Governmental and Nonprofit Accounting (11th Edition)

11th Edition

ISBN: 9780133799569

Author: Robert J. Freeman, Craig D. Shoulders, Dwayne N. McSwain, Robert B. Scott

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 3, Problem 7E

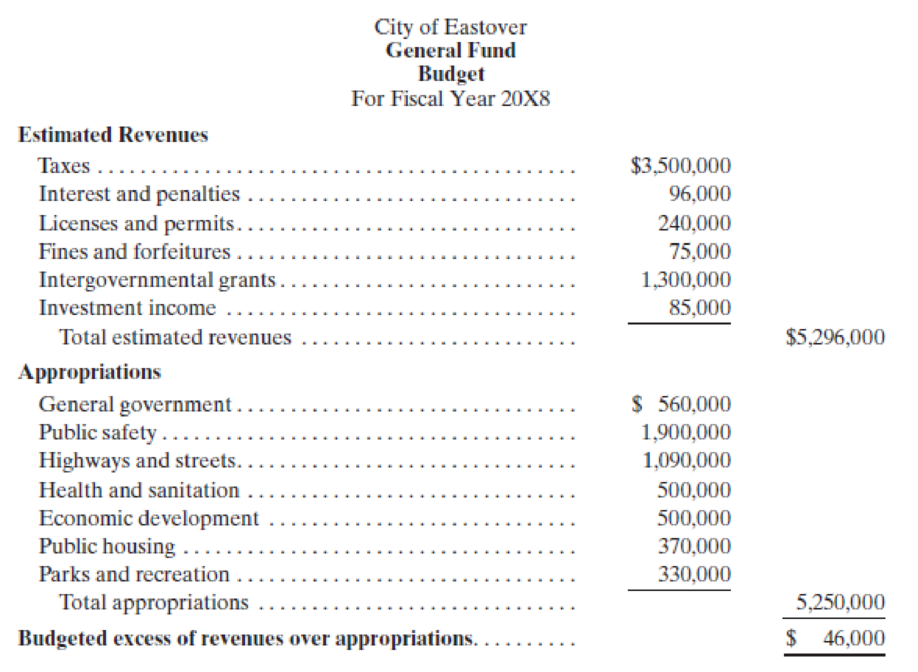

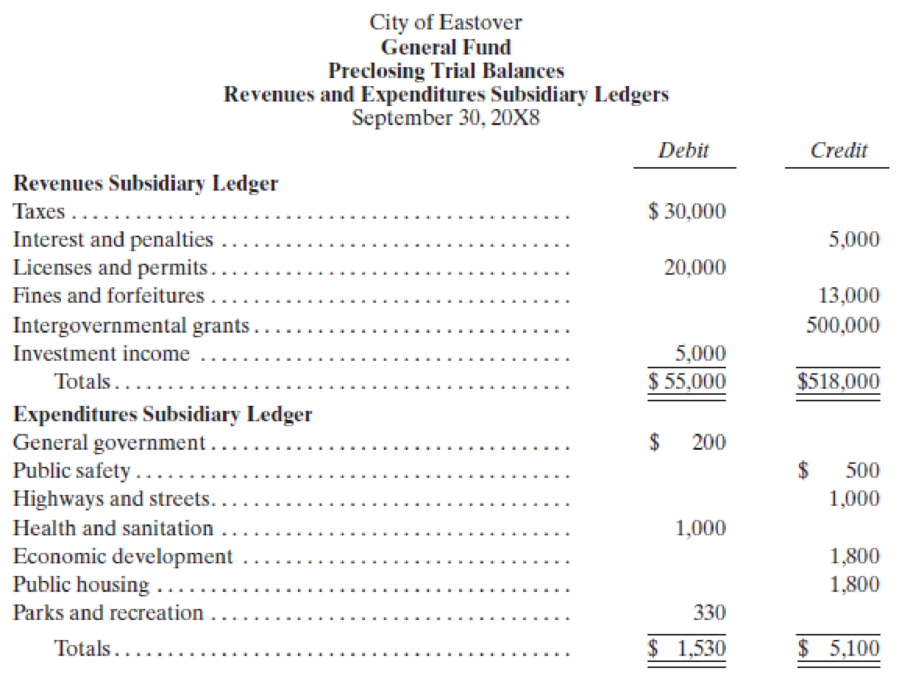

(General Ledger—Subsidiary Ledgers Relationship, Closing Entries, Budgetary Statement) The Eastover City Council adopted the following budget for its General Fund for 20X8. The budget was not revised during the fiscal year. The budgetary basis was modified accrual.

The preclosing

The only encumbrances outstanding at year end were for $75,000 of unperformed contracts for the Health and Sanitation function. The beginning total fund balance was $312,000.

- a. Prepare closing entries for both the General Ledger accounts and the subsidiary ledgers of the City of Eastover General Fund. (Hint: You will have to derive the General Ledger balances of some accounts.)

- b. Prepare the Statement of Revenues, Expenditures, and Changes in Fund Balance—Budget and Actual for the General Fund of the City of Eastover for fiscal year 20X8.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Greenville has provided the following Information from its General Fund Revenues and Appropriations/Expenditure/Encumbrances

subsidiary ledgers for the fiscal year ended. Assume the beginning fund balances are $149 (in thousands) and that the budget was not

amended during the year.

City of Greenville

General Fund

Subsidiary Ledger Account Balances (in thousands)

Estimated Revenue

Taxes

For the Fiscal Year

Fines & Forfeits

Intergovernmental Revenue

Charges for Services

Revenues

Debits

6,048

303

497

370

Credits

Taxes

Fines & Forfeits

Intergovernmental Revenue

Charges for Services

Appropriations

Public Safety

General Government

6,080

308

497

368

1,636

3,375

Public Works

Culture & Recreation

Interfund Transfers Out

Expenditures

General Government

1,465

724

Estimated Other Financing Uses

48.

1,622

Public Safety

3,360

Public Works

1,443

Culture & Recreation

715

Encumbrances

General Government

12

I

Public Safety

13

Public Works

21

232

Culture & Recreation

0

Other Financing Uses

Interfund…

subsidiary ledgers for the fiscal year ended. Assume the beginning fund balances are $140 (in thousands) and that the budget was not

amended during the year.

Subsidiary Ledger Account Balances (in thousands)

For the Fiscal Year

Estimated Revenue

Taxes

Fines & Forfeits

City of Greenville

General Fund

Intergovernmental Revenue

Charges for Services

Revenues

Taxes

Fines & Forfeits

Intergovernmental Revenue

Charges for Services

Appropriations

General Government

Public Safety

Public Works

Culture & Recreation

Estimated Other Financing Uses

Interfund Transfers Out

Expenditures

General Government

Public Safety

Public Works

Culture & Recreation

Encumbrances

General Government

Public Safety

Public Works

D

Culture & Recreation

Other Financing Uses

Interfund Transfers Out

Debits

6,048

303

484

370

1,622

3,347

1,443

703

1

26

10

0

36

Credits

6,054

308

484

368

1,625

3,375

1,454

724

36

Required

a. Prepare a General Fund statement of revenues, expenditures, and changes in fund balance.

b. Prepare a…

The City of Lynnwood was recently incorporated and had the following transactions for the fiscal year ended December 31.

The city council adopted a General Fund budget for the fiscal year. Revenues were estimated at $2,000,000 and appropriations were $1,990,000.

Property taxes in the amount of $1,940,000 were levied. It is estimated that $9,000 of the taxes levied will be uncollectible.

A General Fund transfer of $25,000 in cash and $300,000 in equipment (with accumulated depreciation of $65,000) was made to establish a central duplicating internal service fund.

A citizen of Lynnwood donated marketable securities with a fair value of $800,000. The donated resources are to be maintained in perpetuity with the city using the revenue generated by the donation to finance an after-school program for children, which is sponsored by the culture and recreation function. Revenue earned and received as of December 31 was $40,000.

The city’s utility fund billed the city’s General Fund…

Chapter 3 Solutions

Governmental and Nonprofit Accounting (11th Edition)

Ch. 3 - Governmental budgeting and budgetary control are...Ch. 3 - Distinguish between the following types of...Ch. 3 - Prob. 3QCh. 3 - What are budgetary control points? How do they...Ch. 3 - Prob. 5QCh. 3 - Why might a local government not prepare and adopt...Ch. 3 - Revenue estimates and appropriations enacted are...Ch. 3 - In business accounting, a single general ledger...Ch. 3 - Illustrations 3-2 and 3-3 show Revenues Subsidiary...Ch. 3 - An interim budgetary comparison statement for a...

Ch. 3 - Prob. 11QCh. 3 - An annual budgetary comparison schedule for a...Ch. 3 - General budgets are most common for which of the...Ch. 3 - Special budgets are best defined as budgets a....Ch. 3 - Prob. 1.3ECh. 3 - Which of the following statements is false? a....Ch. 3 - Which of the following statements is true? a....Ch. 3 - Appropriation requests for the General Fund are...Ch. 3 - Which of the following statements would be true...Ch. 3 - Prob. 2.3ECh. 3 - Which of the following GAAP requirements for...Ch. 3 - Prob. 2.5ECh. 3 - Prob. 3.1ECh. 3 - Which of the following items does a government...Ch. 3 - The budget data presented in a school district...Ch. 3 - Allotments are best defined as a. legislative...Ch. 3 - Prob. 4ECh. 3 - Prob. 5ECh. 3 - (Budgetary EntriesGeneral Ledger) The city of...Ch. 3 - (General LedgerSubsidiary Ledgers Relationship,...Ch. 3 - (General Ledger Entries) Record the following...Ch. 3 - (Encumbrances) Record the following transactions...Ch. 3 - (Operating Budget Preparation) The finance...Ch. 3 - (Budgetary and Other EntriesGeneral and Subsidiary...Ch. 3 - Prob. 3PCh. 3 - (Budgetary Comparison StatementBudgetary Basis...Ch. 3 - (a) Prepare general ledger and subsidiary ledger...Ch. 3 - Using the information from C3-2 and assuming that...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. Deferred inflows of resources—property taxes of $51,200 at the end of the previous fiscal year were recognized as property tax revenue in the current year’s Statement of Revenues, Expenditures, and Changes in Fund Balance. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $200,000 is thought to be uncollectible, $349,000 would likely be collected during the 60-day period after the end of the fiscal year, and $53,800 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting. In addition to the expenditures recognized under modified accrual accounting, the City computed that $29,000 should be…arrow_forwardPrepare journal entries in general journal format to record the following transactions for the City of Dallas General Fund (subsidiary detail may be omitted) 1. The budget prepared for the fiscal year included total estimated revenues of $4,693,000, appropriations of $4,686,000 and estimated other financing uses of $225,000. 2. Purchase orders in the amount of $451,000 were mailed to vendors. 3. The current year’s tax levy of $4,005,000 was recorded; uncollectible taxes were estimated to be 2% of the tax levy. 4. Collections of delinquent taxes from prior years’ levies totaled $82,700; collections of the current year’s levy totaled $3,524,900. 5. Invoices were received and approved for payment for items ordered in documents recorded as encumbrances in transaction (#2) of this problem. The estimated liability for the related items was $351,200. Actual invoices were $353,500. 6. Revenue other than taxes collected during the year consisted of licenses and permits, $177,600;…arrow_forwardThe City of Greystone maintains its books so as to prepare fund accounting statements and prepares worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: The City levied property taxes for the current fiscal year in the amount of $8,000,000. At year-end, $720,000 of the taxes had not been collected. It was estimated that $330,000 of that amount would be collected during the 60 days after the end of the fiscal year and that $360,000 would be collected after that time and the balance would be uncollectible. The City had recognized the maximum of property taxes allowable under modified accrual accounting. $255,000 of property taxes had been deferred at the end of the previous year and was recognized under modified accrual as revenue in the current year. In addition to the expenditures reported under modified accrual accounting, the city computed that an additional $104,000…arrow_forward

- Assume that the County of Katerah maintains its books and records in a manner that facilitates preparation of the fund financial statements. The county formally integrates the budget into the accounting system and uses the encumbrance system. All appropriations lapse at year-end. At the beginning of the fiscal year, the county had the following balances in its accounts. All amounts are in thousands. Prepare the necessary entries for the current fiscal year. Cash $200 Fund balance unassigned 50 Reserve for encumbrances (committed or assigned) 150 (a) The county made the appropriate entry to restore the prior-year purchase commitments. (b) The county board approved a budget with revenues estimated to be $800 and expenditures of $750. (c) The county received the items that had been ordered in the prior year at an actual cost of $135. (d) The county ordered supplies at an estimated cost of $50 and equipment at an estimated cost of $70. (e) The county incurred salaries and other operating…arrow_forwardThe following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year’s appropriation. The budget prepared for the fiscal year 2020 was as follows: Estimated Revenues: Taxes $ 1,957,000 Licenses and permits 374,000 Intergovernmental revenue 399,000 Miscellaneous revenues 64,000 Total estimated revenues 2,794,000 Appropriations: General government 475,200 Public safety 890,200 Public works 654,200 Health and welfare 604,200 Miscellaneous 88,000 Total appropriations 2,711,800 Budgeted increase in fund balance $ 82,200 Encumbrances issued against the appropriations during the year were as follows: General government $ 60,000 Public safety 252,000 Public works 394,000 Health and…arrow_forwardEdwards City has the following information for its general fund for the upcoming fiscal year. Which of the following would be the appropriate effect to budgetary fund balance when the budget is recorded? Estimated revenue Appropriations Property tax 3,500,000 Salaries 2,690,000 Sales tax 490,000 Capital items 1,320,000 Other 50,000 Other 15,000 None of these Credit budgetary fund balance $30,000 Credit budgetary fund balance $15,000 Debit budgetary fund balance $30,000arrow_forward

- The board of commissioners of Perry City approved the city budget for the year starting July 1, 2019, which indicated estimated revenue of $1,000,000 and appropriations of $900,000. When the city CLOSES OUT the budget at the end of the fiscal year, the entry would include: O A) a debit to Budgetary Fund Balance - Unassigned in the amount of $100,000. B) a credit to Budgetary Fund Balance – Unassigned in the amount of $100,000. C) a debit to Appropriations in the amount of $900,000. D) a debit to Estimated Revenues in the amount of $1,000,000. E) both A. and C.arrow_forward3. The pre-closing trial balance of the General Fund for the City of Taif shows the following balances at the end of its fiscal year. Budgetary fund balance SAR 20,000 Fund balance, beginning (actual) 150.000 Estimated revenues 830.000 Appropriations 810.000 Revenues (actual) 725.000 Expenditures 675.000 Based on information presented above Prepare closing entries for the budgetary and financial accounts.arrow_forwardThe City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forward

- The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forward6. Franklin County issued $4,300,000, 3 percent serial bonds, paying interest on January 1 and July 1. The bonds were sold on June 1 for 102. The county is required to use all accrued interest and premiums to service the debt. Any additional resources needed to service the debt are to come from the General Fund. The county's fiscal year-end is December 31. Required Prepare in general journal form the budgetary entry the debt service fund would make to account for this serial bond issue. What, if any, adjustment would need to be made to the General Fund budget to account for this serial bond issue? Medium Answer Answer any TWO questions (2x 5 marks = 10 marks) Section B -arrow_forwardThe following transactions relate to the General Fund of the City of Buffalo Falls for the year ended December 31, 2020: Beginning balances were: Cash, $94,000; Taxes Receivable, $191,000; Accounts Payable, $53,000; and Fund Balance, $232,000. The budget was passed. Estimated revenues amounted to $1,240,000 and appropriations totaled $1,237,200. All expenditures are classified as General Government. Property taxes were levied in the amount of $920,000. All of the taxes are expected to be collected before February 2021. Cash receipts totaled $890,000 for property taxes and $300,000 from other revenue. Contracts were issued for contracted services in the amount of $97,000. Contracted services were performed relating to $87,000 of the contracts with invoices amounting to $85,200. Other expenditures amounted to $968,000. Accounts payable were paid in the amount of $1,100,000. The books were closed. Required:a. Prepare journal entries for the above transactions.b. Prepare a Statement of…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education

What is Fund Accounting?; Author: Aplos;https://www.youtube.com/watch?v=W5D5Dr0j9j4;License: Standard Youtube License