Concept explainers

Videos

The general ledger of Red Storm Cleaners at January 1, 2018, includes the following account balances:

| Accounts | Debits | Credits |

| Cash | $20,000 | |

| 8,000 | ||

| Supplies | 4,000 | |

| Equipment | 15,000 | |

| $ 5,000 | ||

| Salaries Payable | 7,500 | |

| Common Stock | 25,000 | |

| 9,500 | ||

| Totals | $47,000 | $47,000 |

The following is a summary of the transactions for the war:

a. March 12 Provide services to customers, $60,000, of which $21,000 is on account.

b. May 2 Collect on accounts receivable, $18,000.

c. June 30 Issue shares of common stock in exchange for $6,000 cash.

d. August 1 Pay salaries, $26,000 (of which $7,500 is for salaries payable in 2017).

e. September 25 Pay repairs and maintenance expenses. $13,000.

f. October 19 Purchase equipment for $8,000 cash.

g. December 30 Pay $1,100 cash dividends to stockholders.

Required:

1. Set up the necessary T-accounts and enter the beginning balances from the

2. Record each of the summary transactions listed above.

3. Post the transactions to the accounts.

4. Prepare an unadjusted trial balance.

5. Record

6. Post adjusting entries.

7. Prepare an adjusted trial balance.

8. Prepare an income statement for 2018 and a classified balance sheet as of December 31, 2018.

9. Record closing entries.

10. Post closing entries.

11. Prepare a post-closing trial balance.

Requirement – 1

To prepare: The T-accounts and enter the beginning balance from the trial balance.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

The T-accounts of given item in trial balance are as follows:

| Cash | |||

| Jan. 1 | $20,000 | ||

| Bal. | $20,000 | ||

| Equipment | |||

| Jan. 1 | $15,000 | ||

| Bal. | $15,000 | ||

| Common stock | |||

| Jan. 1 | $25,000 | ||

| Bal. | $25,000 | ||

|

Accounts receivables | |||

| Jan. 1 | $8,000 | ||

| Bal. | $8,000 | ||

| Supplies | |||

| Jan. 1 | $4,000 | ||

| Bal. | $4,000 | ||

| Salaries payable | |||

| Jan. 1 | $7,500 | ||

| Bal. | $7,500 | ||

| Accumulated Depreciation | |||

| Jan. 1 | $5,000 | ||

| Bal. | $5,000 | ||

| Retained earnings | |||

| Jan. 1 | $9,500 | ||

| Bal. | $9,500 | ||

Requirement – 2

To record: The journal entries for given transactions.

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

The journal entries for given transactions of Company R are as follows:

| Date | Account Title and Explanation | Debit($) | Credit($) |

| 2018 | Accounts receivable | 21,000 | |

| March 12 | Cash | 39,000 | |

| Service revenue | 60,000 | ||

| (To record the recognized service revenue on account and cash) | |||

| 2018 | Cash | 18,000 | |

| May, 2 | Accounts receivable | 18,000 | |

| (To record cash collection from customer) | |||

| 2018 | Cash | 6,000 | |

| June 30 | Common stock | 6,000 | |

| (To record the cash received from issuance of common stock) | |||

| 2018 | Salaries payable | 7,500 | |

| August 1 | Salaries expense | 18,500 | |

| Cash | 26,000 | ||

| (To record the payment of current and past salaries) | |||

| 2018 | Repairs and maintenance expense | 13,000 | |

| September 25 | Cash | 13,000 | |

| (To record the payment of repairs and maintenance expense) | |||

| 2018 | Equipment | 8,000 | |

| October 19 | Cash | 8,000 | |

| (To record purchase of equipment in cash) | |||

| 2018 | Dividends | 1,100 | |

| December 30 | Cash | 1,100 | |

| (To record the payment of dividends) | |||

Table (1)

Requirement – 3

To post: The transactions to T-accounts.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

T-accounts of above transactions are as follows:

| Cash | |||

| Jan. 1 | $20,000 | Aug. 1 | $26,000 |

| Mar. 12 | $39,000 | Sep. 25 | $13,000 |

| May 2 | $18,000 | Oct. 19 | $8,000 |

| Jun. 30 | $6,000 | Dec. 30 | $1,100 |

| Total | $83,000 | Total | $48,100 |

| Bal. | $34,900 | ||

| Equipment | |||

| Jan. 1 | $15,000 | ||

| Oct. 19 | $8,000 | ||

| Bal. | $23,000 | ||

| Common stock | |||

| Jan. 1 | $25,000 | ||

| Jun. 30 | $6,000 | ||

| Bal. | $31,000 | ||

| Dividends | |||

| Jan. 1 | $0 | ||

| Dec. 30 | $1,100 | ||

| Bal. | $1,100 | ||

| Accounts receivables | |||

| Jan. 1 | $8,000 | ||

| Mar. 12 | $21,000 | May 2 | $18,000 |

| Total | $29,000 | Total | $18,000 |

| Bal. | $11,000 | ||

| Accumulated Depreciation | |||

| Jan. 1 | $5,000 | ||

| Bal. | $5,000 | ||

| Supplies | |||

| Jan. 1 | $4,000 | ||

| Bal. | $4,000 | ||

| Salaries payable | |||

| Aug. 1 | $7,500 | Jan. 1 | $7,500 |

| Bal. | $0 | ||

| Retained earnings | |||

| Jan. 1 | $9,500 | ||

| Bal. | $9,500 | ||

| Salaries expense | |||

| Jan. 1 | $0 | ||

| Aug. 1 | $18,500 | ||

| Bal. | $18,500 | ||

| Service revenue | |||

| Jan. 1 | $0 | ||

| Mar. 12 | $60,000 | ||

| Bal. | $60,000 | ||

| Repairs and maintenance expense | |||

| Jan. 1 | $0 | ||

| Sep. 25 | $13,000 | ||

| Bal. | $13,000 | ||

Requirement – 4

To prepare: The unadjusted trial balance of Company R.

Explanation of Solution

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts before making adjusting journal entries at the end of the period.

| Company R | ||

| Unadjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit | Credit |

| Cash | $34,900 | |

| Accounts Receivable | 11,000 | |

| Supplies | 4,000 | |

| Equipment | 23,000 | |

| Accumulated depreciation | 5,000 | |

| Salaries payable | 0 | |

| Common stock | 31,000 | |

| Retained earnings | 9,500 | |

| Dividends | 1,100 | |

| Service revenue | 60,000 | |

| Salaries expense | 18,500 | |

| Repairs and maintenance expense | 13,000 | |

| Depreciation expense | 0 | |

| Supplies expense | 0 | |

| Totals | $105,500 | $105,500 |

Table (2)

Therefore, the total of debit, and credit columns of unadjusted trial balance is $105,500 and agree.

Requirement – 5

To record: The given adjusting entries of Company R.

Explanation of Solution

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. The purpose of adjusting entries is to adjust the revenue, and the expenses during the period in which they actually occurs.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Adjusting entries of Company R are as follows:

Accrued salaries:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Salaries expense | 1,100 | ||

| Salaries payable | 1,100 | |||

| (To record the salaries expense incurred at the end of the accounting year) |

Table (3)

Following is the rule of debit and credit of above transaction:

- Salaries expense is an expense, and it decreased the value of stockholder’s equity. Therefore, it is debited.

- Salaries payable is a liability account. There is a decrease in liability, therefore it is credited.

Depreciation expense:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Depreciation Expense | 5,000 | ||

| Accumulated Depreciation | 5,000 | |||

| (To record the amount of depreciation for the year) |

Table (4)

Following is the rule of debit and credit of above transaction:

- Depreciation expense is an expense, and it decreased the value of stockholder’s equity. Therefore, it is debited.

- Accumulated depreciation is a contra-asset account. There is a decrease in assets, therefore it is credited.

Office supplies expense:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Supplies expense | 1,200 | ||

| Supplies | 1,200 | |||

| (To record the supplies expense incurred at the end of the accounting year) |

Table (5)

Following is the rule of debit and credit of above transaction:

- Supplies expense is an expense, and it decreased the value of stockholder’s equity. Therefore, it is debited.

- Supplies are an asset account. There is a decrease in assets, therefore it is credited.

Requirement – 6

To post: The adjusting entries to appropriate T-accounts.

Explanation of Solution

| Depreciation expense | |||

| Jan. 1 | $0 | ||

| Dec. 31 | $5,000 | ||

| Bal. | $5,000 | ||

| Accumulated Depreciation | |||

| Jan. 1 | $5,000 | ||

| Dec. 31 | $5,000 | ||

| Bal. | $10,000 | ||

| Salaries expense | |||

| Jan. 1 | $0 | ||

| Aug. 1 | $18,500 | ||

| Dec. 31 | $1,100 | ||

| Bal. | $19,600 | ||

| Supplies expense | |||

| Jan. 1 | $0 | ||

| Dec. 31 | $2,800 | ||

| Bal. | $2,800 | ||

| Supplies | |||

| Jan. 1 | $4,000 | Dec. 31 | $2,800 |

| Total | $4,000 | Total | $2,800 |

| Bal. | $1,200 | ||

| Salaries payable | |||

| Aug. 1 | $7,500 | Jan. 1 | $7,500 |

| Dec. 11 | $1,100 | ||

| Total | $7,500 | Total | $8,600 |

| Bal. | $1,100 | ||

Requirement – 7

To prepare: The adjusted trial balance of Company R.

Explanation of Solution

Adjusted trial balance:

Adjusted trial balance is a summary of all the ledger accounts, and it contains the balances of all the accounts after the adjustment entries are journalized, and posted.

Adjusted trial balance of Company R is as follows:

| Company R | ||

| Adjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit | Credit |

| Cash | 34,900 | |

| Accounts Receivable | 11,000 | |

| Supplies | 1,200 | |

| Equipment | 23,000 | |

| Accumulated depreciation | 10,000 | |

| Salaries payable | 1,100 | |

| Common stock | 31,000 | |

| Retained earnings | 9,500 | |

| Dividends | 1,100 | |

| Service revenue | 60,000 | |

| Salaries expense | 19,600 | |

| Repairs and maintenance expense | 13,000 | |

| Depreciation expense | 5000 | |

| Supplies expense | 2,800 | |

| Totals | $111,600 | $111,600 |

Table (6)

Therefore, the total of debit, and credit columns of adjusted trial balance is $111,600 and agree.

Requirement – 8

To prepare: An income statement for 2018 and classified balance sheet as on December 31, 2018.

Explanation of Solution

Income statement:

This is the financial statement of a company which shows all the revenues earned and expenses incurred by the company over a period of time.

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

Income statement:

Income statement of Company R is as follows:

| Company R | ||

| Income statement | ||

| For the year ended December 31, 2018 | ||

| $ | $ | |

| Service revenue (A) | 60,000 | |

| Expenses: | ||

| Salaries expense | 19,600 | |

| Repairs and maintenance expense | 13,000 | |

| Depreciation expense | 5,000 | |

| Supplies expense | 2,800 | |

| Total expense (B) | 40,400 | |

| Net income

| 19,600 | |

Table (7)

Therefore, the net income of Company R is $19,600.

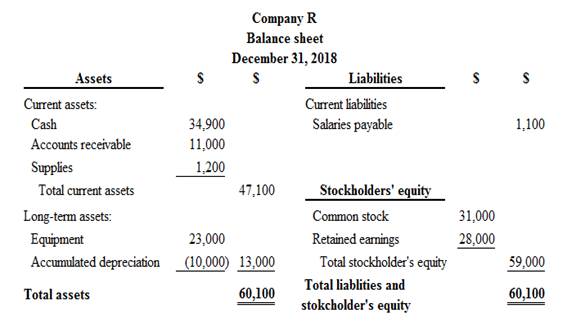

Classified balance sheet:

Classified balance sheet of Company R is as follows:

Figure (1)

Figure (1)

Therefore, the total assets of Company R are $60,100, and the total liabilities and stockholders’ equity are $60,100.

Working note:

Calculation of ending balance retained earnings

Requirement – 9

To record: The necessary closing entries of Company R.

Explanation of Solution

Closing entries:

Closing entries are those journal entries, which are passed to transfer the final balances of temporary accounts, (all revenues account, all expenses account and dividend) to the retained earnings. Closing entries produce a zero balance in each temporary account.

Closing entries of Company R is as follows:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| 2018 | Service revenue | 60,000 | ||

| December 31 | Retained earnings | 60,000 | ||

| (To close all revenue account) | ||||

| 2018 | Retained earnings | 40,400 | ||

| December 31 | Salaries expense | 19,600 | ||

| Repairs and maintenance expense | 13,000 | |||

| Depreciation expense | 5,000 | |||

| Supplies expense | 2,800 | |||

| (To close all the expenses account) | ||||

| 2018 | Retained earnings | 1,100 | ||

| December 31 | Dividends | 1,100 | ||

| (To close the dividends account) | ||||

Table (8)

Requirement – 10

To post: The closing entries to the T-accounts.

Explanation of Solution

| Depreciation expense | |||

| Jan. 1 | $0 | ||

| Dec. 31 | $5,000 | Dec. 31 | $5,000 |

| Bal. | $0 | ||

| Salaries expense | |||

| Jan. 1 | $0 | ||

| Aug. 1 | $18,500 | ||

| Dec. 31 | $1,100 | Dec. 31 | $19,600 |

| Bal. | $0 | ||

| Supplies expense | |||

| Jan. 1 | $0 | ||

| Dec. 31 | $2,800 | Dec. 31 | $2,800 |

| Bal. | $0 | ||

| Repairs and maintenance expense | |||

| Jan. 1 | $0 | ||

| Sep. 25 | $13,000 | Dec. 31 | $13,000 |

| Bal. | $0 | ||

| Dividends | |||

| Jan. 1 | $0 | ||

| Dec. 30 | $1,100 | Dec. 31 | $1,100 |

| Bal. | $0 | ||

| Service revenue | |||

| Jan. 1 | $0 | ||

| Dec. 31 | $60,000 | Mar. 12 | $60,000 |

| Bal. | $0 | ||

| Retained earnings | |||

| Dec. 31 | $40,400 | Jan. 1 | $9,500 |

| Dec. 31 | $1,100 | Dec. 31 | $60,000 |

| Total | $41,500 | Total | $69,500 |

| Bal. | $28,000 | ||

Requirement – 11

To prepare: A post-closing trial balance of Company R.

Explanation of Solution

Post-closing trial balance:

The post-closing trial balance is a summary of all ledger accounts, and it shows the debit and the credit balances after the closing entries are journalized and posted. The post-closing trial balance contains only permanent (balance sheet) accounts, and the debit and the credit balances of permanent accounts should agree.

Post-closing trial balance of Company R is as follows:

| Company R | ||

| Post-closing trial balance | ||

| December 31, 2018 | ||

| Accounts | Debit | Credit |

| Cash | $34,900 | |

| Accounts Receivable | 11,000 | |

| Supplies | 1,200 | |

| Equipment | 23,000 | |

| Accumulated depreciation | 10,000 | |

| Salaries payable | 1,100 | |

| Common stock | 31,000 | |

| Retained earnings | 28,000 | |

| Totals | $70,100 | $70,100 |

Table (9)

Therefore, the total of debit, and credit columns of post-closing trial balance is $70,100 and agree.

Want to see more full solutions like this?

Chapter 3 Solutions

FINANCIAL ACCOUNTINGLL W/CONNECT >IC<

- Required information [The following information applies to the questions displayed below.] The general ledger of Zips Storage at January 1, 2024, includes the following account balances: The following is a summary of the transactions for the year: January 9 February 12 April 25 May 6 July 15 September 10 October 31 November 20 December 30 Provide storage services for cash, $135, 100, and on account, $52, 700. Collect on accounts receivable, $51, 600. Receive cash in advance from customers, $13,000. Purchase supplies on account, $9, 400. Pay property taxes, $8,600. Pay on accounts payable, $11,500. Pay salaries, $124, 600. Issue shares of common stock in exchange for $28,000 cash. Pay $2,900 cash dividends to stockholders.Prepare an unadjusted trial balance.arrow_forwardAnalyzing the Accounts The controller for Summit Sales Inc. provides the following information on transactions that occurred during the year: a. Purchased supplies on credit, $18,600 b. Paid $14,800 cash toward the purchase in Transaction a c. Provided services to customers on credit1 $46,925 d. Collected $39,650 cash from accounts receivable e. Recorded depreciation expense, $8,175 f. Employee salaries accrued, $15,650 g. Paid $15,650 cash to employees for salaries earned h. Accrued interest expense on long-term debt, $1,950 i. Paid a total of $25,000 on long-term debt, which includes $1.950 interest from Transaction h j. Paid $2,220 cash for l years insurance coverage in advance k. Recognized insurance expense, $1,340, that was paid in a previous period l. Sold equipment with a book value of $7,500 for $7,500 cash m. Declared cash dividend, $12,000 n. Paid cash dividend declared in Transaction m o. Purchased new equipment for $28,300 cash. p. Issued common stock for $60,000 cash q. Used $10,700 of supplies to produce revenues Summit Sales uses the indirect method to prepare its statement of cash flows. Required: 1. Construct a table similar to the one shown at the top of the next page. Analyze each transaction and indicate its effect on the fundamental accounting equation. If the transaction increases a financial statement element, write the amount of the increase preceded by a plus sign (+) in the appropriate column. If the transaction decreases a financial statement element, write the amount of the decrease preceded by a minus sign (-) in the appropriate column. 2. Indicate whether each transaction results in a cash inflow or a cash outflow in the Effect on Cash Flows column. If the transaction has no effect on cash flow, then indicate this by placing none in the Effect on Cash Flows column. 3. For each transaction that affected cash flows, indicate whether the cash flow would be classified as a cash flow from operating activities, cash flow from investing activities, or cash flow from financing activities. If there is no effect on cash flows, indicate this as a non-cash activity.arrow_forwardCatherines Cookies has a beginning balance in the Accounts Payable control total account of $8,200. In the cash disbursements journal, the Accounts Payable column has total debits of $6,800 for November. The Accounts Payable credit column in the purchases journal reveals a total of $10,500 for the current month. Based on this information, what is the ending balance in the Accounts Payable account in the general ledger?arrow_forward

- On March 24, MS Companys Accounts Receivable consisted of the following customer balances: S. Burton 310 A. Tangier 240 J. Holmes 504 F. Fullman 110 P. Molty 90 During the following week, MS made a sale of 104 to Molty and collected cash on account of 207 from Burton and 360 from Holmes. Prepare a schedule of accounts receivable for MS at March 31, 20--.arrow_forwardTask 2: Evaluate the company's efficiency in collecting its accounts receivable during the fiscal year ended 31 December 2021. Use the company's information from its annual reports: Receivables as of 31 December 2020 $4,468,392 $4,972,722 $45,349,943 Receivables as of 31 December 2021 Sales revenue for year ended 31 December 2021 1. Calculate the company's number of days of sales outstanding (DSO) for the fiscal year ended 31 December 2021. (Use the average receivables to calculate the ratio). Not Accounting receivable Average Day's sales in receivable = 154; 2. Interpret the calculated ratio. 3. Assume that the industry average DSO ratio is 60 days. Based on this information and the subject company's DSO ratio, critically evaluate the company's credit policy and its implications.arrow_forwardLoucks Company established a $330 petty cash fund on October 2, 2024. The fund is replenished at the end of each month. At the end of October 2024, the fund contained $89 in cash and the following receipts: Office supplies $ 102 Advertising 74 Postage 33 Miscellaneous 32 Required: Prepare the necessary general journal entries to establish the petty cash fund on October 2 and to replenish the fund on October 31. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field.arrow_forward

- Jones, a company, prepares monthly Receivables and Payables ledger control accounts. At 1 June 20X5 the following balances existed in the company's records. Receivables ledger balances Dr $ 54,000 Payables ledger balances CR $ 43,000 During the month of June, the transactions of Jones included the $ Credit sales • 251,000 Cash sales -34,000 Credit sales returns 11,000 Amounts received from credit customers • 242,000 Dishonoured cheques • 500 Cash discounts allowed Irrecoverable debts written off 3,000 Increase in allowance for receivables 1,000 Interest charged to customers 1,200 - 1,400 Contras between receivables and payables -800 You are required to prepare the receivables ledger control account for the month of June, showing the balance as at 30 June 20X5.arrow_forwardAN Jensen Company's general ledger included the following selected accounts (in thousands) at December 31, 2021: Accounts payable $1,077.3 Accounts receivable 590.4 Accumulated depreciation—equipment 858.7 Allowance for doubtful accounts 35.4 Bad debt expense 91.3 Cash 395.6 Cost of goods sold 660.4 Equipment 1,732.8 Interest revenue 19.7 Merchandise inventory 630.9 Notes receivable—due in 2022 96.0 Notes receivable—due in 2025 191.1 Prepaid expenses 20.1 Sales 4,565.5 Sales discounts 31.3 Short-term investments 194.9 Supplies 21.7 Unearned revenue 56.3 Additional information: 1.On December 31, 2020, Accounts Receivable was $611.1 thousand and the Allowance for Doubtful Accounts was $36.6 thousand. 2.The receivables turnover was 8.3 the previous year. Instructions a. Prepare the assets section of the balance sheet. b. Calculate the receivables turnover and average collection period. Compare these results with the previous year's results and comment on any trendsarrow_forwardTask 2: Evaluate the company's efficiency in collecting its accounts receivable during the fiscal year ended 31 December 2021. Use the company's information from its annual reports: Receivables as of 31 December 2020 Receivables as of 31 December 2021 $4,468,392 $4,972,722 $45,349,943 Sales revenue for year ended 31 December 2021 1. Calculate the company's number of days of sales outstanding (DSO) for the fiscal year ended 31 December 2021. (Use the average receivables to calculate the ratio). Net = 2.37 = Accounting receivable: Average Day's sales in receivable = 154. 2. Interpret the calculated ratio. 3. Assume that the industry average DSO ratio is 60 days. Based on this information and the subject company's DSO ratio, critically evaluate the company's credit policy and its implications.arrow_forward

- The following are excerpts from the financial statements of 2018 and 2019 of Mandela Corporation. 2019 2018 Sales $187,600 $195,000 Accounts Receivable (net): Beginning of Year 68,100 66,500 End of Year 60,200 68,100 A newly hired manager has started implementing new credit policies. Required: a. As a consultant, you are contracted to analyze Accounts Receivable Turnover and Number of Days’ Sales in Receivable and provide opinion as to whether Mandela’s credit policy changes are working b. What conclusions does your analysis suggest. Are the new credit policies working?arrow_forwardAn examination of Hutton Corporation’s accounting records indicates that all receivables are being recorded in a single account entitled Receivables. An analysis of the account reveals the following: Accounts receivable (trade) $15,500 Accounts receivable (officers)$3600 Interest receivable, due in 3 months$675 Advances to employees$1800 Notes receivable (trade), due in 3 years $9000 Deposit to guarantee contract performance$5000 Utility deposit$500 Total $36,075 Required : How would each of the preceding items normally be reflected (current or noncurrent; trade or nontrade receivable) on Hutton’s balance sheet?arrow_forwardAn examination of Hutton Corporation’s accounting records indicates that all receivables are being recorded in a single account entitled Receivables. An analysis of the account reveals the following: Accounts receivable (trade) $15,500 Accounts receivable (officers)$3600 Interest receivable, due in 3 months$675 Advances to employees$1800 Notes receivable (trade), due in 3 years $9000 Deposit to guarantee contract performance$5000 Utility deposit$500 Total $36,075 Required: 1. Prepare a journal entry to separate the preceding items into their proper accounts.arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax CollegeCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax CollegeCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning