FUND.ACCT.PRIN.

25th Edition

ISBN: 9781260247985

Author: Wild

Publisher: RENT MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 19, Problem 13E

Exercise 19-13

Adjusting factory

Refer to information in Exercise 19-7. Prepare the

Exercise 19-7

Cost flows in a

P1 P2 P3 P4

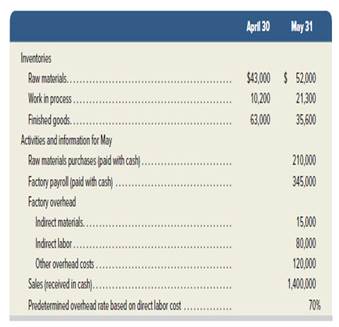

The following information is available for Lock-Tite Company, which produces special- order security products and uses a job order costing system.

Compute the following amounts for the month of May.

1. Cost of direct materials used.

2. Cost of direct labor used.

3. Cost of goods manufactured.

4. Cost of goods sold.*

5. Gross profit.

6. Overapplied or underapplied overhead.

*Do not consider any underapplied or overapplied overhead. Check (3) $625,400

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Exercise 5.19Journal Entries, T-AccountsObjective 4 - Describe the cost flows associated with job-order costing, andprepare the joumal entries.Kapoor Company uses job-order costing. During January, the following datawere reported:a. Materials purchased on account: direct materials, $98,500; indirectmaterials, S14,800.b. Materials issued: direct materials, S82,500; indirect materials, S8,800.c. Labor cost incurred: direct labor, $67,000; indirect labor, $18,750.d. Other manufacturing costs incurred ( all payables), S46,200.e, Overhead is applied on the basis of 110 percent of direct labor cost.f. Wark finished and transferred to Finished Goods Inventory cost$230,000.g. Finished goods costing S215,000 were sold on account for 140 percentof cost.h. Any over- or underapplied overhead is closed to Cost of Goods Sold.Required:1, Prepare journal entries to record these transactions.2. Prepare a T-account for Overhead Control. Post all relevant information to thisaccount. What is the ending…

Problem 22: Cost of Goods Sold Statement

Julius Inc. is employing normal costing for its job orders. The overhead is applied using a predetermined overhead rate. The following information relates to the Julius Inc. for the year ended December 31, 2020:

Job No. 101 Job No. 102 Job No. 103

Job in Process, January 1, 2020:

Direct Materials 40,000 30,000 0

Labor 60,000 40,000 0

Factory Overhead 30,000 20,000 0

Costs added during 2020

Materials 20,000 10,000 100,000

Labor 100,000…

PART III—DETERMINE WORK IN PROCESS AND FINISHED GOODS BALANCES

Hanover Manufacturing begins operations on April 1. Information from job cost sheets shows the following:

Manufacturing Costs Assigned (non-cumulative)

Job April May June

15$10,200

16 5,100$6,400

18 3,6005,900$4,000

197,3007,400

203,100

Job 15 was completed in April. Job 16 was completed in May. Job 18 was completed in June. Each job was sold in the month following completion.

Instructions: Determine the following amounts:

1.Work in process inventory, April 30$_______________

2.Finished goods inventory, April 30$_______________

3.Work in process inventory, May 31$_______________

4.Finished goods inventory, May 31$_______________

5.Work in process inventory, June 30$_______________

6.Finished goods inventory, June 30$_______________

Chapter 19 Solutions

FUND.ACCT.PRIN.

Ch. 19 - Jobs and job lots C1 Determine which of the...Ch. 19 - Job cost sheets C2 Clemens Cars's job cost sheet...Ch. 19 - Documents in job order costing P1 P2 P3 The left...Ch. 19 - Raw materials journal entries P1 During the...Ch. 19 - Prob. 5QSCh. 19 - Prob. 6QSCh. 19 - Prob. 7QSCh. 19 - Prob. 8QSCh. 19 - Prob. 9QSCh. 19 - Prob. 10QS

Ch. 19 - Prob. 11QSCh. 19 - Prob. 12QSCh. 19 - Jab order costing of services A1 An advertising...Ch. 19 - Job order costing of services A1 An advertising...Ch. 19 - Job cost sheet C2 Eco Skate makes skateboards from...Ch. 19 - Prob. 16QSCh. 19 - Prob. 17QSCh. 19 - Prob. 18QSCh. 19 - Prob. 19QSCh. 19 - Prob. 20QSCh. 19 - Prob. 21QSCh. 19 - Prob. 22QSCh. 19 - Prob. 23QSCh. 19 - Prob. 24QSCh. 19 - Exercise 19-1 Job order production C1 Match each...Ch. 19 - Exercise 19-2 Job cost computation C2 The...Ch. 19 - Exercise 19-3 Analysis of cost flows C2 As of the...Ch. 19 - Exercise 19-4 Recording product costs P1 P2 P3...Ch. 19 - Exercise 19-5 Manufacturing cost flows P1 P2 P3...Ch. 19 - Exercise 19-6 Recording events in job order...Ch. 19 - Exercise 19-7 Cost flows in a jab order costing...Ch. 19 - Exercise 19-8 Journal entries for materials P1 Use...Ch. 19 - Exercise 19-9 Journal entries for labor P2 Use...Ch. 19 - Exercise 19-10 Journal entries for overhead P3 Use...Ch. 19 - Exercise 19-11 Overhead rate; costs assigned to...Ch. 19 - Exercise 19-12 Analyzing costs assigned to work in...Ch. 19 - Exercise 19-13 Adjusting factory overhead P4 Refer...Ch. 19 - Exercise 19-14 Adjusting factory overhead P4...Ch. 19 - Prob. 15ECh. 19 - Prob. 16ECh. 19 - Exercise 19-17 Overhead rate calculation,...Ch. 19 - Exercise 19-18 Job order costing for services A1...Ch. 19 - Exercise 19-19 Job order costing of services A1...Ch. 19 - Exercise 19-20 Direct materials journal entries P1...Ch. 19 - Prob. 21ECh. 19 - Prob. 22ECh. 19 - Prob. 23ECh. 19 - Prob. 24ECh. 19 - Prob. 25ECh. 19 - Prob. 26ECh. 19 - Prob. 27ECh. 19 - Prob. 28ECh. 19 - Prob. 29ECh. 19 - Prob. 30ECh. 19 - Prob. 31ECh. 19 - Problem 19-1A Production costs computed and...Ch. 19 - Problem 19-2 A Source documents, journal entries,...Ch. 19 - Prob. 3PSACh. 19 - Prob. 4PSACh. 19 - Problem 19-5A Production transactions, subsidiary...Ch. 19 - Problem 19-1B Production costs computed and...Ch. 19 - Prob. 2PSBCh. 19 - Prob. 3PSBCh. 19 - Problem 19-4B Overhead allocation and adjustment...Ch. 19 - Problem 19-5B Production transactions, subsidiary...Ch. 19 - The computer workstation furniture manufacturing...Ch. 19 - The General Ledger tool in Connect automates...Ch. 19 - Manufacturers and merchandisers can apply...Ch. 19 - Prob. 2AACh. 19 - Apple and Samsung compete in the global...Ch. 19 - Prob. 1DQCh. 19 - Some companies use labor cost to apply factory...Ch. 19 - Prob. 3DQCh. 19 - In a job order costing system, what records serve...Ch. 19 - What journal entry is recorded when a materials...Ch. 19 - Prob. 6DQCh. 19 - Google uses a "time ticket" for some employees....Ch. 19 - What events cause debits to be recorded in the...Ch. 19 - Prob. 9DQCh. 19 - Assume that Apple produces a batch of 1,000...Ch. 19 - 11. Why must a company use predetermined overhead...Ch. 19 - How would a hospital apply job order costing?...Ch. 19 - Harley-Davidson manufactures 30 custom-made,...Ch. 19 - Prob. 14DQCh. 19 - Prob. 15DQCh. 19 - Assume that your company sells portable housing to...Ch. 19 - Assume that you are preparing for a second...Ch. 19 - Prob. 3BTNCh. 19 - Consider the activities undertaken by a medical...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- JOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M. Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or over applied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102,103, and 104, direct labor hours are 12, 000, 10,000, 11, 000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour. (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101104 using the predetermined factory overhead rate (see above). (i) Finished Job Nos. 101103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and for 50,000 and 45,400, respectively. (k) Transferred under- or over applied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). 2. Post the entries to the work in process and finished goods accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardJOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or overapplied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102, 103, and 104, direct labor hours are 12,000, 10,000, 11,000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101-104 using the predetermined factory overhead rare (see above). (i) Finished Job Nos. 101-103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and O for 50,000 and 45,400, respectively. (k) Transferred under- or overapplied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). Make compound entries for (b), (d), and (h), with separate debits for each job. 2. Post the entries to the work in process and finished goods T accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardKingsford Furnishings Company manufactures designer furniture. Kingsford Furnishings uses a job order cost system. Balances on April 1 from the materials ledger are as follows: The materials purchased during April are summarized from the receiving reports as follows: Materials were requisitioned to individual jobs as follows: The glue is not a significant cost, so it is treated as indirect materials (factory overhead). a. Journalize the entry to record the purchase of materials in April. b. Journalize the entry to record the requisition of materials in April. c. Determine the April 30 balances that would be shown in the materials ledger accounts.arrow_forward

- JOURNAL ENTRIES FOR MATERIAL, LABOR, OVERHEAD, AND SALES Alert Enterprises had the following job order transactions during the month of April. Record the transactions in the general journal, including issuance of materials, labor, and factory overhead applied; completed jobs sent to finished goods inventory; closing of the under or over applied factory overhead to the cost of goods sold account; and sale of finished goods.arrow_forwardSchumacher Industries Inc. manufactures recreational vehicles. Schumacher Industries uses a job order cost system. The time tickets from June jobs are summarized as follows: Factory overhead is applied to jobs on the basis of a predetermined overhead rate of 23 per direct labor hour. The direct labor rate is 29 per hour. a. Journalize the entry to record the factory labor costs. b. Journalize the entry to apply factory overhead to production for June.arrow_forwardSummary information from a companys job cost sheets shows the following information: What are the balances in the work in process inventory, finished goods Inventory, and cost of goods sold for April, May, and June?arrow_forward

- JOURNAL ENTRIES FOR MATERIAL, LABOR, OVERHEAD, AND SALES Micro Enterprises had the following job order transactions during the month of April. Record the transactions in the general journal, including issuance of materials, labor, and factory overhead applied; completed jobs sent to finished goods inventory; closing of the under- or overapplied factory overhead to the cost of goods sold account; and sale of finished goods. Apr.1 Purchased materials on account, 35,000. 10 Issued direct materials to Job No. 33, 10,000. 11 Issued direct materials to Job No. 34, 8,000. 12 Issued direct materials to Job No. 35, 11,000. 25 Incurred direct labor: On Job No. 33, 6,000 On Job No. 34, 4,000 On Job No. 35, 5,000 25 Applied factory overhead: To Job No. 33, 1,500 To Job No. 34, 1,200 To Job No. 35, 1,600 30 Transferred Job Nos. 3335 to the finished goods inventory account as products F, G, and H, respectively. 30 Sold products F, G, and H for 20,000, 16,000, and 22,000, respectively. 30 Actual factory overhead for Job Nos. 3335, 4,220.arrow_forward(Appendix 3A) Method of Least Squares Using Computer Spreadsheet Program The controller for Beckham Company believes that the number of direct labor hours is associated with overhead cost. He collected the following data on the number of direct labor hours and associated factory overhead cost for the months of January through August. Required: 1. Using a computer spreadsheet program such as Excel, run a regression on these data. Print out your results. 2. Using your results from Requirement 1, write the cost formula for overhead cost. (Note: Round the fixed cost to the nearest dollar and the variable rate to the nearest cent.) 3. CONCEPTUAL CONNECTION What is R2 based on your results? Do you think that the number of direct labor hours is a good predictor of factory overhead cost? 4. Assuming that expected September direct labor hours are 700, what is expected factory overhead cost using the cost formula in Requirement 2?arrow_forward(Appendix 4A) Unit Cost, Ending Work in Process, Journal Entries During August, Leming Inc. worked on two jobs. Data relating to these two jobs follow: Overhead is assigned on the basis of direct labor hours at a rate of 11. During August, Job 64 was completed and transferred to Finished Goods. Job 65 was the only unfinished job at the end of the month. Required: 1. Calculate the per-unit cost of Job 64. 2. Compute the ending balance in the work-in-process account. 3. Prepare the journal entries reflecting the completion and sale on account of Job 64. The selling price is 175% of cost. (Note: Round all journal entry amounts to the nearest dollar.)arrow_forward

- A new company started production. Job 10 was completed, and Job 20 remains in production. Here is the information from job cost sheets from their first and only jobs so far: Using the information provided. A. What is the balance in work in process? B. What Is the balance in the finished goods inventory? C. If manufacturing overhead is applied on the basis of direct labor hours, what is the predetermined overhead rate?arrow_forwardPREDETERMINED FACTORY OVERHEAD RATE Marston Enterprises calculates a predetermined factory overhead rate so that factory overhead may be applied to production during the month. It calculates the overhead using three different methods and then decides which one to use. Total estimated factory overhead costs are 600,000. Total estimated direct labor hours are 30,000. Total estimated direct labor costs are 1,200,000. Total machine hours are estimated to be 200,000. Calculate the predetermined overhead application rates based on (1) direct labor hours, (2) direct labor costs, and (3) machine hours.arrow_forwardOverhead Assignment: Actual and Normal Activity Compared Reynolds Printing Company specializes in wedding announcements. Reynolds uses an actual job-order costing system. An actual overhead rate is calculated at the end of each month using actual direct labor hours and overhead for the month. Once the actual cost of a job is determined, the customer is billed at actual cost plus 50%. During April, Mrs. Lucky, a good friend of owner Jane Reynolds, ordered three sets of wedding announcements to be delivered May 10, June 10, and July 10, respectively. Reynolds scheduled production for each order on May 7, June 7, and July 7, respectively. The orders were assigned job numbers 115, 116, and 117, respectively. Reynolds assured Mrs. Lucky that she would attend each of her daughters weddings. Out of sympathy and friendship, she also offered a lower price. Instead of cost plus 50%, she gave her a special price of cost plus 25%. Additionally, she agreed to wait until the final wedding to bill for the three jobs. On August 15, Reynolds asked her accountant to bring her the completed job-order cost sheets for Jobs 115, 116, and 117. She also gave instructions to lower the price as had been agreed upon. The cost sheets revealed the following information: Reynolds could not understand why the overhead costs assigned to Jobs 116 and 117 were so much higher than those for Job 115. She asked for an overhead cost summary sheet for the months of May, June, and July, which showed that actual overhead costs were 20,000 each month. She also discovered that direct labor hours worked on all jobs were 500 hours in May and 250 hours each in June and July. Required: 1. How do you think Mrs. Lucky will feel when she receives the bill for the three sets of wedding announcements? 2. Explain how the overhead costs were assigned to each job. 3. Assume that Reynoldss average activity is 500 hours per month and that the company usually experiences overhead costs of 240,000 each year. Can you recommend a better way to assign overhead costs to jobs? Recompute the cost of each job and its price, given your method of overhead cost assignment. Which method do you think is best? Why?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

College Accounting, Chapters 1-27

Accounting

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:Cengage Learning,

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

College Accounting, Chapters 1-27 (New in Account...

Accounting

ISBN:9781305666160

Author:James A. Heintz, Robert W. Parry

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Cost Accounting - Definition, Purpose, Types, How it Works?; Author: WallStreetMojo;https://www.youtube.com/watch?v=AwrwUf8vYEY;License: Standard YouTube License, CC-BY