Concept explainers

Videos

The general ledger of Jackrabbit Rentals at January 1, 2018, includes the following account balances:

| Accounts | Debits | Credits |

| Cash | $ 41,500 | |

| 25,700 | ||

| Land | 110,800 | |

| Accounts Payable | $ 15,300 | |

| Notes Payable | 30,000 | |

| Common Stock | 100,000 | |

| 32,700 | ||

| Totals | $178,000 | $178,000 |

The following is a summary of the transactions for the year

a. January 12 Provide services to customers on account, $62,400.

b. February 25 Provide services to customers for cash, $75,300.

c. March 19 Collect on accounts receivable, S45,700.

d. April 30 Issue shares of common stock in exchange for $30,000 cash.

e. June 16 Purchase supplies on account, $12,100.

f. July 7 Pay on accounts payable, $11,300.

g. September 30 Pay salaries for employee work in the current war, $64,200.

h. November 22 Pay advertising for the current year, $22,500.

i. December 30 Pay $2,900 cash dividends to stockholders.

Required:

1. Set up the necessary T-accounts and enter the beginning balances from the

2. Record each of the summary transactions listed above.

3. Post the transactions to the accounts.

4. Prepare an unadjusted trial balance.

5. Record

6. Post adjusting entries.

Requirement – 1

To prepare: The T-accounts and enter the beginning balance from the trial balance.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

The T-accounts of given item in trial balance are as follows:

| Cash | |||

| Jan. 1 | $41,500 | ||

| Bal. | $41,500 | ||

| Land | |||

| Jan. 1 | $110,800 | ||

| Bal. | $110,800 | ||

| Retained earnings | |||

| Jan. 1 | $32,700 | ||

| Bal. | $32,700 | ||

|

Accounts receivables | |||

| Jan. 1 | $25,700 | ||

| Bal. | $25,700 | ||

| Accounts payable | |||

| Jan.1 | $15,300 | ||

| Bal. | $15,300 | ||

| Notes payable | |||

| Jan. 1 | $30,000 | ||

| Bal. | $30,000 | ||

| Common stock | |||

| Jan. 1 | $100,000 | ||

| Bal. | $100,000 | ||

Requirement – 2

To record: The journal entries for given transactions.

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

The journal entries for given transactions of Company J are as follows:

| Date | Account Title and Explanation | Debit($) | Credit($) |

| 2018 | Accounts receivable | 62,400 | |

| January, 12 | Service revenue | 62,400 | |

| (To record the recognized service revenue on account ) | |||

| 2018 | Cash | 75,300 | |

| February, 25 | Service revenue | 75,300 | |

| (To record cash collection from customer) | |||

| 2018 | Cash | 45,700 | |

| March, 19 | Accounts receivables | 45,700 | |

| (To record cash collection on account) | |||

| 2018 | Cash | 30,000 | |

| April, 30 | Common stock | 30,000 | |

| (To record the cash received from issuance of common stock) | |||

| 2018 | Supplies | 12,100 | |

| June, 16 | Accounts payable | 12,100 | |

| (To record the purchase of supplies on account) | |||

| 2018 | Accounts payable | 11,300 | |

| July, 7 | Cash | 11,300 | |

| (To record the payment of cash on account) | |||

| 2018 | Salary expense | 64,200 | |

| September 30 | cash | 10,000 | |

| (To record payment of salaries for work in the current period) | |||

| 2018 | Advertising expense | 22,500 | |

| November 22 | cash | 22,500 | |

| To record payment of advertising) | |||

| 2018 | Dividends | 2,900 | |

| December 30 | Cash | 2,900 | |

| (To record the payment of dividends) | |||

Table (1)

Requirement – 3

To post: The transactions to T-accounts.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

T-accounts of above transactions are as follows:

| Cash | |||

| Jan.1 | $41,500 | July.7 | $11,300 |

| Feb.25 | $75,300 | Sep.30 | $64,200 |

| Mar.19 | $45,700 | Nov.22 | $22,500 |

| Apr.30 | $30,000 | Dec.30 | $2,900 |

| Total | $192,500 | Total | 100,900 |

| Bal. | $91,600 | ||

| Land | |||

| Jan.1 | $110,800 | ||

| Bal. | $110,800 | ||

| Retained earnings | |||

| Jan.1 | $32,700 | ||

| Bal. | $32,700 | ||

|

Salaries expenses | |||

| Jan.1 | $0 | ||

| Bal. | $64,200 | ||

| Accounts receivable | |||

| Jan.1 | $25,700 | ||

| Jan.12 | $62,400 | Mar.19 | $45,700 |

| Accounts payable | |||

| Jan.1 | $15,300 | ||

| Bal. | $11,300 | Jun.16 | $12,100 |

| Notes payable | |||

| Jan. 1 | $30,000 | ||

| Bal. | $30,000 | ||

| Dividends | |||

| Jan.1 | $0 | ||

| Dec.30 | $2,900 | ||

| Advertising expense | |||

| Jan. 1 | $0 | ||

| Nov.22 | $22,500 | ||

| Bal. | $22,500 | ||

| Supplies | |||

| Jan.1 | $0 | ||

| Jun.16 | $12,100 | ||

| Bal. | $12,100 | ||

| Salaries payable | |||

| Jan. 1 | $0 | ||

| Dec.31 | $1,500 | ||

| Common stock | |||

| Jan. 1 | $100,000 | ||

| Apr.30 | $30,000 | ||

| Bal. | $130,000 | ||

| Service revenue | |||

| Jan.1 | $0 | ||

| Jan.12 | $62,400 | ||

| Feb.25 | $75,300 | ||

Requirement – 4

To prepare: The unadjusted trial balance of Company J.

Explanation of Solution

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts before making adjusting journal entries at the end of the period.

| Company J | ||

| Unadjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit Amount($) |

Credit Amount($) |

| Cash | 91,600 | |

| Accounts Receivable | 42,400 | |

| Supplies | 12,100 | |

| Land | 110,800 | |

| Accounts payable | 16,100 | |

| Salaries payable | 0 | |

| Interest payable | 0 | |

| Notes payable | 30,000 | |

| Common stock | 130,000 | |

| Retained earnings | 32,700 | |

| Dividends | 2,900 | |

| Service revenue | 137,700 | |

| Salaries expense | 64,200 | |

| Advertising expense | 22,500 | |

| Interest expense | 0 | |

| Supplies expense | 0 | |

| Totals | $346,500 | $346,500 |

Table (2)

Therefore, the total of debit, and credit columns of unadjusted trial balance is $346,500 and agree.

Requirement – 5

To record: The given adjusting entries of Company J.

Explanation of Solution

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. The purpose of adjusting entries is to adjust the revenue, and the expenses during the period in which they actually occurs.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Adjusting entries of Company P are as follows:

Depreciation expense:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Interest Expense | 2,500 | ||

| Interest payable | 2,500 | |||

| (To record the amount of accrue interest on notes payable) |

Table (3)

Following is the rule of debit and credit of above transaction:

- Interest expense is an expense, and it decreased the value of stockholder’s equity. Therefore, it is debited.

- Interest payable is a liability. There is a increase in the value of liability. Therefore it is credited.

Office supplies expense:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Supplies expense | 9,800 | ||

|

Supplies (1) | 9,800 | |||

| (To record the supplies expense incurred at the end of the accounting year) |

Table (4)

Following is the rule of debit and credit of above transaction:

- Supplies expense is an expense, and it decreased the value of stockholder’s equity. Therefore, it is debited.

- Supplies are an asset account. There is a decrease in assets, therefore it is credited.

Deferred revenue:

| Date | Accounts title and explanation | Post Ref. | Debit ($) | Credit ($) |

| December 31, 2018 | Salaries expense | 1,500 | ||

| Salaries payable | 1,500 | |||

| (To record the salary payable for the current period) |

Table (5)

Following is the rules of debit and credit of above transaction:

- Salaries expense is an expense. There is a decrease in the value of stockholder’s equity. Therefore, it is debited.

- Salaries payable is a liability. There is a increase in the value of liability. Therefore it is credited

Working note:

1. Calculate the supplies used during the year

Requirement – 6

To post: The adjusting entries to appropriate T-accounts.

Explanation of Solution

| Cash | |||

| Jan.1 | $41,500 | July.7 | $11,300 |

| Feb.25 | $75,300 | Sep.30 | $64,200 |

| Mar.19 | $45,700 | Nov.22 | $22,500 |

| Apr.30 | $30,000 | Dec.30 | $2,900 |

| Total | $192,500 | Total | 100,900 |

| Bal. | $91,600 | ||

| Land | |||

| Jan.1 | $110,800 | ||

| Interest payable | |||

| Jan.1 | $0 | ||

| Dec.31 | $2,500 | ||

| Retained earnings | |||

| Jan.1 | $32,700 | ||

| Dec.31 | $100,500 | Dec.31 | $137,700 |

| Dec.31 | $2,900 | ||

| Bal. | $67,000 | ||

| Salaries Expense | |||

| Jan.1 | $0 | ||

| Sep.30 | $64,200 | ||

| Dec.30 | $1,500 | ||

| Bal.65,700 | |||

| Supplies Expense | |||

| Jan.1 | $0 | ||

| Dec.31 | $9,800 | Bal. | $9,800 |

| Total | $0 | ||

| Accounts payable | |||

| Jan.1 | $15,300 | ||

| Bal. | $11,300 | Jun.16 | $12,100 |

| Notes payable | |||

| Jan. 1 | $30,000 | ||

| Bal. | $30,000 | ||

| Dividends | |||

| Jan.1 | $0 | ||

| Dec.30 | $2,900 | ||

| Advertising expense | |||

| Jan. 1 | $0 | ||

| Nov.22 | $22,500 | ||

| Bal. | $22,500 | ||

| Supplies | |||

| Jan.1 | $0 | ||

| Jun.16 | $12,100 | ||

| Bal. | $9,800 | ||

| Common stock | |||

| Jan. 1 | $100,000 | ||

| Apr.30 | $30,000 | ||

| Bal. | $130,000 | ||

|

Service revenue | |||

| Jan.1 | $0 | ||

| Jan.12 | $62,400 | ||

| Feb.25 | $75,300 | ||

| Bal. | $137,700 | ||

| Interest expense | |||

| Jan.1 | $0 | ||

| Dec.30 | $2,500 | ||

Requirement – 7

To prepare: The adjusted trial balance of Company J.

Explanation of Solution

Adjusted trial balance:

Adjusted trial balance is a summary of all the ledger accounts, and it contains the balances of all the accounts after the adjustment entries are journalized, and posted.

Adjusted trial balance of Company J is as follows:

| Company J | ||

| Adjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit Amount($) |

Credit Amount($) |

| Cash | 91,600 | |

| Accounts Receivable | 42,400 | |

| Supplies | 12,100 | |

| Land | 110,800 | |

| Accounts payable | 16,100 | |

| Salaries payable | 1,500 | |

| Interest payable | 2,200 | |

| Notes payable | 30,000 | |

| Common stock | 130,000 | |

| Retained earnings | 32,700 | |

| Dividends | 2,900 | |

| Service revenue | 137,700 | |

| Salaries expense | 64,200 | |

| Advertising expense | 22,500 | |

| Interest expense | 2,500 | |

| Supplies expense | 9,800 | |

| Totals | $350,500 | $350,500 |

Table (6)

Therefore, the total of debit, and credit columns of adjusted trial balance is $350,500 and agree.

Requirement – 8

To prepare: An income statement for 2018 and classified balance sheet as on December 31, 2018.

Explanation of Solution

Income statement:

This is the financial statement of a company which shows all the revenues earned and expenses incurred by the company over a period of time.

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

Income statement:

Income statement of Company J is as follows:

| Company J | ||

| Income statement | ||

| For the year ended December 31, 2018 | ||

| $ | $ | |

| Service revenue (A) | 137,700 | |

| Expenses: | ||

| Salaries expense | 65,700 | |

| Utilities expense | 22,500 | |

| Depreciation expense | 2,500 | |

| Supplies expense | 9,800 | |

| Total expense (B) | 100,500 | |

| Net income

| 37,200 | |

Table (7)

Therefore, the net income of Company J is $37,200.

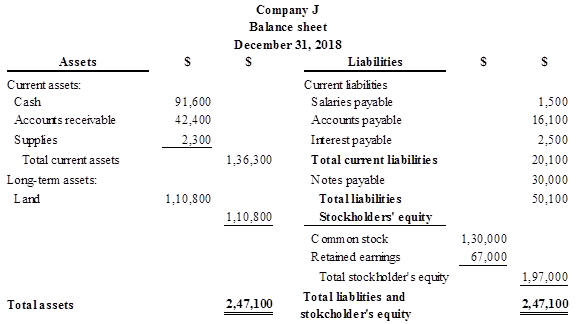

Classified balance sheet:

Classified balance sheet of Company J is as follows:

Figure (1)

Therefore, the total assets of Company P are $247,100, and the total liabilities and stockholders’ equity are $247,100.

Working note:

Calculation of ending balance retained earnings

Requirement – 9

To record: The necessary closing entries of Company J.

Explanation of Solution

Closing entries:

Closing entries are those journal entries, which are passed to transfer the final balances of temporary accounts, (all revenues account, all expenses account and dividend) to the retained earnings. Closing entries produce a zero balance in each temporary account.

Closing entries of Company J is as follows:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| 2018 | Service revenue | 137,700 | ||

| December 31 | Retained earnings | 137,700 | ||

| (To close all revenue account) | ||||

| 2018 | Retained earnings | 100,500 | ||

| December 31 | Salaries expense | 65,700 | ||

| Advertising expense | 22,500 | |||

| Interest expense | 2,500 | |||

| Supplies expense | 9,800 | |||

| (To close all the expenses account) | ||||

| 2018 | Retained earnings | 2,900 | ||

| December 31 | Dividends | 2,900 | ||

| (To close the dividends account) | ||||

Table (8)

Requirement – 10

To post: The closing entries to the T-accounts.

Explanation of Solution

| Cash | |||

| Jan.1 | $41,500 | July.7 | $11,300 |

| Feb.25 | $75,300 | Sep.30 | $64,200 |

| Mar.19 | $45,700 | Nov.22 | $22,500 |

| Apr.30 | $30,000 | Dec.30 | $2,900 |

| Total | $192,500 | Total | 100,900 |

| Bal. | $91,600 | ||

| Land | |||

| Jan.1 | $110,800 | ||

| Bal. | $110,800 | ||

| Interest payable | |||

| Jan.1 | $0 | ||

| Dec.31 | $2,500 | ||

| Retained earnings | |||

| Jan.1 | $32,700 | ||

| Bal. | $32,700 | ||

| Salaries Expense | |||

| Jan.1 | $0 | ||

| Sep.30 | $64,200 | ||

| Dec.30 | $1,500 | ||

| Bal. | $65,700 | ||

| Supplies Expense | |||

| Jan.1 | $0 | ||

| Dec.31 | $9,800 | ||

| Accounts receivable | |||

| Jan.1 | $25,700 | ||

| Jan.12 | $62,400 | Mar.19 | $45,700 |

| Accounts payable | |||

| Jan.1 | $15,300 | ||

| Bal. | $11,300 | Jun.16 | $12,100 |

| Total |

$16,100 | ||

|

Notes payable | |||

| Jan. 1 | $30,000 | ||

| Bal. | $30,000 | ||

| Dividends | |||

| Jan.1 | $0 | ||

| Dec.30 | $2,900 | Bal. | $2,900 |

| Advertising expense | |||

| Jan. 1 | $0 | ||

| Nov.22 | $22,500 | Bal. | $22,500 |

| Total | $0 | ||

| Supplies | |||

| Jan.1 | $0 | ||

| Jun.16 | $12,100 | ||

| Bal. | $9,800 | ||

| Total | $2,300 | ||

| Salaries payable | |||

| Jan. 1 | $0 | ||

| Dec.31 | $1,500 | ||

| Common stock | |||

| Jan. 1 | $100,000 | ||

| Apr.30 | $30,000 | ||

| Total | $130,000 | ||

|

Service revenue | |||

| Jan.1 | $0 | ||

| Jan.12 | $62,400 | ||

| Bal. | 137,700 | Feb.25 | $75,300 |

| Total. | $0 | ||

| Interest expense | |||

| Jan.1 | $0 | ||

| Dec.30 | $2,500 | Bal | $2,500 |

| Total | $0 | ||

Requirement – 11

To prepare: A post-closing trial balance of Company J.

Explanation of Solution

Post-closing trial balance:

The post-closing trial balance is a summary of all ledger accounts, and it shows the debit and the credit balances after the closing entries are journalized and posted. The post-closing trial balance contains only permanent (balance sheet) accounts, and the debit and the credit balances of permanent accounts should agree.

Post-closing trial balance of Company J is as follows:

| Company J | ||

| Adjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit Amount($) | Credit Amount($) |

| Cash | 91,600 | |

| Accounts Receivable | 42,400 | |

| Supplies | 2,300 | |

| Land | 110,800 | |

| Account payable | 16,000 | |

| Salaries payable | 1,500 | |

| Interest payable | 2,500 | |

| Notes payable | 30,000 | |

| Common stock | 130,000 | |

| Retained earnings | 67,000 | |

| Total | $247,100 | $247,100 |

Table (9)

Therefore, the total of debit, and credit columns of post-closing trial balance is $247,100 and agree.

Want to see more full solutions like this?

Chapter 3 Solutions

FINANCIAL ACCOUNTINGLL W/CONNECT >IC<

- Maddie Inc. has the following transactions for its first month of business. A. What are the individual account balances, and the total balance, in the accounts receivable subsidiary ledger? B. What is the balance in the accounts receivable general ledger (control) account?arrow_forwardCatherines Cookies has a beginning balance in the Accounts Payable control total account of $8,200. In the cash disbursements journal, the Accounts Payable column has total debits of $6,800 for November. The Accounts Payable credit column in the purchases journal reveals a total of $10,500 for the current month. Based on this information, what is the ending balance in the Accounts Payable account in the general ledger?arrow_forwardCatherines Cookies has a beginning balance in the Accounts Receivable control total account of $8,200. $15,700 was credited to Accounts Receivable during the month. In the sales journal, the Accounts Receivable debit column shows a total of $12,000. What is the ending balance of the Accounts Receivable account in the general ledger?arrow_forward

- When examining the accounts of Palma Company, you ascertain that balance relating to bothreceivables and payables are included in a single controlling account (called receivables),which has a P23,050 debit balance. An analysis of the details of this account revealed thefollowing: Items Debit Credit Accounts Receivable - customers P 40,000 Accounts receivable - officers (Current collection expected) 2,500 Debit balances - creditors 450 Expense advances to salespersons 1,000 Share capital subscriptions receivable 4,600 Accounts payable for merchandise P 19,250 Unpaid salaries 3,300 Credit balance in customer accounts 2,000 Cash received in advance from customers for goods not yet shipped 450 Expected bad debts, cumulative 500 Required:1. How should each item be reported on Palma Company’s statement of financial position?arrow_forwardWhen examining the accounts of Palma Company, you ascertain that balance relating to bothreceivables and payables are included in a single controlling account (called receivables),which has a P23,050 debit balance. An analysis of the details of this account revealed thefollowing: Items Debit Credit Accounts Receivable - customers P 40,000 Accounts receivable - officers (Current collection expected) 2,500 Debit balances - creditors 450 Expense advances to salespersons 1,000 Share capital subscriptions receivable 4,600 Accounts payable for merchandise P 19,250 Unpaid salaries 3,300 Credit balance in customer accounts 2,000 Cash received in advance from customers for goods not yet shipped 450 Expected bad debts, cumulative 500 Required:1. Give the journal entry to eliminate the above account and to set up the appropriateaccounts to replace it.arrow_forwardThe following data are taken from the financial statements of Colby Company. Accounts receivable (net), end of year Net sales on account Terms for all sales are 1/10, n/45 Accounts Receivable turnover Average collection period (b) B I U T₂ T² Ix 2022 $550,000 4,300,000 2022 7.9 times lil 2021 What conclusions about the management of accounts receivable can be drawn from the accounts receivable turnover and the average collections period. € $540,000 4,000,000 2021 46.2 days 48.7 days 7.5 times W 144 144 들 3 99 = á T ¶₁arrow_forward

- Guardian Carpets Incorporated provided the following accounts related to beginning balances in its accounts receivable and allowance accounts for the current year: Accounts Receivable Beginning Balance 6,000,000 Allowance for Uncollectible Accounts 2,000,000 Beginning Balance Question content area top right Part 1 Requirement Prepare the journal entries to record the following transactions that occurred during the current year. Prepare a schedule for both accounts receivable and the allowance for uncollectible accounts that shows the beginning balances, the various items that change the beginning balance, and the ending balance. Question content area bottom Part 1 Prepare the journal entries to record the following transactions that occurred during the current year. (Record debits first, then credits. Exclude explanations from any journal…arrow_forwardThe following is select financial statement information from Candid Photography: Year Net Credit Sales Ending Accounts Receivable 2017 $2,988,000 $1,290,450 2018 $3,750,860 $1,345,600 2019 $4,000,350 $1,546,550 Compute the accounts receivable turnover ratios and the number of days’ sales in receivables ratios for 2018 and 2019 (round answers to two decimal places): 2018 Accounts Receivable Turnover _______ times. A. 2.85 B. 2.91 C. 1.42 D. 2.79 2018 Days' Sales in Receivables ________days. A. 128.07 B. 125.43 C. 257.04 D. 130.82 2019 Accounts Receivable Turnover _________times. A. 2.97 B. 2.77 C. 1.38 D. 2.59 2019 Days' Sales in Receivables _______days. A. 131.77 B. 122.90 C. 140.93 D. 264.49 What do the outcomes tell a potential investor about Candid Photography if industry average for accounts receivable turnover ratio is 3…arrow_forward(c) What is the balance of accounts receivable on it December 31 balance sheet? Estimating Uncollectible Accounts and Reporting Accounts ReceivableLaFond Company analyzes its accounts receivable at December 31, and arrives at the age categories below along with the percentages that are estimated as uncollectible. Age Group Accounts Receivable Estimated Loss % 0-30 days past due $ 180,000 1% 31-60 days past due 40,000 2 61-120 days past due 22,000 5 121-180 12,000 10 Over 180 days past due 8,000 25 Total accounts receivable $ 262,000arrow_forward

- The details of the accounts receivable of AA Corporation as December 31, 2022 shows the following: Beginning balance P3,450,000 Sales on account made to customers 2,800,000 Collection of accounts receivable during the year 4,200,000 Accounts written off as uncollectible 90,000 The following transactions were included in the recorded transactions during the year: 1. Invoice dated December 28, 2022 for P350,000 was shipped and received by the buyer on December 31, 2022, this invoice was recorded in the book at P35,000. 2. Invoice dated and recorded on November 30, 2022 was erroneously priced at P32 per unit. There were 11,000 units of goods delivered which were received on December 10, 2022. The agreed price should be at P22 per unit only. AA's policy is to provide 5% of the outstanding balance of accounts receivable as uncollectible and there is beginning balance of allowance for bad debts of P40,000. Statement 1: The amount of bad debt expense in 2022 is P158,250. Statement 2: The…arrow_forwardEnter the balances at July 1 in the receivable accounts and post the entries to all of the receivable accounts. (Post entries in the order of journal entries presented in the previous part.) 7/1 Bal. 7/5 7/31 7/1 Bal 7/31 Bal. Notes Receivable 22,000 4140 400 Accounts Receivable 400 Interest Receivable 728 80 648arrow_forwardFinancial statement data for the years ended December 31 for Parker Corporation are as follows: Sales Accounts receivable: Beginning of year End of year Current Year Current Year $2,595,600 Current Year 390,000 434,000 a. Determine the accounts receivable turnover for each year. Round your answers to one decimal place. Accounts Receivable Turnover times times Prior Year $2,409,500 400,000 390,000 Prior Year b. Determine the days' sales in receivables for each year. Round your answers to nearest day. Assume 365 days per year. Number of Days' Sales in Receivables days days Prior Year c. Does the change in accounts receivable turnover and days' sales in receivables from the first year to the second year indicate a favorable or unfavorable change?arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax CollegeCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax CollegeCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,