Quantity Help desk Number of calls $55,660 2,200 Network center Number of devices monitored 668,100 10,200 Electronic mail Number of user accounts 57,500 5,750 Handheld technology support Number of handheld devices issued 153,600 9,600 One of the profit centers for Middler Corporation is the Communication Systems (COMM) sector. Assume the following information for the COMM sector: The sector has 1,000 employees, of whom 50% are office employees.…arrow_forward

- Middler Corporation, a manufacturer of electronics and communications systems, uses a service department charge system to charge profit centers with Computing and Communications Services (CCS) service department costs. The following table identifies an abbreviated list of service categories and activity bases used by the CCS department. The table also includes some assumed cost and activity base quantity information for each service for October. CCS ServiceCategory Activity Base Budgeted Cost Budgeted ActivityBase Quantity Help desk Number of calls $82,350 2,700 Network center Number of devices monitored 631,125 9,350 Electronic mail Number of user accounts 63,500 6,350 Handheld technology support Number of handheld devices issued 140,800 8,800 One of the profit centers for Middler Corporation is the Communication Systems (COMM) sector. Assume the following information for the COMM sector: The sector has 1,000 employees, of whom 30% are office employees.…arrow_forwardMiddler Corporation, a manufacturer of electronics and communications systems, uses a service department charge system to charge profit centers with Computing and Communications Services (CCS) service department costs. The following table identifies an abbreviated list of service categories and activity bases used by the CCS department. The table also includes some assumed cost and activity base quantity information for each service for October. CCS ServiceCategory Activity Base Budgeted Cost Budgeted ActivityBase Quantity Help desk Number of calls $82,350 2,700 Network center Number of devices monitored 631,125 9,350 Electronic mail Number of user accounts 63,500 6,350 Handheld technology support Number of handheld devices issued 140,800 8,800 One of the profit centers for Middler Corporation is the Communication Systems (COMM) sector. Assume the following information for the COMM sector: The sector has 1,000 employees, of whom 30% are office employees.…arrow_forwardMiddler Corporation, a manufacturer of electronics and communications systems, uses a service department charge system to charge profit centers with Computing and Communications Services (CCS) service department costs. The following table identifies an abbreviated list of service categories and activity bases used by the CCS department. The table also includes some assumed cost and activity base quantity information for each service for October. CCS ServiceCategory Activity Base Budgeted Cost Budgeted ActivityBase Quantity Help desk Number of calls $160,000 3,200 Network center Number of devices monitored 735,000 9,800 Electronic mail Number of user accounts 100,000 10,000 Handheld Technology support Number of handheld devices issued 124,600 8,900 One of the profit centers for Middler Corporation is the Communication Systems (COMM) sector. Assume the following information for the COMM sector: The sector has 5,200 employees, of whom 25% are office…arrow_forward

- The Vest School of Vocational Technology has organized the school training programs into three departments. Each department provides training in a different area as follows: nursing assistant, dental hygiene, and office technology. The school's owner, Candice Vest, wants to know how much it cost to operate each of the three departments. To accumulate the total cost for each department, the accountant has identified several indirect costs that must be allocated to each. These costs are $10,080 of telephone expense, $2,016 of supplies expense, $720,000 of office rent, $144,000 of janitorial services, and $150,000 of salary paid to the dean of students. To provide a reasonably accurate allocation of costs, the accountant has identified several possible cost drivers. These drivers and their association with each department follow. Cost Driver Department 1 Department 2 Department 3 Number of telephone 28 16 19 Number of faculty members 20 16 12 Square footage of office space 28,000 16,800…arrow_forwardBrewster Toymakers Inc. produces toys for children. The toys are produced in the Molding andAssembly departments. The Janitorial and Security departments support the production of thetoys. Costs from the Janitorial Department are allocated based on square feet. Costs from theSecurity Department are allocated based on asset value. Relevant department information isprovided in the following table: Using the reciprocal services method of support department cost allocation, determine(a) the percentage of Janitorial costs that should be allocated to the Security Departmentand(b) the percentage of Security costs that should be allocated to the Janitorial Department.arrow_forwardSupport Department Allocations And Cost Drivers Varney Corporation, a manufacturer of electronics and communications systems, allocates Computing and Communications Services Department (CCS) costs to profit centers. The following table lists the types of services and cost drivers for each service. The table also includes the budgeted cost and quantity for each service for August. CCS Services Cost Drivers Budgeted Cost Budgeted Quantityof Services Help desk Number of calls $72,000 3,600 Network center Number of devices 168,000 2,000 Electronic mail Number of user accounts 166,500 4,500 Smartphone support Number of smartphones issued 131,200 4,100 One of the profit centers for Varney Corporation is the Communication Systems (COMM) division. Assume the following information for COMM: COMM has 3,500 employees, of whom 35% are office employees. All of the office employees have been issued a smartphone, and 96% of them have a computer on the network. Of the employees with a…arrow_forward

- "The controller for Tulsa Medical Supply Company has established the following activity cost pools and cost drivers. Activity Cost Pool Budgeted Overhead cost Cost Driver Budgeted Level for cost Driver Pool Rate Machine Setups $250,000 Number of Setups 125 $2,000 per setup Material Handling 75,000 Weight of Raw Material 37,500 Lb. $2 per pound Hazardous Waste Control 25,000 Weight of hazardous Chemical used 5,000 Lb. $5 per pound Quality Control 75,000 Numbers of Inspections 1,000 $75 per inspection Other Overhead cost 200,000 Machine Hours 20,000 $10 per hours Total $625,000 An order for 1,000 boxes of medical-testing agent has the following production requirements Machine setups ...............................................................................................5 setups Raw material .........................................................................................10,000…arrow_forward"The controller for Tulsa Medical Supply Company has established the following activity cost pools and cost drivers. Activity Cost Pool Budgeted Overhead cost Cost Driver Budgeted Level for cost Driver Pool Rate Machine Setups $250,000 Number of Setups 125 $2,000 per setup Material Handling 75,000 Weight of Raw Material 37,500 Lb. $2 per pound Hazardous Waste Control 25,000 Weight of hazardous Chemical used 5,000 Lb. $5 per pound Quality Control 75,000 Numbers of Inspections 1,000 $75 per inspection Other Overhead cost 200,000 Machine Hours 20,000 $10 per hours Total $625,000 An order for 1,000 boxes of medical-testing agent has the following production requirements Machine setups ...............................................................................................5 setups Raw material .........................................................................................10,000…arrow_forward"The controller for Tulsa Medical Supply Company has established the following activity cost pools and cost drivers. Activity Cost Pool Budgeted Overhead cost Cost Driver Budgeted Level for cost Driver Pool Rate Machine Setups $250,000 Number of Setups 125 $2,000 per setup Material Handling 75,000 Weight of Raw Material 37,500 Lb. $2 per pound Hazardous Waste Control 25,000 Weight of hazardous Chemical used 5,000 Lb. $5 per pound Quality Control 75,000 Numbers of Inspections 1,000 $75 per inspection Other Overhead cost 200,000 Machine Hours 20,000 $10 per hours Total $625,000 An order for 1,000 boxes of medical-testing agents has the following production requirements Machine setups ...............................................................................................5 setups Raw material .........................................................................................10,000…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub