Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

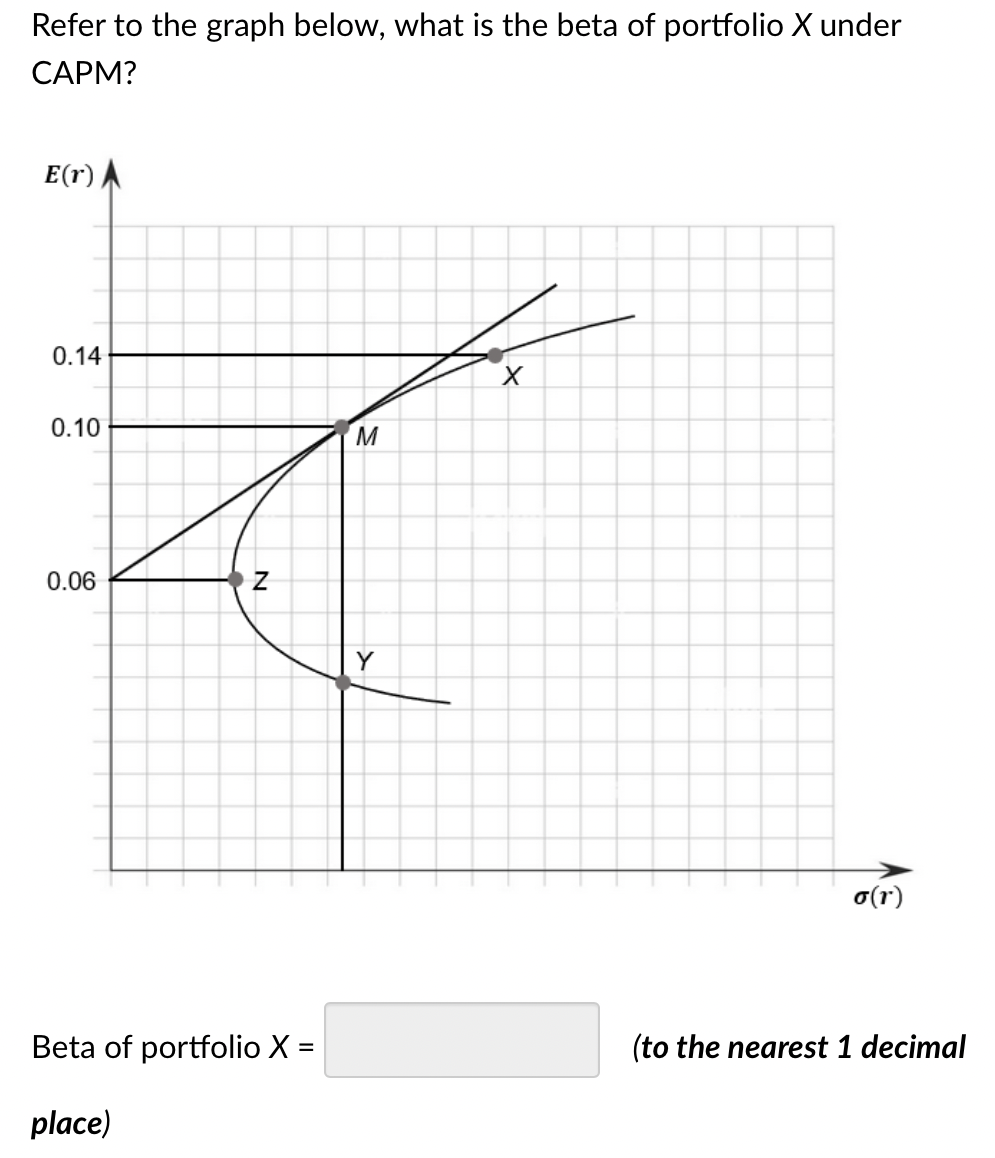

Transcribed Image Text:Refer to the graph below, what is the beta of portfolio X under

CAPM?

E(r) A

0.14

0.10

0.06

N

Beta of portfolio X =

place)

M

X

o(r)

(to the nearest 1 decimal

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Consider a two-factor Arbitrage Pricing Theory (APT) model, T; = a; + b1,ifı + b2.i f2 + €i, with the following information Asset i Asset 1 0.07 0.50 0.25 Asset 2 0.15 1.10 0.75 Asset 3 0.20 b1,3 Hi b1i b2i 1.0 and the risk-free rate rp is 0.025. (a) Find the value of b13 to preclude arbitrage opportunity. (b) is an Asset 4 with 4 = 0.13, b14 = 0.8, and b2.4 = 0.4. Explain how you would exploit an arbitrage opportunity if therearrow_forwardExplain in words the following future- value formula: F = P(1 + r)".arrow_forwardInternal Rate of Return is the discount rate that sets NPV to 0. True or false?arrow_forward

- Compute the VaR(95%) and ES(95%) of the portfolio managed by Absolute Asset Management if its returns, r, follow the distribution specified below: = 1 10 - |r 100| – 10arrow_forwardIf you plot the relationship between portfolio expected return and portfolio beta, what is the slope of the line that results? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) | Slope of the line %arrow_forwardBhagiarrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Y Z Market Risk-free Rp 16.00% бр 32.00% 15.00 27.00 7.30 17.00 11.30 5.80 22.00 0 Bp 1.90 1.25 0.75 1.00 0 Assume that the tracking error of Portfolio X is 13.40 percent. What is the information ratio for Portfolio X? Note: A negative value should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to 4 decimal places. Information ratioarrow_forward2. Suppose that you have a riskfree asset and N risky assets for investment. The rate of return on the riskfree asset is r,, while the (Nx1) vector of the rate of return on the N risky assets is r, which is multivariate normal, i.e., r N(u, E). Your utility function for a portfolio that consists of the riskfree asset and the N risky asset is u(r,)=r,-=o, 2 Suppose that the sum of investment proportions on the riskfree and risky assets is one. Answer the following question. A. What is your optimal investment proportion in the risky assets? How is your investment on the riskfree asset affected by different values of 2? B. Suppose that there is only one risky asset i. Show the effects of the Sharpe ratio (4,/0, ) on the investment proportion in the risky asset.arrow_forwardIt measures the sensitivity of the return of a security to changes in the return of a common index taken to be a proxy of the market portfolio. A. alpha B. sharpe index C. treynor index D. Betaarrow_forwardarrow_back_iosSEE MORE QUESTIONSarrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education