Videos

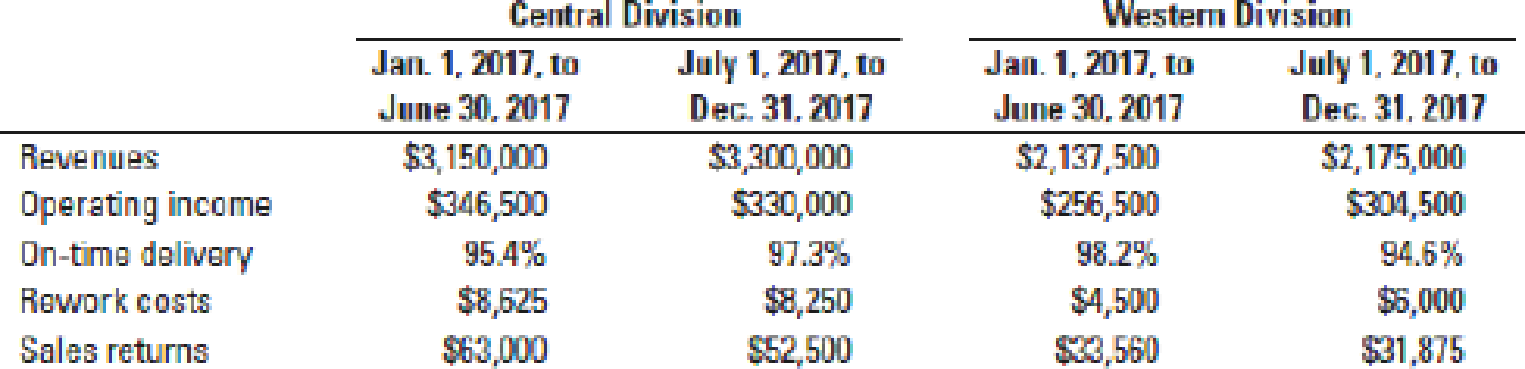

Financial and nonfinancial performance measures, goal congruence. (CMA, adapted) Precision Equipment specializes in the manufacture of medical equipment, a field that has become increasingly competitive. Approximately 2 years ago, Pedro Mendez, president of Precision, decided to revise the bonus plan (based, at the time, entirely on operating income) to encourage division managers to focus on areas that were important to customers and that added value without increasing cost. In addition to a profitability incentive, the revised plan includes incentives for reduced rework costs, reduced sales returns, and on-time deliveries. The company calculates and rewards bonuses semiannually on the following basis: A base bonus is calculated at 2% of operating income; this amount is then adjusted as follows:

- i. Reduced by excess of rework costs over and above 2% of operating income

- ii. No adjustment if rework costs are less than or equal to 2% of operating income

- i. Increased by $4,000 if more than 98% of deliveries are on time and by $1,500 if 96–98% of deliveries are on time

- ii. No adjustment if on-time deliveries are below 96%

- i. Increased by $2,500 if sales returns are less than or equal to 1.5% of sales

- ii. Decreased by 50% of excess of sales returns over 1.5% of sales

If the calculation of the bonus results in a negative amount for a particular period, the manager simply receives no bonus, and the negative amount is not carried forward to the next period.

Results for Precision’s Central division and Western division for 2017, the first year under the new bonus plan, follow. In 2016, under the old bonus plan, the Central division manager earned a bonus of $20,295 and the Western division manager received a bonus of $15,830.

- 1. Why did Mendez need to introduce these new performance measures? That is, why does Mendez need to use these performance measures in addition to the operating-income numbers for the period?

- 2. Calculate the bonus earned by each manager for each 6-month period and for 2017 overall.

- 3. What effect did the change in the bonus plan have on each manager’s behavior? Did the new bonus plan achieve what Mendez wanted? What changes, if any, would you make to the new bonus plan?

Want to see the full answer?

Check out a sample textbook solution

Chapter 23 Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- At the end of 20x1, Mejorar Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To lower costs, Mejorar undertook a number of improvement activities such as JIT production, total quality management, and activity-based management. Now, after two years of operation, the president of Mejorar wants some assessment of the achievements. To help provide this assessment, the following information on one product has been gathered: Required: 1. Compute the following measures for 20x1 and 20x3: a. Actual velocity and cycle time b. Percentage of total revenue from new customers (assume one unit per customer) c. Percentage of very satisfied customers (assume each customer purchases one unit) d. Market share e. Percentage change in actual product cost (for 20x3 only) f. Percentage change in days of inventory (for 20x3 only) g. Defective units as a percentage of total units produced h. Total hours of training i. Suggestions per production worker j. Total revenue k. Number of new customers 2. For the measures listed in Requirement 1, list likely strategic objectives, classified according to the four Balance Scorecard perspectives. Assume there is one measure per objective.arrow_forwardSuspicious Acquisition of Data, Ethical Issues Bill Lewis, manager of the Thomas Electronics Division, called a meeting with his controller, Brindon Peterson, and his marketing manager, Patty Fritz. The following is a transcript of the conversation that took place during the meeting: Bill: Brindon, the variable costing system that you developed has proved to be a big plus for our division. Our success in winning bids has increased, and as a result our revenues have increased by 25%. However, if we intend to meet this years profit targets, we are going to need something extraam I right, Patty? Patty: Absolutely. While we have been able to win more bids, we still are losing too many, particularly to our major competitor, Kilborn Electronics. If we knew more about their bidding strategy, we could be more successful at competing with them. Brindon: Would knowing their variable costs help? Patty: Certainly. It would give me their minimum price. With that knowledge, Im sure that we could find a way to beat them on several jobs, particularly on those jobs where we are at least as efficient. It would also help us to identify where we are not cost competitive. With this information, we might be able to find ways to increase our efficiency. Brindon: Well, I have good news. Ive been talking with Carl Penobscot, Kilborns assistant controller. Carl doesnt feel appreciated by Kilborn and wants to make a change. He could easily fit into our team here. Plus, Carl has been preparing for a job switch by quietly copying Kilborns accounting files and records. Hes already given me some data that reveal bids that Kilborn made on several jobs. If we can come to a satisfactory agreement with Carl, hell bring the rest of the information with him. Well easily be able to figure out Kilborns prospective bids and find ways to beat them. Besides, I could use another accountant on my staff. Bill, would you authorize my immediate hiring of Carl with a favorable compensation package? Bill: I know that you need more staff, Brindon, but is this the right thing to do? It sounds like Carl is stealing those files, and surely Kilborn considers this information confidential. I have real ethical and legal concerns about this. Why dont we meet with Laurie, our attorney, and determine any legal problems? Required: 1. Is Carls behavior ethical? What would Kilborn think? 2. Is Bill correct in supposing that there are ethical and/or legal problems involved with the hiring of Carl? (Reread the section on corporate codes of conduct in Chapter 1.) What would you do if you were Bill? Explain.arrow_forwardInternal and External Linkages, Strategic Cost Management Maxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintain—and perhaps increase—its market share, Maxwell’s management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems. Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage;…arrow_forward

- JIT production, relevant benets, relevant costs, ethics. Galveston Pump Corporation is considering implementing a JIT production system. The new system would reduce current average inventory levels of $2,000,000 by 75%, but it would require a much greater dependency on the company’s core suppliers for on-time deliveries and high-quality inputs. The company’s operations manager, Frank Griswold, is opposed to the idea of a new JIT system because he is concerned that the new system (a) will be too costly to manage; (b) will result in too many stockouts; and (c) will lead to the layoff of his employees, several of whom are currently managing inventory. He believes that these layoffs will affect the morale of his entire production department. The management accountant, Bonnie Barrett, is in favor of the new system because of its likely cost savings. Frank wants Bonnie to rework the numbers because he is concerned that top management will give more weight to nancial factors and not give due…arrow_forwardHarry Haney, manager of the Eastern Division of MertockCo., made the following comment to the manager of theCentral Division: It’s all well and good for you to say that I should dis-regard sunk costs when I consider whether to replace the old, inefficient equipment with new, more efficientequipment. But my performance evaluation is based onnet operating profits divided by total assets. The newequipment will increase my total asset base and lowerthe ratio of profits to assets, hurting my performance.Thus, I will not sell the old equipment.Do you agree with Haney’s statement? Why or why not?arrow_forwardBalanced scorecard, social performance. Comtex Company provides cable and Internet services in the greater Boston area. There are many competitors that provide similar services. Comtex believes that the key to nancial success is to offer a quality service at the lowest cost. Comtex currently spends a signicant amount of hours on installation and postinstallation support. This is one area that the company has targeted for cost reduction. Comtex’s balanced scorecard for 2017 follows.arrow_forward

- Balanced scorecard, social performance. Comtex Company provides cable and Internet services in the greater Boston area. There are many competitors that provide similar services. Comtex believes that the key to financial success is to offer a quality service at the lowest cost. Comtex currently spends a significant amount of hours on installation and post-installation support. This is one area that the company has targeted for cost reduction. Comtex’s balanced scorecard for 2017 follows.arrow_forwardChoice of Strategic Business UnitRequired For each of the following cases, determine whether the business unit should be evaluated asa cost center or a profit center and explain why. If you choose cost center, then explain which type of costcenter—the discretionary-cost center or the engineered-cost center.1. A trucking firm has experienced a rapid increase in fuel costs and has only been partly successful inpassing along the increased costs to customers. In recent months, fuel prices have come back down, butthe firm’s management knows to expect a continued volatility in the cost of fuel. To secure the firm’sprofits when fuel costs are rising, the company has established an Office of Sustainability to developand implement a strategy for reducing costs and reducing the firm’s overall carbon footprint.2. To more effectively compete in a dynamic market for consumer electronics, a manufacturer of consumer electronics products has established a new department for Innovation and Refinement…arrow_forwardStrategy, balanced scorecard, service company. Compton Associates is an architectural firm that has been in practice only a few years. Because it is a relatively new firm, the market for the firm’s services is very competitive. To compete successfully, Compton must deliver quality services at a low cost. Compton presents the following data for 2016 and 2017. Architect labor-hour costs are variable costs. Architect support costs for each year depend on the Architect support capacity that Compton chooses to maintain each year (that is, the number of jobs it can do each year). Architect support costs do not vary with the actual number of jobs done that year. 1. Is Compton Associate’s strategy one of product differentiation or cost leadership? Explain briefly. 2. Describe key measures you would include in Compton’s balanced scorecard and your reasons for doing so.arrow_forward

- The Southern Division manager of Texcaliber Inc. is growing concerned that the division will not be able to meet its current period income objectives. The division uses absorption costing for internal profit reporting and had an appropriate level of inventory at the beginning of the period. The division manager knows that he can boost profits by increasing production at the end of the period. The increased production will allocate fixed costs over a greater number of units, reducing cost of goods sold and increasing earnings. Unfortunately, it is unlikely that additional production will be sold, resulting in a large ending inventory balance. The division manager has come to Aston Melon, the divisional controller, to determine exactly how much additional production is needed to increase net income enough to meet the division's profit objectives. Aston analyzes the data and determines that the division will need to increase inventory by 30% in order to absorb enough fixed costs to meet…arrow_forwardBalanced scorecard, social performance. Comtex Company provides cable and Internet services in the greater Boston area. There are many competitors that provide similar services. Comtex believes that the key to financial success is to offer a quality service at the lowest cost. Comtex currently spends a significant amount of hours on installation and post-installation support. This is one area that the company has targeted for cost reduction. Comtex’s balanced scorecard for 2017 follows in the attatched: Q.Is there a cause-and-effect linkage between the measures in the internal-business-process perspective and the customer perspective? That is, would you add other measures to the internal-business-process perspective or the customer perspective? Why or why not? Explain briefly.arrow_forwardBalanced scorecard, social performance. Comtex Company provides cable and Internet services in the greater Boston area. There are many competitors that provide similar services. Comtex believes that the key to financial success is to offer a quality service at the lowest cost. Comtex currently spends a significant amount of hours on installation and post-installation support. This is one area that the company has targeted for cost reduction. Comtex’s balanced scorecard for 2017 follows in the attatched: Q. Why do you think Comtex included balanced scorecard measures relating to employee safety and community engagement? How well is the company doing on these measures?arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning