Videos

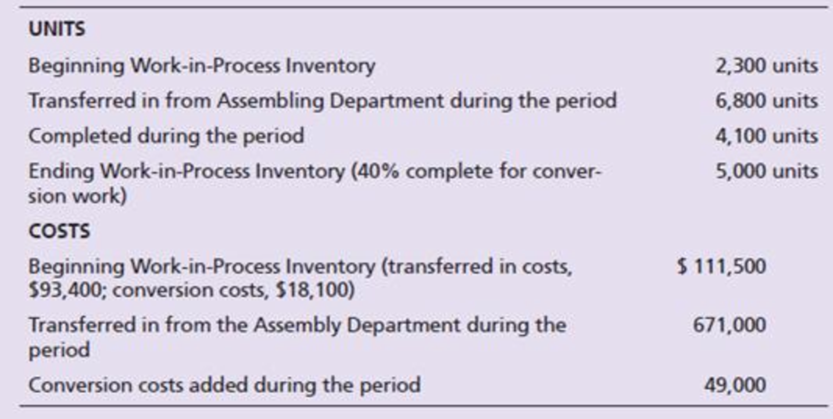

Sea Worthy uses three processes to manufacture lifts for personal watercrafts: forming a lift’s parts from galvanized steel, assembling the lift, and testing the completed lift. The lifts are transferred to finished goods before shipment to marinas across the country.

Sea Worthy’s Testing Department requires no direct materials. (Conversion costs are incurred evenly throughout the testing process. Other information follows for October 2018:

The cost transferred into Finished Goods Inventory is the cost of the lifts transferred out of the Testing Department. Sea Worthy uses weighted-average

Requirements

- 1. Prepare a production cost report for the Testing Department.

- 2. What is the cost per unit for lifts completed and transferred out to Finished Goods Inventory? Why would management be interested in this cost?

Want to see the full answer?

Check out a sample textbook solution

Chapter 18 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Additional Business Textbook Solutions

Auditing And Assurance Services

Principles of Accounting Volume 1

Horngren's Accounting (12th Edition)

Managerial Accounting

Advanced Financial Accounting

FINANCIAL ACCT.FUND.(LOOSELEAF)

- The management of Ramir Manufacturing Company is trying to decide whether to continue manufacturing a part or to buy it from an outside supplier. The part, called BROCO, is a component of the company's finished product. The following information was collected from the accounting records and production data for the year ending December 31, 2022. 1. 8,000 units of BROCO were produced in the Production Department. 2. Variable manufacturing costs applicable to the production of each BROCO unit were: direct materials $4.80, direct labor $4.30, indirect labor $0.43, utilities $0.40. Fixed manufacturing costs applicable to the production of BROCO were: 3. Cost Item Depreciation Property taxes Insurance Direct $2,100 500 900 $3.500 Allocated $ 900 200 600 $1,700 Total $3,000 700 1,500 $5.200 All variable manufacturing and direct fixed costs will be eliminated if BROCO is purchased. Allocated costs will not be eliminated if BROCO is purchased. So if BROCO is purchased, the fixed manufacturing…arrow_forwardMatterhorn,Inc., produces a special line of toy racing cars. Matterhorn produces the cars in batches. To manufacture each batch of the cars, Matterhorn must set up the machines and molds. Setup costs are batch-level costs and are fixed with respect to the number of setup-hours. A separate Setup Department is responsible for setting up machines and molds for each style of car. The following information pertains to July 2017: Calculate the following: a. the spending variance for fixed setup overhead costs; b. the budgeted fixed setup overhead rate; and c. the production-volume variance for fixed overhead setup costs. Actual Amounts Static-budget Amounts Units produced and sold 15,000 (Actual) 11,250 (Budgeted) Batch size (number of units per batch) 250 (Actual) 225 (Budgeted) Setup-hours per batch 5 (Actual) 5.25 (Budgeted) Total fixed setup overhead costs $12,000 (Actual) $9,975 (Budgeted)arrow_forwardIn its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. It sells the products at cost. The direct materials costs are zero, but the operation requires the use of direct labor and overhead. The company uses a process costing system and tracks the processing volume and costs incurred in each period. At the start of the current period, 550 towels were in process and were 60 percent complete. The costs incurred were $1,207. During the month, costs of $20,500 were incurred, 4,100 towels were started, and 275 towels were still in process at the end of the month. At the end of the month, the towels were 20 percent complete. Required: a. Prepare a production cost report; the company uses weighted-average process costing. b. Show the flow of costs through T-accounts. Assume that current period conversion costs are credited to various payables. i did A i want help in barrow_forward

- In its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. It sells the products at cost. The direct materials costs are zero, but the operation requires the use of direct labor and overhead. The company uses a process costing system and tracks the processing volume and costs incurred in each period. At the start of the current period, 550 towels were in process and were 60 percent complete. The costs incurred were $1,207. During the month, costs of $20,500 were incurred, 4,100 towels were started, and 275 towels were still in process at the end of the month. At the end of the month, the towels were 20 percent complete. Required: a. Prepare a production cost report; the company uses weighted-average process costing. b. Show the flow of costs through T-accounts. Assume that current period conversion costs are credited to various payables. i did A part , i want help in Barrow_forwardIn its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. It sells the products at cost. The direct materials costs are zero, but the operation requires the use of direct labor and overhead. The company uses a process costing system and tracks the processing volume and costs incurred in each period. At the start of the current period, 550 towels were in process and were 60 percent complete. The costs incurred were $1,207. During the month, costs of $20,500 were incurred, 4,100 towels were started, and 275 towels were still in process at the end of the month. At the end of the month, the towels were 20 percent complete. Required: a. Prepare a production cost report; the company uses weighted-average process costing. b. Show the flow of costs through T-accounts. Assume that current period conversion costs are credited to various payables.arrow_forwardMichael's Pottery makes decorative garden pieces using three consecutive processes: Moulding, Baking & Spraying. Quality control check takes place during the process, at which point, rejected units are separated from good units. The following details relate to production for the month of October 2020, for the Baking Department. i) Work-in-process, October 1: -0- ii) Transfer from Moulding: 2,000 units valued at $336.40 each ii) Other manufacturing costs incurred during October: $202,120 $212,840 Direct material added Direct Manufacturing Wages Manufacturing Overhead Applied $306,160 iv) Normal losses are estimated to be 5% of the units transferred in during the period. Losses from the Baking Department are deemed to be scrap and sold at $382 each. v) At inspection 300 decorative pieces were rejected as scrap. These units had reached the following degree of completion: From Moulding 100% Direct material added 40% Conversion costs 12½% vi) 1,200 pieces were completed and transferred out…arrow_forward

- Michael's Pottery makes decorative garden pieces using three consecutive processes: Moulding, Baking & Spraying. Quality control check takes place during the process, at which point, rejected units are separated from good units. The following details relate to production for the month of October 2020, for the Baking Department. i) Work-in-process, October 1: -0- ii) Transfer from Moulding: 2,000 units valued at $336.40 each iii) Other manufacturing costs incurred during October: Direct material added $202,120 Direct Manufacturing Wages $212,840 Manufacturing Overhead Applied $306,160 iv) Normal losses are estimated to be 5% of the units transferred in during the period. Losses from the Baking Department are deemed to be scrap and sold at $382 each. v) At inspection 300 decorative pieces were rejected as scrap. These units had reached the following degree of completion: From Moulding 100% Direct material added 40% Conversion costs 12%% vi) 1,200 pieces were completed and transferred out…arrow_forwardMichael's Pottery makes decorative garden pieces using three consecutive processes: Moulding, Baking & Spraying. Quality control check takes place during the process, at which point, rejected units are separated from good units. The following details relate to production for the month of October 2020, for the Baking Department. i) Work-in-process, October 1: -0- ii) Transfer from Moulding: 2,000 units valued at $336.40 each iii) Other manufacturing costs incurred during October: Direct material added $202,120 Direct Manufacturing Wages $212,840 Manufacturing Overhead Applied $306,160 iv) Normal losses are estimated to be 5% of the units transferred in during the period. Losses from the Baking Department are deemed to be scrap and sold at $382 each. v) At inspection 300 decorative pieces were rejected as scrap. These units had reached the following degree of completion: From Moulding 100% Direct material added 40% Conversion costs 12%% vi) 1,200 pieces were completed and transferred out…arrow_forwardMichael’s Pottery makes decorative garden pieces using three consecutive processes: Moulding, Baking & Spraying. Quality control check takes place during the process, at which point, rejected units are separated from good units. The following details relate to production for the month of October 2020, for the Baking Department. i) Work-in-process, October 1: -0- ii) Transfer from Moulding: 2,000 units valued at $336.40 each iii) Other manufacturing costs incurred during October: Direct material added $202,120 Direct Manufacturing Wages $212,840 Manufacturing Overhead Applied $306,160 iv) Normal losses are estimated to be 5% of the units transferred in during the period. Losses from the Baking Department are deemed to be scrap and sold at $382 each. v) At inspection 300 decorative pieces were rejected as scrap. These units had reached the following degree of completion: From Moulding 100% Direct material added 40% Conversion costs 12½%…arrow_forward

- Michael’s Pottery makes decorative garden pieces using three consecutive processes: Moulding, Baking & Spraying. Quality control check takes place during the process, at which point, rejected units are separated from good units. The following details relate to production for the month of October 2020, for the Baking Department. i) Work-in-process, October 1: -0- ii) Transfer from Moulding: 2,000 units valued at $336.40 each iii) Other manufacturing costs incurred during October: Direct material added Direct Manufacturing Wages Manufacturing Overhead Applied $202,120 $212,840 $306,160 iv) Normal losses are estimated to be 5% of the units transferred in during the period. Losses from the Baking Department are deemed to be scrap and sold at $382 each. v) At inspection 300 decorative pieces were rejected as scrap. These units had reached the following degree of completion: From Moulding Direct material added Conversion costs 100% 40% 12½% vi) 1,200 pieces were completed and transferred…arrow_forwardLally, Inc. produces universal remote controls. Lally uses a JIT costing system. One of the company's products has a standard direct materials cost of $9 per unit and a standard conversion cost of $35 per unit. During January 2018, Lally produced 500 units and sold 495 units on account at $45 each. It purchased $4,800 of direct materials on the account and incurred actual conversion costs totaling $14,000. Requiremets : 1. Prepare summary jounal entries for January. 2. The January 1, 2018, balance of the Raw and In-Process inventory account was $70. Use a T - account to find the January 31 balance. 3. Use a T - account to determine wheither conversion costs are overallocated or unerallocated for the month. By how much? Prepare the journal entry to adjust the Conversion Costs account.arrow_forwardMichael's Pottery makes decorative garden pieces using three consecutive processes: Moulding, Baking & Spraying. Quality control check takes place during the process, at which point, rejected units are separated from good units. The following details relate to production for the month of October 2020, for the Baking Department. i) Work-in-process, October 1: -0- i) Transfer from Moulding: 2,000 units valued at $336.40 each ii) Other manufacturing costs incurred during October: Direct material added $202,120 Direct Manufacturing Wages $212,840 Manufacturing Overhead Applied $306,160 iv) Normal losses are estimated to be 5% of the units transferred in during the period. Losses from the Baking Department are deemed to be scrap and sold at $382 each. v) At inspection 300 decorative pieces were rejected as scrap. These units had reached the following degree of completion: From Moulding 100% Direct material added 40% Conversion costs 12%% vi) 1,200 pieces were completed and transferred out…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education