ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

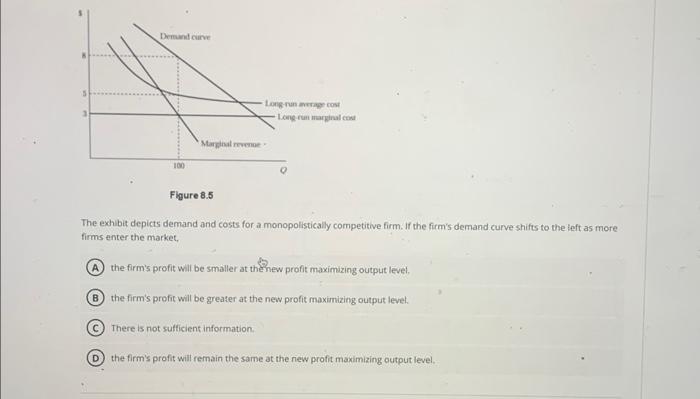

Transcribed Image Text:3

Demand curve

100

Long run average cost

Marginal revenue-

There is not sufficient information.

Long-run marginal cost

Figure 8.5

The exhibit depicts demand and costs for a monopolistically competitive firm. If the firm's demand curve shifts to the left as more

firms enter the market,

A the firm's profit will be smaller at the new profit maximizing output level.

B the firm's profit will be greater at the new profit maximizing output level.

(D) the firm's profit will remain the same at the new profit maximizing output level.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps

Knowledge Booster

Similar questions

- The accompanying graph depicts average total cost (ATC) marginal cost (MC), marginal revenue (M), and demand (D) 50 facing a monopolistically competitive firm MC 45 Place point A at the firm's profit maximizing price and quantity 40 35 What is the firm's total cost? ATC 30 25 total cost: 20 15 What is the firm's total revenue? 10 5 total revenue: $ MR 0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95100 Quantity What is the firm's total profit? profit: $ Price and Cost ($)arrow_forwardQ. 2arrow_forwardWataDine is one of a city’s many restaurants that serve lunch and dinner in a monopolistically competitive market. Assume WataDine, as a typical restaurant in the city, is currently producing the profit-maximizing output level, and earns positive short-run economic profit. (a) How is monopolistic competition similar to each of the following market structures? (i) Perfect competition (ii) Monopoly (b) WataDine is currently earning short-run economic profits. Draw a correctly labeled graph for WataDine in short-run equilibrium and show each of the following. (i) The profit-maximizing quantity, labeled QM (ii) The profit-maximizing price, labeled PM (c) Given that WataDine is currently earning short-run economic profits, what will happen to each of the following in the long run? (i) WataDine's economic profit. Explain. (ii) WataDine's demand curve for its restaurant meals. (d) Assume WataDine is in long-run equilibrium. (i) Is WataDine taking advantage of its economies of scale? Explain.…arrow_forward

- True/False I need help with the last three mostarrow_forwarddo fast.arrow_forwardQuestion 7 As competitors enter a monopolistically competitive industry, the incumbent firms' demand curves... Group of answer choices Shift to the left and become less elastic Shift to the right and become less elastic Shift to the left and become more elastic Shift to the right and become more elasticarrow_forward

- botharrow_forwardA firm in a monopolistically competitive market has a monopoly power because: O There are very few other sellers in the market. There are many firms selling similar products. The firm is not concerned with entry of new firms. The firm's product is differentiated. ◄ Previous MAY 4 Next Not saved Submit tvarrow_forwardPTICE and COST $40 30 23 20 10 MC ATC ATC MR AR=D 150 200 Quantity per day 0:13 Question 11 (10 points) (Exhibit: Profit Maximization for a Firm in Monopolistic Competition) Suppose that an innovation reduces a firm's fixed costs and reduces cost from ATC to ATC' Before the innovation reduced the cost, the firm's maximum economic profit was: $0. $30. $750. $4,500.arrow_forward

- (Figure: The Market for Designer Boots in Monopolistic Competition IV) Use Figure: The Market for Designer Boots in Monopolistic Competition. A positive economic profit will be earned if the profit-maximizing price is in panel Price, cost XXX G; (A) H; (B) (a) O I; (C) O F; (A) ATC Quantity (per period) Price, (b) cost ATC Quantity (per period) Price, (c) cost ATC Quantity (per period)arrow_forwardQuestion 5 The diagram below illustrates a firm under monopolistic competition: Label the curves Curve I, Curve II, Curve III, Curve IV. Graphically identify profit maximizing output and price Explain how the amount of profit is defined at the maximum-profit output.arrow_forwardStudy Tools ins ess Tips ss Tips PRICE (Dellars per engine) 288 RSS #RR 100 50 30 20 10 MO 0 0 10 ATC MR Demand 20 30 40 50 70 DO 90 QUANTITY (Thousands of engines) 100 Mon Comp Outcome Min Unt Cost Decause this market is a monopolistically competitive market, you can tell that it is in long-run equilibrum by the fact that optimal quantity. Furthermore, a monopolistically competitive firm's average total cost in long-run equilibrium is average total cost. at the the minimumarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education