Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

4th Edition

ISBN: 9780134083278

Author: Jonathan Berk, Peter DeMarzo

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 16, Problem 13P

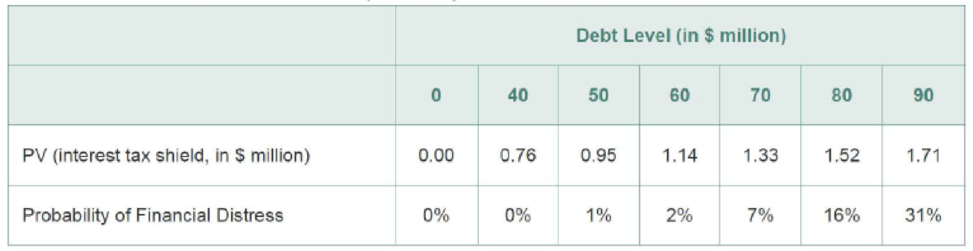

Your firm is considering issuing one-year debt, and has come up with the following estimates of the value of the interest tax shield and the probability of distress for different levels of debt:

Suppose the firm has a beta of zero, so that the appropriate discount rate for financial distress costs is the risk-free rate of 5%. Which level of debt above is optimal if, in the event of distress, the firm will have distress costs equal to

- a. $2 million?

- b. $5 million?

- c. $25 million?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

(Use the following information for the next three questions). Consider a

world with taxes but no other market imperfections. BLT machinery has a debt

to equity ratio of 2/3. Its cost of equity is 20%, cost of debt is 4%, and tax rate is

35%. Assume that the risk-free rate is 4%, and market risk premium is 8%.

Suppose the firm repurchases stock and finances the repurchase with debt,

causing its debt to equity ratio to change to 3/2.

What is the firm's new cost of equity?

None of the choices

New cost of equity is 26.05%

New cost of equity is 23.59%

New cost of equity is 16.32%

New cost of equity is 28.00%

Your firm is targeting specific debt levels in the future. Cost of debt (RB) is 7%. The

risk-free rate is 4% and the expected market risk premium is 6%. Your firm's

unlevered (asset) beta is 1.

What is the appropriate rate to discount the interest tax shields associated with

your debt?

4.0%

6.00%

10.00%

12.57%

7.00%

Your firm has a target debt ratio of 30%. Cost of debt (RB) is 6%. The risk-free rate is 3% and the

expected market risk premium is 6%. Your firm's unlevered (asset) beta is 1.

What is the appropriate rate to discount the interest tax shields associated with your debt?

10.00%

11.57%

6.00%

9.00%

4.00%

Chapter 16 Solutions

Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

Ch. 16.1 - Prob. 1CCCh. 16.1 - Does the risk of default reduce the value of the...Ch. 16.2 - If a firm files for bankruptcy under Chapter 11 of...Ch. 16.2 - Why are the losses of debt holders whose claims...Ch. 16.3 - Prob. 1CCCh. 16.3 - True or False: If bankruptcy costs are only...Ch. 16.4 - Prob. 1CCCh. 16.4 - According to the trade-off theory, all else being...Ch. 16.5 - Prob. 1CCCh. 16.5 - Why would debt holders desire covenants that...

Ch. 16.6 - Prob. 1CCCh. 16.6 - Prob. 2CCCh. 16.7 - Coca-Cola Enterprises is almost 50% debt financed...Ch. 16.7 - Why would a firm with excessive leverage not...Ch. 16.7 - Describe how management entrenchment can affect...Ch. 16.8 - How does asymmetric information explain the...Ch. 16.8 - Prob. 2CCCh. 16.9 - Prob. 1CCCh. 16.9 - Prob. 2CCCh. 16 - Gladstone Corporation is about to launch a new...Ch. 16 - Baruk Industries has no cash and a debt obligation...Ch. 16 - When a firm defaults on its debt, debt holders...Ch. 16 - Prob. 4PCh. 16 - Prob. 5PCh. 16 - Suppose Tefco Corp. has a value of 100 million if...Ch. 16 - You have received two job offers. Firm A offers to...Ch. 16 - As in Problem 1, Gladstone Corporation is about to...Ch. 16 - Kohwe Corporation plans to issue equity to raise...Ch. 16 - Prob. 10PCh. 16 - Prob. 11PCh. 16 - Hawar International is a shipping firm with a...Ch. 16 - Your firm is considering issuing one-year debt,...Ch. 16 - Marpor Industries has no debt and expects to...Ch. 16 - Real estate purchases are often financed with at...Ch. 16 - On May 14, 2008, General Motors paid a dividend of...Ch. 16 - Prob. 17PCh. 16 - Consider a firm whose only asset is a plot of...Ch. 16 - Prob. 19PCh. 16 - Prob. 20PCh. 16 - Prob. 21PCh. 16 - Consider the setting of Problem 21 , and suppose...Ch. 16 - Consider the setting of Problems 21 and 22, and...Ch. 16 - You own your own firm, and you want to raise 30...Ch. 16 - Empire Industries forecasts net income this coming...Ch. 16 - Ralston Enterprises has assets that will have a...Ch. 16 - Prob. 27PCh. 16 - If it is managed efficiently, Remel Inc. will have...Ch. 16 - Which of the following industries have low optimal...Ch. 16 - According to the managerial entrenchment theory,...Ch. 16 - Info Systems Technology (IST) manufactures...Ch. 16 - Prob. 32PCh. 16 - Prob. 33P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Suppose Mullens Corporation is considering three average-risk projects with the following costs and rates of return: Project Cost Expected Rate of Return 1 $2,500 23.00% 2 $3,000 30.00% 3 $2,750 24.00% Mullens estimates that it can issue debt at a rate of rd=20.00%rd=20.00% and a tax rate of T=25.00%T=25.00%. It can issue preferred stock that pays a constant dividend of Dp=$20.00Dp=$20.00 per year and at Pp=$200.00Pp=$200.00 per share. Also, its common stock currently sells for P0=$16.00P0=$16.00 per share. The expected dividend payment of the common stock is D1=$4.00D1=$4.00 and the dividend is expected to grow at a constant annual rate of g=5.00%g=5.00% per year. Mullens’ target capital structure consists of ws=75.00%ws=75.00% common stock, wd=15.00%wd=15.00% debt, and wp=10.00%wp=10.00% preferred stock. 1.According to the video, the after-tax cost of debt can be stated as ________________ . Plugging in the values for rdrd and (T)T yields an after-tax cost of…arrow_forwardYou have the following initial information on which to base your calculations and discussion: Debt yield = 2.6% Required Rate of Return on Equity = 12% Expected return on S&P500 = 10% Risk-free rate (rF) = 1.5% Inflation = 2.5% Corporate tax rate (TC) = 30% Current long-term and target debt-equity ratio (D:E) = 1:3 a. What is the unlevered cost of equity (rE*) for this firm? Assume that the management of the firm is considering a leveraged buyout of the above company. They believe that they can gear the company to a higher level due to their ability to extract efficiencies from the firm’s operations. Thus, they wish to use a target debt-equity ratio of 3:1 in their valuation calculations. b. What would the levered cost of equity equal for this firm at a debt-equity ratio (D:E) of 3:1? c. What would the required rate of return for the company equal if it were to be acquired under the leveraged buyout structure (i.e., what would the estimated firm WACC equal to under a…arrow_forwardYou have the following initial information on which to base your calculations and discussion: Debt yield = 2.5% Required Rate of Return on Equity = 13% Expected return on S&P500 = 8% Risk-free rate (rF) = 1.5% Inflation = 2.5% Corporate tax rate (TC) = 30% Current long-term and target debt-equity ratio (D:E) = 1:3 a. What is the unlevered cost of equity (rE*) for this firm? Assume that the management of the firm is considering a leveraged buyout of the above company. They believe that they can gear the company to a higher level due to their ability to extract efficiencies from the firm’s operations. Thus, they wish to use a target debt-equity ratio of 3:1 in their valuation calculations.arrow_forward

- Based in the U.S., Your firm faces a 25% chance of a potential loss of $20 million next year. If yourfirm implements new policies, it can reduce the chance of this loss by 10%, but these new policieshave an upfront cost of $300,000. Suppose the beta of the loss is 0, and the risk-free interest rate5%.ISa) If the firm is uninsured, what is the NPV of implementing the new policies?b) If the firm is fully insured, what is the NPV of implementing the new policies?c) Given your answer to question b), what is the actuarially fair cost of full insurance?d) What is the minimum-size deductible that would leave your firm with an incentive toimplement the new policies?e) What is the actuarially fair price of an insurance policy with the deductible in question darrow_forwardBeing Finance Manager of Salalah Textiles Industries, you need to invest an amount for OMR 50,000 in the investment market. Assume the market rate of return is 0.11, risk free rate of return is 2.75% and Beta is .73, then:Required:a) What should be required rate of return for your investment?arrow_forwardWhere do we generally find optimal level of debt? A. where the tax shield is maximized B. the amount of debt such that the YTM is 5.5% or less C. where debt equals equity D. whatever will yield a FICO sore of 700 or better E. consistent with a low investment grade debt ratingarrow_forward

- Consider a two-date binomial model. A company has both debt and equity in its capital structure. The value of the company is 100 at Date 0. At Date 1, it is equally like that the value of the company increases by 20% or decreases by 10%. The total promised amount to the debtholders is 100 at Date 1. The riskfree interest rate is 10%. a. What is the value of the debt at Date 0? What is the value of the equity at Date 0? b. Suppose the government announces that it guarantees the company’s payment to the debtholders. How much is the government guarantee worth?arrow_forwardA firm is considering two investment projects, Y and Z. These projects are NOT mutually exclusive. Assume the firm is not capital constrained. The initial costs and cashflows for these projects are: 0 1 2 3 Y -40,000 17,000 17,000 15,000 Z -28,000 12,000 12,000 20,000 Using a discount rate of 9% calculate the net present value for each project. What decision would you make based on your calculations? How would your decision change if the discount rate used for calculating the net present value is 15%? Calculate an approximate IRR for each project. Assume the hurdle rate is 9%. What decision would you make based on your calculations? Calculate the payback period for each project. The company looks to select investment projects paying back in 2 years. What decision would you make based on your calculations? Critically discuss Net Present Value (NPV), Internal Rate of Return (IRR) and payback period as criteria for investment appraisal.arrow_forwardConsider a two-date binomial model. A company has both debt and equity in its capital structure. The value of the company is 100 at Date 0. At Date 1, it is equally like that the value of the company increases by 20% or decreases by 10%. The total promised amount to the debtholders is 100 at Date 1. The riskfree interest rate is 10%. a. What are the possible payoffs to the equityholders at date 1? What kind of financial product has the same payoffs? Please describe the detailed characteristics of the financial product. b. What are the possible payoffs to the bondholders at date 1? Are they riskfree? What kind of financial product/portfolio has the same payoffs? Please describe the detailed characteristics of the financial product/portfolio.arrow_forward

- A firm is considering a project that will generate perpetual after-tax cash flows of $16,500 per year beginning next year. The project has the same risk as the firm's overall operations and must be financed externally. Equity flotation costs 14 percent and debt issues cost 3 percent on an after-tax basis. The firm's D/E ratio is 0.5. What is the most the firm can pay for the project and still earn its required return? Note: Do not round intermediate calculations. Round your answer to the nearest whole dollar. Maximum the firm can payarrow_forwardMantap Industries has three projects under consideration. Project L is a lower-than-averagerisk project, project A is an average-risk project, and project H is a higher-than-average-riskproject. You have gathered the following information to determine if one or more of theseprojects has an acceptable rate of return for the firm.• Sources of financing 50% debt and 50% equity• Rd = 8.00% before taxes• Tax Rate = 30%• Average beta for Mantap Industries = 1.0• Rm = 13.00%• Rf = 4.00%• Adjusted WACC = 9.30%• Beta for project L = 0.80, for project A = 1.00, and for project H = 1.20• IRRL = 9.00%, IRRA = 10.00%, and IRRH = 11.00%Calculate the required rate of return for each project and determine which, if any, projects are acceptable to the firmarrow_forwardEstablish a finance plan that assumes the sales estimates at the take price level would have been increased by $500,000. This means that the current take price level of $9,170,000 would increase by $500,000. This change would offer more collateral to the bank, and the bank would then increase the GAP loan. The GAP loan requires 200% collateral in unsold rights. This change would impact the equity investment. Question: What would be the new equity investment be if the budget stays the same?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

The U.S. Treasury Markets Explained | Office Hours with Gary Gensler; Author: U.S. Securities and Exchange Commission;https://www.youtube.com/watch?v=uKXZSzY2ZbA;License: Standard Youtube License