Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

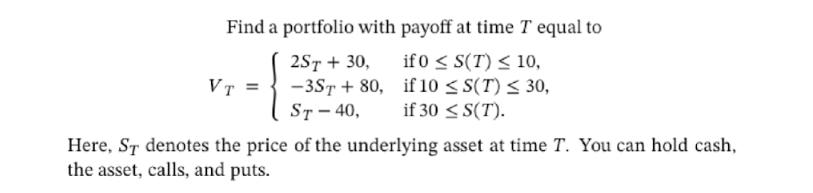

Transcribed Image Text:Find a portfolio with payoff at time T equal to

if 0 ≤ S(T) ≤ 10,

if 10 ≤S(T) ≤ 30,

if 30 ≤S(T).

VT =

2ST + 30,

-3ST+80,

ST-40,

Here, ST denotes the price of the underlying asset at time T. You can hold cash,

the asset, calls, and puts.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Consider the following portfolio choice problem. The investor has initial wealth w and utility u(x)=. There is a safe asset (such as a US government bond) that has net real return of zero. There is also a risky asset with a random net return that has only two possible returns, R₁ with probability 1-q and Ro with probability q. We assume R₁ 0. Let A be the amount invested in the risky asset, so that w - A is invested in the safe asset. 1) Does the investor put more or less of his portfolio into the risky asset as his wealth increases?arrow_forwardThe possible returns of a security I and research returns under three possible states are as follows. Probability % market % security 0.2 15 10 0.5 13 16 0.3 25 30 The risk free rate is 9%, determine the required rate of return of security I and sate whether it is correctly valued. 12-marks] 20 Ri= E(R) XWarrow_forwardA forward contract has an underlying asset which, in Cox-RossRubenstein notation, has S=22,u=1.2 and d=0.9. This forward contract matures in one time step and the return over this time step is R=1.02. Assuming the forward price is calculated rationally, what is the value of the forward at node (1,1)? (Give your answer as a positive number.)arrow_forward

- Bhagiarrow_forwardPortfolio Suppose rA ~ N (0.05, 0.01), rB ~ N (0.1, 0.04) with pA,B = 0.2 where rA and rB are CCR’s. a) Suppose you construct a portfolio with 50% for A and 50% for B. Find the variance of the portfolio CCR. b) Find the portfolio expected gross return. c) Find the expected portfolio CCR.arrow_forwardAssume that using the Security Market Line(SML) the required rate of return(RA)on stock A is found to be halfof the required return (RB) on stock B. The risk-free rate (Rf) is one-fourthof the required return on A. Return on market portfolio is denoted by RM. Find the ratioof betaof A(A) tobeta of B(B). Thank you for your help.arrow_forward

- Asset W has an expected return of 13.4 percent and a beta of 1.6. If the risk-free rate is 5.0 percent, complete the following table for portfolios of Asset W and a risk-free asset. (Do not round intermediate calculations and enter your expected return answers as a percent rounded to 2 decimal places, e.g., 32.16. Round your beta answers to 3 decimal places, e.g., 32.161.) Asset W has an expected return of 13.4 percent and a beta of 1.6. If the risk-free rate is 5.0 percent, complete the following table for portfolios of Asset W and a risk-free asset. (Do not round intermediate calculations and enter your expected return answers as a percent rounded to 2 decimal places, e.g., 32.16. Round your beta answers to 3 decimal places, e.g., 32.161.)arrow_forwardFind the weights of the two pure factor portfolios constructed from the following three securities: r1 = .06 + 2F¡ + 2F, r2 = .05 + 3F, + IF, r3 = .04 + 3F, + OF, Then write out the factor equations for the two pure factor portfolios, and determine their risk premiums. Assume a risk-free rate that is implied by the factor equations and no arbitrage.arrow_forwardThe portfolio with the highest Sharpe Ratio is I. The minimum-variance point on the efficient frontier II. The tangency point of the capital market line and the efficient frontier III. The maximum-return point on the efficient frontier IV. The line with the steepest slope that connects the risk-free rate to the efficient frontier Select one: a. II and IV only b. I and IV only c. III and IV only d. Only IV e. I and II onlyarrow_forward

- Consider the following graph. According to Markowitz’ portfolio theory, which point on the graph represents optimal portfolio? C A B Darrow_forwardAssume a security follows a geometric Brownian motion with volatility parameter = 0.2. Assume the initial price of the security is 21 and the interest rate is 0. It is known that the price of a down-and-in barrier option and a down-and-out barrier option with strike price 19 and expiration 30 days have equal risk-neutral prices. Compute this common risk-neutral price.arrow_forward4. Valuation of a Derivative Consider a derivative on a stock with the time to expiration T and the following payoff: 0 K₁ 0 if ST K₁. What is the present value of the derivative? Provide an analytic expression of the price using N(), the cumulative probability distribution function of a standard normal random variable.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education