ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

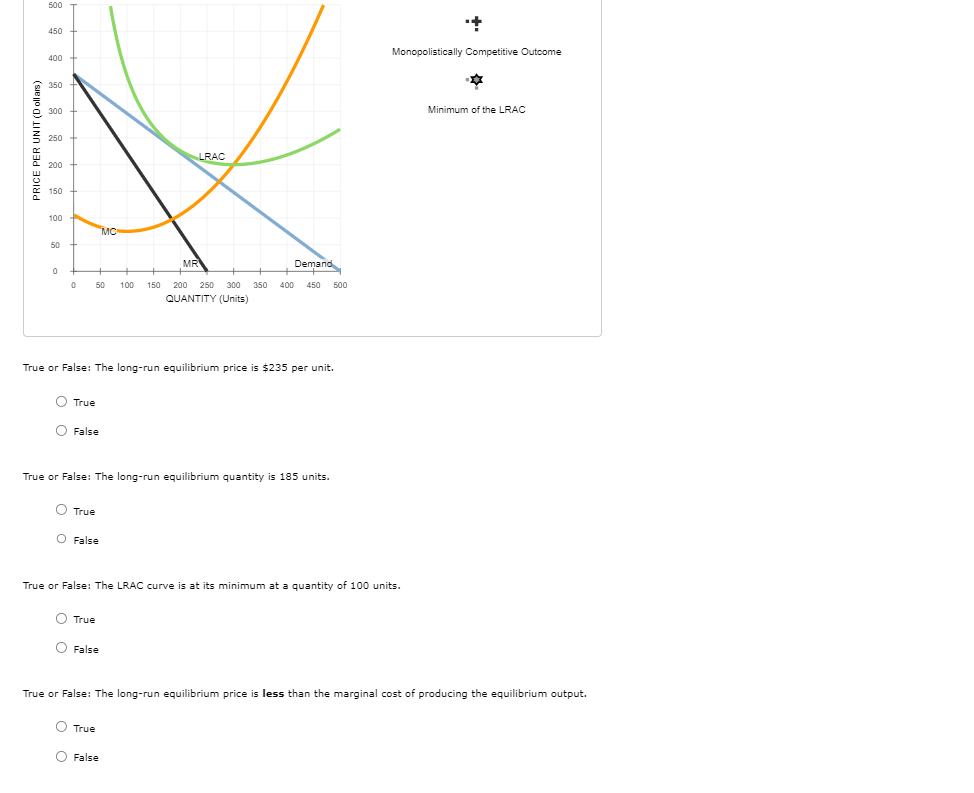

Transcribed Image Text:PRICE PER UNIT (Dollars)

500

450

400

350

300

250

LRAC

200

150

100

MC

50

MR

Demand

0

0

50 100 150

200 250 300 350 400 450 500

QUANTITY (Units)

True or False: The long-run equilibrium price is $235 per unit.

True

False

True or False: The long-run equilibrium quantity is 185 units.

True

False

True or False: The LRAC curve is at its minimum at a quantity of 100 units.

True

False

Monopolistically Competitive Outcome

Minimum of the LRAC

True or False: The long-run equilibrium price is less than the marginal cost of producing the equilibrium output.

True

False

Transcribed Image Text:3. Study Questions and Problems #3

The following graph represents a monopolistically competitive firm in long-run equilibrium.

Place the black point (cross sign) on the graph to indicate the short-run profit-maximizing price and quantity for this monopolistically competitive

company. Next, place the grey star on the graph to indicate the point where the LRAC reaches a minimum.

PRICE PER UNIT (Dollars)

500

450

400

350

300

250

200

150

100

50

MC

0

+

0

50

100

LRAC

MR

Demand

150 200 250 300 350 400 450 500

QUANTITY (Units)

True or False: The long-run equilibrium price is $235 per unit.

True

False

True or False: The long-run equilibrium quantity is 185 units.

True

O False

True or False: The LRAC curve is at its minimum at a quantity of 100 units.

Monopolistically Competitive Outcome

Minimum of the LRAC

?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Recall that in perfect competition a firm's demand curve is a horizontal line drawn at the market price level and that P=MR. With this in mind, based on the figure below, if we assume that the firm chooses the level of output that maximizes profit, what is total revenue at that output level? Price (P) 36 32 MC1 28 24 ATC 20 Dr AVC1 16 12 4 2 4 6 8 10 12 14 16 18 Quantity (Q) Select one: a. $264 b. $200 c. $220 d. $240arrow_forwardDemand Schedule Assume MC = 0 Price Quantity $24 0 $22 1 $20 2 $18 3 $16 4 $14 5 $12 6 $10 7 $8 8 $6 9 $4 10 $2 11 $0 12 1. If the market is perfectly competitive, what will the market equilibrium price and quantity be in the long-term? Explain how you arrived at that answer. 2. If the market is a duopoly and the firms collude to maximize joint profits, what will market price and quantity be? Explain how you arrived at that answer. 3. If the market is a duopoly and the firms collude to maximize joint profits, what is each firm's total revenue if the firm split the market equally? Explain how you calculated that answer.arrow_forwardOnly typed answerarrow_forward

- Please help im beggingarrow_forwardHow would you characterize the nature of competition among small food companies? Are there submarkets with distinct competitive pressures? Are there important substitutes that constrain pricing? Given these competitive issues, how can an organic frozen foods producer be profitable?arrow_forwardQuestion 2 pleasearrow_forward

- PRICE Graph (a) MR QUANTITY MC ATC D PRICE Graph (b) MR QUANTITY Figure 17-4 MC ATC D Graph (c) MR QUANTITY MC ATC D Graph (d) QUANTITY Refer to Figure 16-4. Which of the graphs depicts a short-run equilibrium that will encourage the entry of other firms into a monopolistically competitive industry? O a. Graph (b) O b. Graph (d) O c. Graph (c) O d. Graph (a) MC ATC Darrow_forwardRefer to Figure K.. If there were four identical firms in this competitive industry, which of the following price-quantity combinations would be on the market supply curve? Point A B C D (A) A and C only B) Bonly C) B and D only D) A only Price (Dollars) 4 4 Quantity (Units) 16 32 32 6 6 8 64 64arrow_forwardsolve botharrow_forward

- Dana is a dot-com entrepreneur who has established a Web site at which people can design and buy awatch. Dana pays $200 a month for a Web server and Internet connection. The watches that customers design are made to order by another firm, and Dana pays this firm $60 a watch. Dana has no other costs. The table shows the demand schedule for Dana's watches. What is Dana's profit-maximizing output, price, and economic profit? Dana's profit-maximizing output is Dana's profit-maximizing price is $ Dana's economic profit is $ a month. watches a month. a watch. Price (dollars per watch) 100 80 60 40 20 0 Quantity (watches per month) 0 20 40 60 80 100arrow_forwardCosts and revenue per case 50% a $14 $12 $22 $16 $13 Question 6 Costs and revenue 22 24 30 30 @ 300 The perfectly competitive price would be: MR 22 24 30 3 ATC Demand Quantly (cases) ATC Demand Quantity In the above graph, the firm would earn: $0 in economic profit and break even $44 economic profit $88 economic profit $22 economic loss $44 economic lossarrow_forwardQuestion 21 A firm is a price taker only when the market is perfectly competitive. only when the market is perfectly competitive or monopolistic. Oonly when the market is perfectly competitive or monopolistically competitive. when the market is perfectly competitive, monopolistically competitive, or monopolistic. Question 22arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education