Governmental and Nonprofit Accounting (11th Edition)

11th Edition

ISBN: 9780133799569

Author: Robert J. Freeman, Craig D. Shoulders, Dwayne N. McSwain, Robert B. Scott

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 3, Problem 2C

(a) Prepare general ledger and subsidiary ledger entries to record the following transactions of the City of Ann Arbor, Michigan, Community Television Network Special Revenue Fund for the year ended June 30, 20X3. (b) Reconcile the general ledger and the subsidiary ledgers at year end. (c) Close the accounts.

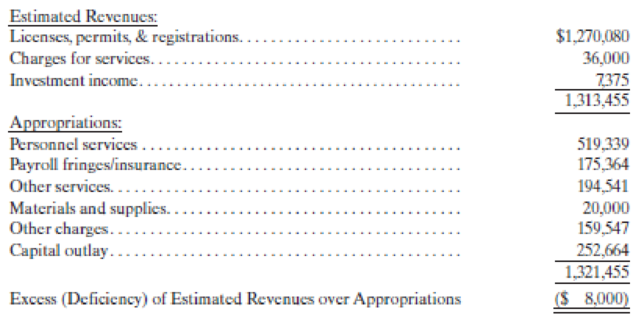

- 1. The Ann Arbor City Council adopted the following budget on the modified accrual basis for the Community Television Network Special Revenue Fund:

- 2. The city collected cash for the network as follows:

- 3. City Council revised the Community Television Network Special Revenue Fund appropriations for “Personnel services” and “Payroll fringes/insurance” upward by $40,000 and $15,000, respectively, as a result of hiring an additional employee and minor modifications to the employees’ insurance benefits. Appropriations for “Materials and supplies” and “Capital outlay” were reduced by $3,000 and $60,000, respectively.

- 4. The payroll was approved and paid, $559,339.

- 5. Payroll

fringe benefit and insurance costs of $190,000 were incurred during the year; $10,000 was not paid by year end. - 6. The network ordered materials and supplies with an estimated cost of $17,000 and equipment expected to cost $192,664.

- 7. “Other services” of $194,000 and “Other charges” of $159,547 were incurred and paid.

- 8. The network received the materials and supplies ordered. The actual cost was $16,980. The network also received must of the equipment ordered, but orders for $50,000 of transmission equipment had not been received by year end. The actual cost of the equipment received was equal to the expected costs.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Assume that the City of Pasco maintains its books and records in a manner that facilitates preparation of the fund financial statements. The city engaged in the following transactions related to its general fund during the current fiscal year. The city formally integrates the budget into the accounting records. The city does not maintain an inventory of supplies. All amounts are in thousands. Prepare, in summary form, the appropriate journal entries.

(a) The city council approved a budget with revenues estimated to be $800 and expenditures of $785.

(b) The city ordered supplies at an estimated cost of $25 and equipment at an estimated cost of $20.

(c) The city incurred salaries and other operating expenses during the year totaling $730. The city paid for these items in cash.

(d) The city received the supplies at an actual cost of $23.

(e) The city collected revenues of $795.

1. Assume that the City of Juneau maintains its books and records to facilitate the preparation of its fund financial statements. The City pays its employees bi-weekly on Friday. The fiscal year ended on Wednesday, June 30. Employees had been paid on Friday, June 25. The employees paid from the General Fund had earned $120,000 on Monday, Tuesday, and Wednesday (June 28, 29, and 30). What entry, if any, should be made in the City s General Fund?

a. Debit Expenditures; Credit Wages and Salaries Payable.

b. Debit Expenses; Credit Wages and Salaries Payable.

c. Debit Expenditures; Credit Encumbrances.

d. No entry is required.

Greenville has provided the following Information from its General Fund Revenues and Appropriations/Expenditure/Encumbrances

subsidiary ledgers for the fiscal year ended. Assume the beginning fund balances are $149 (in thousands) and that the budget was not

amended during the year.

City of Greenville

General Fund

Subsidiary Ledger Account Balances (in thousands)

Estimated Revenue

Taxes

For the Fiscal Year

Fines & Forfeits

Intergovernmental Revenue

Charges for Services

Revenues

Debits

6,048

303

497

370

Credits

Taxes

Fines & Forfeits

Intergovernmental Revenue

Charges for Services

Appropriations

Public Safety

General Government

6,080

308

497

368

1,636

3,375

Public Works

Culture & Recreation

Interfund Transfers Out

Expenditures

General Government

1,465

724

Estimated Other Financing Uses

48.

1,622

Public Safety

3,360

Public Works

1,443

Culture & Recreation

715

Encumbrances

General Government

12

I

Public Safety

13

Public Works

21

232

Culture & Recreation

0

Other Financing Uses

Interfund…

Chapter 3 Solutions

Governmental and Nonprofit Accounting (11th Edition)

Ch. 3 - Governmental budgeting and budgetary control are...Ch. 3 - Distinguish between the following types of...Ch. 3 - Prob. 3QCh. 3 - What are budgetary control points? How do they...Ch. 3 - Prob. 5QCh. 3 - Why might a local government not prepare and adopt...Ch. 3 - Revenue estimates and appropriations enacted are...Ch. 3 - In business accounting, a single general ledger...Ch. 3 - Illustrations 3-2 and 3-3 show Revenues Subsidiary...Ch. 3 - An interim budgetary comparison statement for a...

Ch. 3 - Prob. 11QCh. 3 - An annual budgetary comparison schedule for a...Ch. 3 - General budgets are most common for which of the...Ch. 3 - Special budgets are best defined as budgets a....Ch. 3 - Prob. 1.3ECh. 3 - Which of the following statements is false? a....Ch. 3 - Which of the following statements is true? a....Ch. 3 - Appropriation requests for the General Fund are...Ch. 3 - Which of the following statements would be true...Ch. 3 - Prob. 2.3ECh. 3 - Which of the following GAAP requirements for...Ch. 3 - Prob. 2.5ECh. 3 - Prob. 3.1ECh. 3 - Which of the following items does a government...Ch. 3 - The budget data presented in a school district...Ch. 3 - Allotments are best defined as a. legislative...Ch. 3 - Prob. 4ECh. 3 - Prob. 5ECh. 3 - (Budgetary EntriesGeneral Ledger) The city of...Ch. 3 - (General LedgerSubsidiary Ledgers Relationship,...Ch. 3 - (General Ledger Entries) Record the following...Ch. 3 - (Encumbrances) Record the following transactions...Ch. 3 - (Operating Budget Preparation) The finance...Ch. 3 - (Budgetary and Other EntriesGeneral and Subsidiary...Ch. 3 - Prob. 3PCh. 3 - (Budgetary Comparison StatementBudgetary Basis...Ch. 3 - (a) Prepare general ledger and subsidiary ledger...Ch. 3 - Using the information from C3-2 and assuming that...

Additional Business Textbook Solutions

Find more solutions based on key concepts

Fundamental and Enhancing Characteristics. Identify whether the following items are fundamental characteristics...

Intermediate Accounting

How would the decision to dispose of a segment of operations using a split-off rather than a spin-off impact th...

Advanced Financial Accounting

This year, Prewer Inc. received a 160,000 dividend on its investment consisting of 16 percent of the outstandin...

Principles Of Taxation For Business And Investment Planning 2020 Edition

E6-14 Using accounting vocabulary

Learning Objective 1, 2

Match the accounting terms with the corresponding d...

Horngren's Accounting (11th Edition)

Calculating certain information using the direct method (Learning Objective 4) 20-25 min. Trudeaus Marine, Inc....

Financial Accounting, Student Value Edition (5th Edition)

The amount that should be recorded by Company R for building under historical cost principle.

Financial Accounting (11th Edition)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. Deferred inflows of resources—property taxes of $51,200 at the end of the previous fiscal year were recognized as property tax revenue in the current year’s Statement of Revenues, Expenditures, and Changes in Fund Balance. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $200,000 is thought to be uncollectible, $349,000 would likely be collected during the 60-day period after the end of the fiscal year, and $53,800 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting. In addition to the expenditures recognized under modified accrual accounting, the City computed that $29,000 should be…arrow_forwardThe City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forwardThe City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forward

- Park City uses encumbrance accounting and formally integrates its budget into the general fund's accounting records. For the year ending July 31, Year 1, the following budget was adopted: Estimated revenues $30,000,000 Appropriations $27,000,000 Estimated transfer to debt service fund $900,000 Park's budgetary fund balance is a $3,000,000 credit balance $3,000,000 debit balance $2,100,000 credit balance O $2,1000,000 debit balancearrow_forwardIn approving the budget of the City of Troy, the city council appropriated an amount less than expected revenues, what will be the result of this action .a An increase in outstanding encumbrances by the of the fiscal year .b A credit to budgetary fund balance .C A debit to budgetary fund balance .d A necessity for compensatory offsetting action in the debt service fundarrow_forward4. City of Atwater wants to prepare closing entries at the end of a fiscal year for budgetary and operating statement control accounts in the general ledger of the General Fund. Following balance are belong to the City. Appropriations, $7,824,000%3; Financing Uses, $2,766,000; Estimated Revenues, $7,798,000; Encumbrances,$0; Expenditures, $5,900,0003; Uses, $2,770,000; Revenues, $8,980,000. Required Show in general journal form the entry needed to close all of the preceding accounts that should be closed as of the end of the fiscal year. Estimated Other Other Financingarrow_forward

- Journal entries for a series of transactionsPrepare journal entries in the General Fund for each of the following events relating to the City of Bar Harbor (all amounts in $1,000s). a. The citizens approve the following budget for the year: ESTIMATED REVENUES $78,924 ESTIMATED OTHER FINANCING SOURCES 2,000 APPROPRIATIONS (77,273) BUDGETARY FUND BALANCE $3,651 General Journal Description Debit Credit ESTIMATED OTHER FINANCING SOURCES APPROPRIATIONS b. The City records the following revenues (on account) and other financing sources (paid in cash) during the year: 1. Revenues-real estate and personal property taxes $68,650 2. Revenues-intergovernmental 12,685 3. Other financing sources-bond proceeds 2,400 Description Debit Credit 1. 2. 3. c. The City issues purchase invoices totaling $78,508…arrow_forwardThe City of Jonesboro engaged in the following transactions during the fiscal year ended September 30, 2018. Record the following transactions related to interfund transfers. Be sure to indicate in which fund the entry is being made. a. The city transferred $400,000 from the general fund to a debt service fund to make the interest payments due during the fiscal year. The payments due during the fiscal year were paid. The city also transferred $200,000 from the general fund to a debt service fund to advance-fund the $200,000 interest payment due October 15, 2019. b. The city transferred $75,000 from the Air Operations Special Revenue Fund to the general fund to close out the operations of that fund. c. The city transferred $150,000 from the general fund to the city’s Electric Utility Enterprise Fund to pay for the utilities used by the general and administrative offices during the year. d. The city transferred the required pension contribution of $2 million from the general fund to the…arrow_forwardCraven City has an electric utility fund that is managed by Tara Perkins. Show the journal entries that would be recorded in the general fund for the following transactions that occurred during the fiscal year ended June 30, 2021 and identify the income statement effect of each entry: 1. The electric utility fund provided electric services to city departments accounted for in the general fund. The electric utility fund bills $100,000 for these services. 2. The general fund pays the amount owed.arrow_forward

- 3. The pre-closing trial balance of the General Fund for the City of Taif shows the following balances at the end of its fiscal year. Budgetary fund balance SAR 20,000 Fund balance, beginning (actual) 150.000 Estimated revenues 830.000 Appropriations 810.000 Revenues (actual) 725.000 Expenditures 675.000 Based on information presented above Prepare closing entries for the budgetary and financial accounts.arrow_forwardFor each of the following events or transactions, prepare the necessacry journal entries and identify the fund or funds that will be affected. 1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and maintenance 2. A county government that serves as a tax collection agency for all towns and cities located within the county collects county sales taxes totaling $125,000 for the month. 3. A $1,000,000 bond offering was issued, with a premium of $50,000, to subsidize the construction of a city visitor center. 4. A town receives a donation of $50,000 in bonds. The bonds should be held indefinitely, but bond income is to be donated to the local zoo. The zoo is associated with the town. 5. A central printing shop is established with a $150,000 nonreciprocal transfer from the general fund. 6. A $1,000,000 revenue bond offering was issued at par by a fund that provides water and sewer services to…arrow_forwardFor each of the following events or transactions, prepare the necessacry journal entries and identify the fund or funds that will be affected. 1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and maintenance 2. A county government that serves as a tax collection agency for all towns and cities located within the county collects county sales taxes totaling $125,000 for the month. 3. A $1,000,000 bond offering was issued, with a premium of $50,000, to subsidize the construction of a city visitor center. 4. A town receives a donation of $50,000 in bonds. The bonds should be held indefinitely, but bond income is to be donated to the local zoo. The zoo is associated with the town. 5. A central printing shop is established with a $150,000 nonreciprocal transfer from the general fund. 6. A $1,000,000 revenue bond offering was issued at par by a fund that provides water and sewer services to…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education

What is Fund Accounting?; Author: Aplos;https://www.youtube.com/watch?v=W5D5Dr0j9j4;License: Standard Youtube License