Concept explainers

Videos

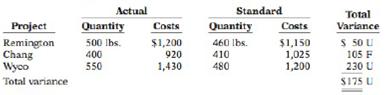

Picard Landscaping plants grass seed as the basic landscaping for business campuses. During a recent month, the company worked on three projects (Remington, Chang, and Wyco). The company is interested in controlling the materials costs, namely the grass seed, for these plantings projects.

In order to provide management with useful cost control information, the company uses

Shown below are quantity and cost data for each project.

Instructions

(a) Prepare a variance report for the purchasing department with the following columns: (1) Project, (2) Actual Pounds Purchased, (3) Actual Price per Pound, (4) Standard Price per Pound, (5) Price Variance, and (6) Explanation.

(b) Prepare a variance report for the production department with the following columns: (1) Project, (2) Actual Pounds, (3) Standard Pounds, (4) Standard Price per Pound, (5) Quantity Variance, and (6) Explanation.

Want to see the full answer?

Check out a sample textbook solution

Chapter 11 Solutions

Managerial Accounting: Tools for Business Decision Making

Additional Business Textbook Solutions

Financial Accounting

Managerial Accounting (5th Edition)

Horngren's Accounting (11th Edition)

Intermediate Accounting (2nd Edition)

Financial Accounting, Student Value Edition (4th Edition)

- Hart Labs, Inc. provides mad cow disease testing for both state and federal governmental agricultural agencies. Because the company's customers are governmental agencies, prices are strictly regulated. Therefore, Hart Labs must constantly monitor and control its testing costs. Shown below are the standard costs for a typical test. Direct materials (2 test tubes @ $1.90 per tube) Direct labor (1 hour @ $30 per hour) Variable overhead (1 hour @ $6.00 per hour) Fixed overhead (1 hour @ $12.00 per hour) Total standard cost per test Direct materials (2,310 test tubes) Direct labor (1,133 hours) Variable overhead Fixed overhead $3.80 $4,158 32,857 6,336 12,672 30.00 6.00 12.00 The lab does not maintain an inventory of test tubes. As a result, the tubes purchased each month are used that month. Actual activity for the month of November 2020, when 1,100 tests were conducted, resulted in the following. $51.80 Monthly budgeted fixed overhead is $16,560. Revenues for the month were $73,700, and…arrow_forwardWaterfun Technology produces engines for recreational boats. Because of competitive pressures, the company was making an effort to reduce costs. As part of this effort, management implemented an activity-based management system and began focusing its attention on processes and activities. Receiving was among the processes (activities) that were carefully studied. The study revealed that the number of receiving orders was a good driver for receiving costs. During the last year, the company incurred fixed receiving costs of $630,000 (salaries of 10 employees). These fixed costs provide a capacity of processing 72,000 receiving orders (7,200 per employee at practical capacity). Management decided that the efficient level for receiving should use 36,000 receiving orders. Required: 1. Explain why receiving would be viewed as a value-added activity. Which of these are possible reasons that explain why the demand for receiving is more than the efficient level of 36,000 orders. 2. Break…arrow_forwardMathes Corporation manufactures paper products. The company operates a landfill, which it uses to dispose of nonhazardous trash. The trash is hauled from the two nearby manufacturing facilities in trucks that can carry up to four tons of trash In a load. The landfill operation requires certain preparation activities regardless of the amount of trash in a truck (Le., for each load). The budget for the landfill for next year follows. volume of trash Preparation costs (varies by loads) other variable costs (varies by tons) Fixed costs 1,200 tons (300 loads) $ 54,000 54,000 178,000 $286, 000 Total budgeted costs Mathes is considering making the landfill a profit center and charging the manufacturing plants for disposal of the trash. The landfill has sufficlent capacity to operate for at least the next 20 years. Other landfills are available in the area (both private and municipal), and each plant would be free to declde which landfill to use. Required: a. Compute the optimal transfer…arrow_forward

- Hart Labs, Inc. provides mad cow disease testing for both state and federal governmental agricultural agencies. Because the company’s customers are governmental agencies, prices are strictly regulated. Therefore, Hart Labs must constantly monitor and control its testing costs. Shown below are the standard costs for a typical test. Direct materials (2 test tubes @ $1.46 per tube) $2.92 Direct labor (1 hour @ $24 per hour) 24.00 Variable overhead (1 hour @ $6 per hour) 6.00 Fixed overhead (1 hour @ $10 per hour) 10.00 Total standard cost per test $42.92 The lab does not maintain an inventory of test tubes. As a result, the tubes purchased each month are used that month. Actual activity for the month of November 2020, when 1,475 tests were conducted, resulted in the following. Direct materials (3,050 test tubes) $4,270 Direct labor (1,550 hours) 35,650 Variable overhead 7,400 Fixed overhead 15,000 Monthly budgeted fixed overhead is…arrow_forwardWaterfun Technology produces engines for recreational boats. Because of competitive pressures, the company was making an effort to reduce costs. As part of this effort, management implemented an activity-based management system and began focusing its attention on processes and activities. Receiving was among the processes (activities) that were carefully studied. The study revealed that the number of receiving orders was a good driver for receiving costs. During the last year, the company incurred fixed receiving costs of $630,000 (salaries of 10 employees). These fixed costs provide a capacity of processing 72,000 receiving orders (7,200 per employee at practical capacity). Management decided that the efficient level for receiving should use 36,000 receiving orders. Required: 1. Explain why receiving would be viewed as a value-added activity. List all possible reasons. Also, list some possible reasons that explain why the demand for receiving is more than the efficient level of…arrow_forwardHart Labs, Inc. provides mad cow disease testing for both state and federal governmental agricultural agencies. Because the company's customers are governmental agencies, prices are strictly regulated. Therefore, Hart Labs must constantly monitor and control its testing costs. Shown below are the standard costs for a typical test. Direct materials (2 test tubes @ $1.00 per tube) $2.00 Direct labor (1 hour @ $32 per hour) 32.00 Variable overhead (1 hour @ $6.00 per hour) 6.00 Fixed overhead (1 hour @ $13.00 per hour) 13.00 Total standard cost per test $53.00 The lab does not maintain an inventory of test tubes. As a result, the tubes purchased each month are used that month. Actual activity for the month of November 2020, when 1,400 tests were conducted, resulted in the following. Direct materials (2,940 test tubes) $2,646 Direct labor (1,442 hours) 44,702 Variable overhead 8,512 Fixed overhead 16,968 Monthly budgeted fixed overhead is $17,030. Revenues for the month were $93,800, and…arrow_forward

- Alexandria Ltd. manufactures high-quality pens. For many years the company manufactured only one type of pen (namely, ballpoint pens) but last year the company also began to manufacture fountain pens. The decision to begin manufacturing fountain pens was taken only after the company’s marketing manager confirmed that there was a significant niche market for fountain pens and the company’s cost accountant estimated that the cost of production for such pens would be much less than the selling price predicted by the marketing manager. When the fountain pen was introduced, sales (in terms of both quantity and price) were higher than expected. Nevertheless the overall profits of Alexandria Ltd. have declined steadily. As a result, the cost accountant decided that he should re-examine his estimate of the cost of producing the fountain pen, with particular reference to overhead costs. In his original analysis, he allocated all manufacturing overhead costs to products in proportion to direct…arrow_forwardMercury, Incorporated, produces cell phones at its plant in Texas. A year ago, a consumer survey ranked the company's cell phones low in product quality. Shocked by this result, Jorge Gomez, Mercury's president, set up a task force to implement a formal quality improvement program. Included on this task force were representatives from the Engineering, Marketing, Customer Service, Production, and Accounting departments. After working together for a year, the task force prepared the quality cost report shown below: Prevention costs: Machine maintenance Training suppliers Quality circles Total prevention cost Appraisal costs: Incoming inspection Final testing Total appraisal cost Internal failure costs: Rework Scrap Total internal failure cost External failure costs: Warranty repairs Customer returns Mercury, Incorporated Quality Cost Report (in thousands) Total external failure cost Total quality cost Total production cost Prevention costs: Machine maintenance Training suppliers Quality…arrow_forwardAlgonac Moldings produces a product made from a metal alloy. Two suppliers, Liebold Metal and Cecil Distributors, supply the alloy. Neither supplier can meet Algonac's typical demand, because of capacity constraints. The material from Liebold is less expensive to buy but more difficult to use, resulting in greater waste. The metal alloy is highly toxic and any waste requires costly handling to avoid environmental accidents. Last year the cost of handling the waste totaled $1,756,920. Additional data from last year's operations are shown as follows: Amount of material purchased (tons) Amount of waste (tons) Cost of purchases Req A1 Req A2 Liebold Metals Required: a. Allocate the cost of the waste-handling to the two suppliers based on: 1. Amount of material purchased. 2. Amount of waste. 3. Cost of material purchased. Req A3 Allocated waste handling cost 68.8 11.0 $ Complete this question by entering your answers in the tabs below. 2,178,581 Liebold Metals Cecil Distributors Amount of…arrow_forward

- Algonac Moldings produces a product made from a metal alloy. Two suppliers, Liebold Metal and Cecil Distributors, supply the alloy. Neither supplier can meet Algonac's typical demand, because of capacity constraints. The material from Liebold is less expensive to buy but more difficult to use, resulting in greater waste. The metal alloy is highly toxic and any waste requires costly handling to avoid environmental accidents. Last year the cost of handling the waste totaled $1,200,000. Additional data from last year’s operations are shown as follows: Liebold Metals Cecil Distributors Amount of material purchased (tons) 64.8 115.2 Amount of waste (tons) 9.0 11.0 Cost of purchases $ 1,488,000 $ 3,312,000 Required: Allocate the cost of the waste handling to the two suppliers based on: Amount of material purchased. Amount of waste. Cost of material purchased. Amount of material purchased. Note: Do not round intermediate calculations. A.)…arrow_forwardRico Company produces custom-made machine parts. Rico recently has implemented an activity-based management (ABM) system with the objective of reducing costs. Rico has begun analyzing each activity to determine ways to increase its efficiency. Setting up equipment was among the first group of activities to be carefully studied. The study revealed that setup hours was a good driver for the activity. During the last year, the company incurred fixed setup costs of $860,200 (salaries of 17 employees). The fixed costs provide a capacity of 39,100 hours (2,300 per employee at practical capacity). The setup activity was viewed as necessary, and the value- added standard was set at 2,300 hours. Actual setup hours used in the most recent period were 37,110. Required: 1. Calculate the volume and unused capacity variances for the setup activity. Enter all amounts as positive values. Volume Variance 22 Unused Capacity Variance $ Show Me How 2. Prepare a report that presents value-added, non varue…arrow_forwardYtze Inc. manufactures bath cubicles. The following activity information is available for its cubicles: Management is looking to remove $7.00 of activity cost from the product in order to make the price more competitive. Assume the process improvement is put in place such assembly as well as setup required one-fourth less time to complete per unit. Based on the data, identify the correct statement. a. These process improvements reduced the activity cost of each battery from $49.00 to $43.00, or $6, thus not exceeding the $7.00 target. b. These process improvements reduced the activity cost of each battery from $49.00 to $44.00, or $5, thus not exceeding the $7.00 target. c. These process improvements reduced the activity cost of each battery from $49.00 to $42.00, or $7, thus exceeding the $7.00 target. d. These process improvements reduced the activity cost of each battery from $49.00 to $41.00, or $8, thus exceeding the $7.00 target.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning