FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

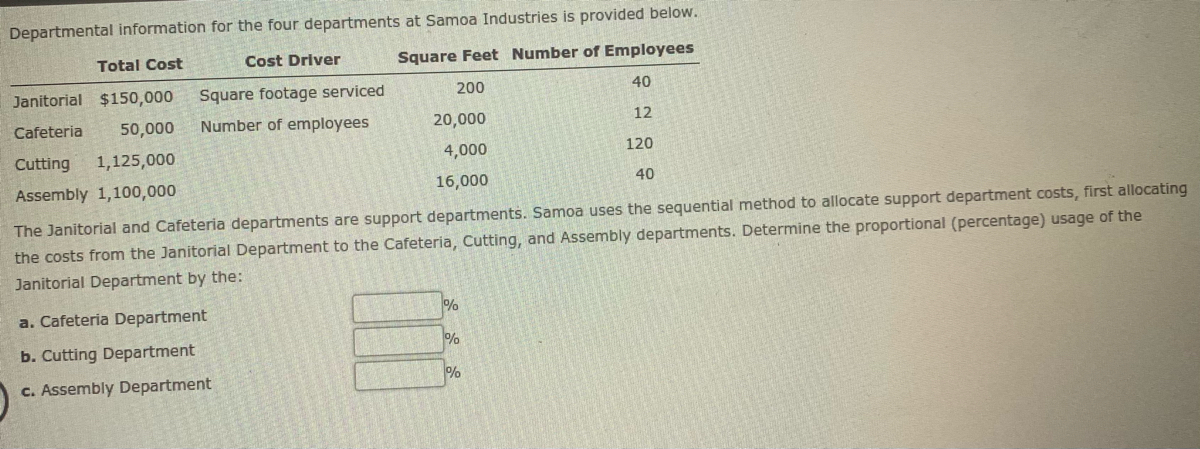

Transcribed Image Text:Departmental information for the four departments at Samoa Industries is provided below.

Total Cost

Cost Driver

Square Feet Number of Employees

Janitorial $150,000

Square footage serviced

200

40

Cafeteria

50,000

Number of employees

20,000

12

Cutting

1,125,000

4,000

120

Assembly 1,100,000

16,000

40

The Janitorial and Cafeteria departments are support departments. Samoa uses the sequential method to allocate support department costs, first allocating

the costs from the Janitorial Department to the Cafeteria, Cutting, and Assembly departments. Determine the proportional (percentage) usage of the

Janitorial Department by the:

a. Cafeteria Department

%

b. Cutting Department

%

c. Assembly Department

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Using the sequential method, Pone Hill Company allocates Janitorial Department costs based on square footage serviced. It allocates Cafeteria Department costs based on the number of employees served. It has determined to allocate Janitorial costs before Cafeteria costs. It has the following information about its two service departments and two production departments, Cutting and Assembly: Line Item Description Costs Square Feet Number ofEmployees Janitorial Department $450,000 100 20 Cafeteria Department 200,000 10,000 10 Cutting Department 1,500,000 2,000 60 Assembly Department 3,000,000 8,000 20 The percentage (proportional) usage of the Cafeteria Department by the Assembly Department is a. 22% b. 18% c. 75% d. 25%arrow_forwardUsing the direct method, Pone Hill Company allocates Janitorial Department costs based on square footage serviced. It allocates Cafeteria Department costs based on the number of employees served. It has the following information about its two service departments and two production departments, Cutting and Assembly: Number of Square Feet Employees Janitorial Department 100 20 Cafeteria Department 10,000 10 Cutting Department 2,000 60 Assembly Department 8,000 20 The percentage (proportional) usage of the Janitorial Department by the Cutting Department is Oa. 10% Ob. 80% Oc. 9.9% Od. 20%arrow_forwardKia Corporation has two departments, A and B. Central costs could be allocated to the two departments in various ways. Square footage of department A and B 6,000 and 18,000 square feet respectively, Number of employees of department A and B 1,500 and 500 respectively, and sales of department A and B $400,000 and $2,000,000 respectively. If total processing costs of $96,000 are allocated on the basis of number of employees, the amount allocated to Department B would be: a. $24,000 b. $28,800 c. $16,000 d. $67,200arrow_forward

- The following departmental information is for the four departments at Samoa Industries. Departmental Total Cost Cost Driver Square Feet Number of Employees Janitorial $150,000 Square footage serviced 200 40 Cafeteria 50,000 Number of employees 20,000 12 Cutting 1,125,000 4,000 120 Assembly 1,100,000 16,000 40 The Janitorial and Cafeteria departments are support departments. Samoa uses the sequential method to allocate support department costs, first allocating the costs from the Janitorial Department to the Cafeteria, Cutting, and Assembly departments. Question Content Area 1. Determine the dollar amount of the Janitorial Department costs to be allocated to the (a) Cafeteria, (b) Cutting, and (c) Assembly departments. Department Amount a. Cafeteria Department fill in the blank 1 of 3$ b. Cutting Department fill in the blank 2 of 3$ c. Assembly Department fill in the blank 3 of 3$…arrow_forwardFounder Consulting Corporation has its headquarters in Memphis and operates from three branch offices in Nashville, Atlanta, and Louisville. Two of the company's activity cost pools are Administrative Service and Development Service. These costs are allocated to the three branch offices using an activity-based costing system. Information for next year follows: Activity Cost Pool Activity Measure Estimated Cost Administrative service % of time devoted to branch $ 1,680,000 Development service Computer time $ 630,000 Estimated branch data for next year is as follows: Time to branch Computer time Nashville 70 % 1,600,000 minutes Atlanta 20 % 1,200,000 minutes Louisville 10 % 400,000 minutes Total 100 % 3,200,000 minutes How much of the headquarters cost allocation should Nashville expect to receive next year?arrow_forwardRiverbed Manufacturing has five activity cost pools and two products (a budget tape vacuum and a deluxe tape vacuum). Information is presented below: Activity Cost Pools Ordering and Receiving Machine Setup Machining Assembly Inspection Budget $ Cost Driver Orders Setups Machine hours Deluxe $ Parts Inspections Overhead cost per unit Est. Overhead $144,000 311,400 1,023,000 1,624,000 314,000 per unit Est. Use of Cost Drivers Budget per unit 600 500 150,000 1.200,000 550 Deluxe 400 Compute the overhead cost per unit for each product. Production is 700.000 units of Budget and 200.000 units of Deluxe. (Round per machine hour and per part values to 3 decimal places, eg 52.711. Round overhead cost per unit to 2 decimal places, e.g. 12.25 and cost assigned to 0 decimal places, eg. 2,500.) 400 100,000 800,000 450arrow_forward

- Support department cost allocation-direct method Becker Tabletops has two support departments (Janitorial and Cafeteria) and two production departments (Cutting and Assembly). Relevant details for these departments are as follows: Support Department Janitorial Department Cafeteria Department Cost Driver Square footage to be serviced Number of employees Janitorial Department $320,000 Janitorial Department cost allocation Cafeteria Department cost allocation Cafeteria Department $170,000 4,500 3 44 10 Department costs Square feet Number of employees Allocate the support department costs to the production departments using the direct method. Cutting Department $ Cutting Department $1,510,000 $ 700 27 Assembly Department $680,000 6,300 3 Assembly Departmentarrow_forwardDepartmental information for the four departments at Samoa Industries is provided below. Total Cost Cost Driver Square Feet Number of Employees Janitorial $150,000 Square footage serviced 200 40 Cafeteria 50,000 Number of employees 20,000 12 Cutting 1,125,000 4,000 120 Assembly 1,100,000 16,000 40 The Janitorial and Cafeteria departments are support departments. Determine the dollar amount of the Janitorial Department costs to be allocated to the (a) Cutting and (b) Assembly departments using the direct method. a. Cutting Department b. Assembly Departmentarrow_forwardSequential method?arrow_forward

- Using the sequential method, Pone Hill Company allocates Janitorial Department costs based on square footage serviced. It allocates Cafeteria Department costs based on the number of employees served. It has determined to allocate Janitorial costs before Cafeteria costs. It has the following information about its two service departments and two production departments, Cutting and Assembly: Line Item Description Costs Square Feet Number ofEmployees Janitorial Department $450,000 100 20 Cafeteria Department 200,000 10,000 10 Cutting Department 1,500,000 2,000 60 Assembly Department 3,000,000 8,000 20 The percentage (proportional) usage of the Janitorial Department by the Cutting Department is a. 80% b. 9% c. 10% d. 20%arrow_forwardPremium Company provides the following ABC costing information: Activities Costs Account inquiry $200,000 Account billing $140,000 Activity-cost drivers 25,000 Account verification accounts $75,000 Total costs 4,000,000 lines Correspondence letters 10,000 hours 40,000 accounts Account billing lines 250,000 lines Department B Account inquiry hours hours Select one: 4,000 letters The above activities are used by Departments A and B as follows: 4,000 hours Account verification accounts accounts 8,000 accounts Correspondence letters a. $8,750 b. $8,500 c. $8,250 d. $8,540 Total 1,600 letters $440,000 Department 2,500 10,000 400,000 lines letters How much of the account billing cost will be assigned to Department B 1,200arrow_forwardTenet Engineering, Incorporated operates two user divisions as separate cost objects. To determine the costs of each division, the company allocates common costs to the divisions. During the past month, the following common costs were incurred: Computer services (85% fixed) Building occupancy Personnel costs Total common costs $ 268,000 658,000 108,000 $ 1,034,000 The following information is available concerning various activity measures and service usages by each of the divisions: Area occupied (square feet) Payroll Computer time (hours) Computer storage (megabytes) Equipment value Operating profit (pre-allocations) Division A 25, 200 $ 453,000 320 5,400 $ 296,000 $ 735,000 Division B 50,400 $ 253,000 340 0 $ 346,000 $ 675,000 If common computer service costs are allocated using computer time as the allocation basis, what is the computer cost allocated to Division B? Note: Do not round intermediate calculations.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education