Videos

Identifying Relevant Costs

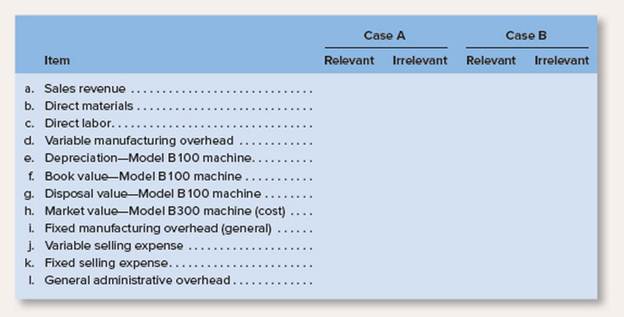

Syahn, AB, is a Swedish manufacturer of sailing yachts The company has assembled the information shown below that pertains to two independent decision-making contexts called Case A and Case B:

Case A:

The company chronically has no idle capacity and the old Model B100 machine is the company’s constraint Management is considering purchasing a Model B300 machine to use in addition to the company’s present Model B100 machine. The old Model B100 machine will continue to be used to capacity as before, with the new Model B300 machine being used to expand production. This will increase the company’s production and sales. The increase in volume will be large enough to require increases in fixed selling expenses and in general administrative

Cue B:

The old Model B100 machine is not the company’s constraint, but management is considering replacing it with a new Model B300 machine because of the potential savings in direct materials with the new machine The Model B100 machine would be sold. This change will have no effect on production or sales, other than some savings in direct materials costs due to less waste.

Required:

Copy the information below onto your answer sheet and place an x in the appropriate column to indicate whether each item is relevant or irrelevant to the decision context described in Case A and Case B.

Want to see the full answer?

Check out a sample textbook solution

Chapter 11 Solutions

Introduction To Managerial Accounting

- Value- and Nonvalue-Added Costs Waterfun Technology produces engines for recreational boats. Because of competitive pressures, the company was makong an effort to reduce costs. A part of this effort, management implemented an activity-based management system and began focusing its attention an procetses and activties. Receiving was among the processes (activities) that were carefully studied. The study revealed that the number of receiving orders was a good dnver fur receiving costs. During the last year, the company incurred fixed receiving costs of $630,000 (salaries of 10 empleyees). These fxed costa provide a capacity of processing 72,000 receiving orders (7,200 per employee at practical capacity). Management decided that the efficient level for receiving should use 36,000 receiving orders. Requiredi 1. Explain why receiving would be viewed as a value-added activity. Which of these are possible reasons that explain why the demand for receiving is more than the efficient level of…arrow_forwardSalem Electronics currently produces two products: a programmable calculator and a tape recorder. A recent marketing study indicated that consumers would react favorably to a radio with the Salem brand name. Owner Kenneth Booth was interested in the possibility. Before any commitment was made, however, Kenneth wanted to know what the incremental fixed costs would be and how many radios must be sold to cover these costs. In response, Betty Johnson, the marketing manager, gathered data for the current products to help in projecting overhead costs for the new product. The overhead costs based on 30,000 direct labor hours follow. (The high-low method using direct labor hours as the independent variable was used to determine the fixed and variable costs.) All depreciation. The following activity data were also gathered: Betty was told that a plantwide overhead rate was used to assign overhead costs based on direct labor hours. She was also informed by engineering that if 20,000 radios were produced and sold (her projection based on her marketing study), they would have the same activity data as the recorders (use the same direct labor hours, machine hours, setups, and so on). Engineering also provided the following additional estimates for the proposed product line: Upon receiving these estimates, Betty did some quick calculations and became quite excited. With a selling price of 26 and just 18,000 of additional fixed costs, only 4,500 units had to be sold to break even. Since Betty was confident that 20,000 units could be sold, she was prepared to strongly recommend the new product line. Required: 1. Reproduce Bettys break-even calculation using conventional cost assignments. How much additional profit would be expected under this scenario, assuming that 20,000 radios are sold? 2. Use an activity-based costing approach, and calculate the break-even point and the incremental profit that would be earned on sales of 20,000 units. 3. Explain why the CVP analysis done in Requirement 2 is more accurate than the analysis done in Requirement 1. What recommendation would you make?arrow_forwardBoston Executive. Inc., produces executive limousines and currently manufactures the mini-bar inset at these costs: The company received an offer from Elite Mini-Bars to produce the insets for $2,100 per Unit and supply 1,000 mini-bars for the coming years estimated production. If the company accepts this offer and shuts down production of this part of the business, production workers and supervisors will be reassigned to other areas. Assume that for the short-term decision-making process demonstrated in this problem, the companys total labor costs (direct labor and supervisor salaries) will remain the same if the bar inserts are purchased. The specialized equipment cannot be used and has no market value. However, the space occupied by the mini bar production can be used by a different production group that will lease it for $55,000 per year. Should the company make or buy the mini-bar insert?arrow_forward

- .A Company produces Optimist sailboats. The costs of producing 107000 tiller extensions for use in the boats are as follows:Direct labor $253000Direct materials 302000Variable overhead 66000Fixed overhead 185000An outside supplier has offered to supply the tiller extensions for $725000. If the company accepts the offer $86000 of fixed costs can be avoided. What is the financial advantage (disadvantage) of accepting the supplier’s offer?arrow_forwardConcord Company produces Optimist sailboats. The costs of producing 107000 tiller extensions for use in the boats are as follows: Direct labor $253000 Direct materials 302000 Variable overhead 66000 Fixed overhead 185000 An outside supplier has offered to supply the tiller extensions for $725000. If Concord accepts the offer $86000 of fixed costs can be avoided. What is the financial advantage (disadvantage) of accepting the supplier’s offer? $26000 ($5000) ($26000) $5000arrow_forward! Required information [The following information applies to the questions displayed below.] Each of the following situations is independent: Make or Buy Terry Incorporated manufactures machine parts for aircraft engines. CEO Bucky Walters is considering an offer from a subcontractor to provide 2,350 units of product OP89 for $190,350. If Terry does not purchase these parts from the subcontractor, it must continue to produce them in-house with these costs: Direct materials Direct labor Variable overhead Allocated fixed overhead Required: Cost per Unit $ 35 25 23 4 1. What is the relevant cost per unit to make the product internally? 2. What is the estimated increase or decrease in short-term operating profit of producing the product internally versus purchasing the product from a supplier?arrow_forward

- Value chain and classification of costs, computer company. Dell Computer incurs the following costs:a. Utility costs for the plant assembling the Latitude computer line of productsb. Distribution costs for shipping the Latitude line of products to a retail chainc. Payment to David Newbury Designs for design of the XPS 2-in-1 laptopd. Salary of computer scientist working on the next generation of serverse. Cost of Dell employees’ visit to a major customer to demonstrate Dell’s ability to interconnect withother computersf. Purchase of competitors’ products for testing against potential Dell productsg. Payment to business magazine for running Dell advertisementsh. Cost of cartridges purchased from outside supplier to be used with Dell printersarrow_forwardMaking outsourcing decisions Cold Sports manufactures snowboards. Its cost of making 2,000 bindings is as follows: Suppose Topnotch will sell bindings to Cold Sports for $15 each. Cold Sports would pay $3 per unit to transport the bindings to its manufacturing plant, where it would add its own logo at a cost of $0.50 per binding. Requirements Cold Sports’s accountants predict that purchasing the bindings from Topnotch will enable the company to avoid $2,300 of fixed overhead. Prepare an analysis to show whether Cold Sports should make or buy the bindings. The facilities freed by purchasing bindings from Topnotch can be used to manufacture another product that will contribute $3,100 to profit. Total fixed costs will be the same as if Cold Sports had produced the bindings. Show which alternative makes the best use of Cold Sports’s facilities: (a) make bindings, (b) buy bindings and leave facilities idle, or (c) buy bindings and make another product.arrow_forwardMohave Corporation is considering outsourcing production of the umbrella tote bag included with some of its products. The company has received a bid from a supplier in Vietnam to produce 8,900 units per year for $7.50 each. Mohave the following information about the cost of producing tote bags: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Total cost per unit Mohave determined all variable costs could be eliminated by outsourcing the tote bags, while 70 percent of the fixed overhead cost is unavoidable. At this time, Mohave has no specific use in mind for the space currently dedicated to producing the tote bags. Required: 1. Compute the difference in cost between making and buying the umbrella tote bag. 2. Based strictly on the incremental analysis, should Mohave buy the tote bags or continue to make them? 3-a. Suppose the space Mohave currently uses to make the bags could be utilized by a new product line that would generate $12,000 in…arrow_forward

- Mohave Corporation is considering outsourcing production of the umbrella tote bag included with some of its products. The company has received a bid from a supplier in Vietnam to produce 8.200 units per year for $9.50 each Mohave the following information about the cost of producing tote bags: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Total cost per unit Mohave determined all variable costs could be eliminated by outsourcing the tote bags, while 60 percent of the fixed overhead cost is unavoidable. At this time, Mohave has no specific use in mind for the space currently dedicated to producing the tote bags Required: 1. Compute the difference in cost between making and buying the umbrella tote bag 2. Based strictly on the incremental analysis, should Mohave buy the tote bags or continue to make them? 3-0. Suppose the space Mohave currently uses to make the bags could be utilized by a new product line that would generate $10,000 in annual…arrow_forwardCost Estimation; Machine Replacement; Ethics Hardison Inc. manufactures glass for officebuildings in Florida. As a result of age and wear, a critical machine in the production process hasbegun to produce quality defects. Hardison is considering replacing the old machine with a newmachine, either brand A or brand B. The manufacturer has provided Hardison with the following dataon the costs of operation of each machine brand at various levels of output:Output(square yards)Brand AEstimated Total CostsBrand BEstimated Total Costs2,000 $ 97,000 $ 120,0004,000 125,000 160,0008,000 180,000 200,00016,000 225,000 260,00032,000 280,000 300,00064,000 438,000 368,000Required1. Graph the data for the two brands of machines.2. Use the high-low method to determine the cost equation for each brand of machine and use the results tocalculate the costs of operating each machine if Hardison’s output is expected to be 25,000 square yardsarrow_forwardPharoah Company has decided to introduce a new product. The new product can be manufactured by either a capital-intensive method or a labor-intensive method. The manufacturing method will not affect the quality of the product. The estimated manufacturing costs by the two methods are as follows. Direct materials Direct labor Variable overhead Fixed manufacturing costs (a) Pharoah' market research department has recommended an introductory unit sales price of $28.00. The selling expenses are estimated to be $432,000 annually plus $2.00 for each unit sold, regardless of manufacturing method. Capital-Intensive $4.00 per unit $5.00 per unit $3.00 per unit $2,284,000 Calculate the estimated break-even point in annual unit sales of the new product if Pharoah Company uses the: 1. Capital-intensive manufacturing method. Labor-intensive manufacturing method. 2. Labor-Intensive $4.50 per unit $7.00 per unit $4.00 per unit $1,437,000 Break-even point in units Capital-Intensive Labor-Intensivearrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning