Concept explainers

Videos

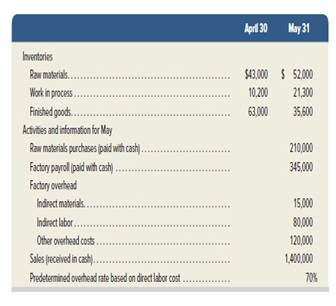

Exercise 19-10

Use information in Exercise 19-7 to prepare journal entries for the following events for the month of May.

1. Incurred other overhead costs (record credit to Other Accounts).

2. Applied overhead to work in process.

Exercise 19-7

Cost flows in a

P1 P2 P3 P4

The following information is available for Lock-Tite Company, which produces special-order security products and uses a job order costing system.

Compute the following amounts for the month of May.

1. Cost of direct materials used.

2. Cost of direct labor used.

3. Cost of goods manufactured.

4. Cost of goods sold.*

5. Gross profit.

6. Overapplied or underapplied overhead.

*Do not consider any underapplied or overapplied overhead.

Check (3) $625,400

Want to see the full answer?

Check out a sample textbook solution

Chapter 19 Solutions

FUND.ACCT.PRIN.

- JOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M. Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or over applied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102,103, and 104, direct labor hours are 12, 000, 10,000, 11, 000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour. (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101104 using the predetermined factory overhead rate (see above). (i) Finished Job Nos. 101103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and for 50,000 and 45,400, respectively. (k) Transferred under- or over applied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). 2. Post the entries to the work in process and finished goods accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardJOURNAL ENTRIES FOR MATERIAL, LABOR, OVERHEAD, AND SALES Alert Enterprises had the following job order transactions during the month of April. Record the transactions in the general journal, including issuance of materials, labor, and factory overhead applied; completed jobs sent to finished goods inventory; closing of the under or over applied factory overhead to the cost of goods sold account; and sale of finished goods.arrow_forwardA companys Individual job sheets show these costs: Overhead is applied at 1.25 times the direct labor cost. Use the data on the cost sheets to perform these tasks: Apply overhead to each of the jobs. Prepare an entry to record the assignment of direct materials to work in process. Prepare an entry to record the assignment of direct labor to work in process. Prepare an entry to record the assignment of manufacturing overhead to work in process.arrow_forward

- A companys individual job sheets show these costs: Overhead is applied at 1.75 times the direct labor cost. Use the data on the cost sheets to perform these tasks: Apply overhead to each of the jobs. Prepare an entry to record the assignment of direct material to work in process. Prepare an entry to record the assignment of direct labor to work in process. Prepare an entry to record the assignment of manufacturing overhead to work in process.arrow_forwardKingsford Furnishings Company manufactures designer furniture. Kingsford Furnishings uses a job order cost system. Balances on April 1 from the materials ledger are as follows: The materials purchased during April are summarized from the receiving reports as follows: Materials were requisitioned to individual jobs as follows: The glue is not a significant cost, so it is treated as indirect materials (factory overhead). a. Journalize the entry to record the purchase of materials in April. b. Journalize the entry to record the requisition of materials in April. c. Determine the April 30 balances that would be shown in the materials ledger accounts.arrow_forward(Appendix 4A) Unit Cost, Ending Work in Process, Journal Entries During August, Leming Inc. worked on two jobs. Data relating to these two jobs follow: Overhead is assigned on the basis of direct labor hours at a rate of 11. During August, Job 64 was completed and transferred to Finished Goods. Job 65 was the only unfinished job at the end of the month. Required: 1. Calculate the per-unit cost of Job 64. 2. Compute the ending balance in the work-in-process account. 3. Prepare the journal entries reflecting the completion and sale on account of Job 64. The selling price is 175% of cost. (Note: Round all journal entry amounts to the nearest dollar.)arrow_forward

- Summary information from a companys job cost sheets shows the following information: What are the balances in the work in process inventory, finished goods Inventory, and cost of goods sold for April, May, and June?arrow_forwardSchumacher Industries Inc. manufactures recreational vehicles. Schumacher Industries uses a job order cost system. The time tickets from June jobs are summarized as follows: Factory overhead is applied to jobs on the basis of a predetermined overhead rate of 23 per direct labor hour. The direct labor rate is 29 per hour. a. Journalize the entry to record the factory labor costs. b. Journalize the entry to apply factory overhead to production for June.arrow_forwardA new company started production. Job 10 was completed, and Job 20 remains in production. Here is the information from job cost sheets from their first and only jobs so far: Using the information provided. A. What is the balance in work in process? B. What Is the balance in the finished goods inventory? C. If manufacturing overhead is applied on the basis of direct labor hours, what is the predetermined overhead rate?arrow_forward

- Journal Entries, Basic Cost Flows In December, Davis Company had the following cost flows: Required: 1. Prepare the journal entries to transfer costs from (a) Molding to Grinding, (b) Grinding to Finishing, and (c) Finishing to Finished Goods. 2. CONCEPTUAL CONNECTION Explain how the journal entries differ from a job-order cost system.arrow_forwardJOURNAL ENTRIES FOR MATERIAL, LABOR, OVERHEAD, AND SALES Micro Enterprises had the following job order transactions during the month of April. Record the transactions in the general journal, including issuance of materials, labor, and factory overhead applied; completed jobs sent to finished goods inventory; closing of the under- or overapplied factory overhead to the cost of goods sold account; and sale of finished goods. Apr.1 Purchased materials on account, 35,000. 10 Issued direct materials to Job No. 33, 10,000. 11 Issued direct materials to Job No. 34, 8,000. 12 Issued direct materials to Job No. 35, 11,000. 25 Incurred direct labor: On Job No. 33, 6,000 On Job No. 34, 4,000 On Job No. 35, 5,000 25 Applied factory overhead: To Job No. 33, 1,500 To Job No. 34, 1,200 To Job No. 35, 1,600 30 Transferred Job Nos. 3335 to the finished goods inventory account as products F, G, and H, respectively. 30 Sold products F, G, and H for 20,000, 16,000, and 22,000, respectively. 30 Actual factory overhead for Job Nos. 3335, 4,220.arrow_forwardOverhead Assignment: Actual and Normal Activity Compared Reynolds Printing Company specializes in wedding announcements. Reynolds uses an actual job-order costing system. An actual overhead rate is calculated at the end of each month using actual direct labor hours and overhead for the month. Once the actual cost of a job is determined, the customer is billed at actual cost plus 50%. During April, Mrs. Lucky, a good friend of owner Jane Reynolds, ordered three sets of wedding announcements to be delivered May 10, June 10, and July 10, respectively. Reynolds scheduled production for each order on May 7, June 7, and July 7, respectively. The orders were assigned job numbers 115, 116, and 117, respectively. Reynolds assured Mrs. Lucky that she would attend each of her daughters weddings. Out of sympathy and friendship, she also offered a lower price. Instead of cost plus 50%, she gave her a special price of cost plus 25%. Additionally, she agreed to wait until the final wedding to bill for the three jobs. On August 15, Reynolds asked her accountant to bring her the completed job-order cost sheets for Jobs 115, 116, and 117. She also gave instructions to lower the price as had been agreed upon. The cost sheets revealed the following information: Reynolds could not understand why the overhead costs assigned to Jobs 116 and 117 were so much higher than those for Job 115. She asked for an overhead cost summary sheet for the months of May, June, and July, which showed that actual overhead costs were 20,000 each month. She also discovered that direct labor hours worked on all jobs were 500 hours in May and 250 hours each in June and July. Required: 1. How do you think Mrs. Lucky will feel when she receives the bill for the three sets of wedding announcements? 2. Explain how the overhead costs were assigned to each job. 3. Assume that Reynoldss average activity is 500 hours per month and that the company usually experiences overhead costs of 240,000 each year. Can you recommend a better way to assign overhead costs to jobs? Recompute the cost of each job and its price, given your method of overhead cost assignment. Which method do you think is best? Why?arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning