Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the market's average return was 14%. Performance is measured using an index model regression on excess returns. Index model regression estimates R-square Residual standard deviation, o(e) Standard deviation of excess returns i. Alpha ii. Information ratio iii. Sharpe ratio iv. Treynor measure a. Calculate the following statistics for each stock: (Round your answers to 4 decimal places.) Stock A % Stock A 1% + 1.2 (rm -rf) 0.635 11.3% 22.6% % Stock B % % Stock B 2% +0.8( rm -rf) 0.466 20.1% 26.9% b. Which stock is the best choice under the following circumstances? i. This is the only risky asset to be held by the investor. ii. This stock will be mixed with the rest of the investor's portfolio, currently composed solely of holdings in the market-index fund. ii. This is one of many stocks that the investor is analyzing to form an actively managed stock portfolio.

Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the market's average return was 14%. Performance is measured using an index model regression on excess returns. Index model regression estimates R-square Residual standard deviation, o(e) Standard deviation of excess returns i. Alpha ii. Information ratio iii. Sharpe ratio iv. Treynor measure a. Calculate the following statistics for each stock: (Round your answers to 4 decimal places.) Stock A % Stock A 1% + 1.2 (rm -rf) 0.635 11.3% 22.6% % Stock B % % Stock B 2% +0.8( rm -rf) 0.466 20.1% 26.9% b. Which stock is the best choice under the following circumstances? i. This is the only risky asset to be held by the investor. ii. This stock will be mixed with the rest of the investor's portfolio, currently composed solely of holdings in the market-index fund. ii. This is one of many stocks that the investor is analyzing to form an actively managed stock portfolio.

Financial Management: Theory & Practice

16th Edition

ISBN:9781337909730

Author:Brigham

Publisher:Brigham

Chapter6: Risk And Return

Section: Chapter Questions

Problem 4P: An analyst gathered daily stock returns for Feburary 1 through March 31, calculated the Fama-French...

Related questions

Concept explainers

Risk and return

Before understanding the concept of Risk and Return in Financial Management, understanding the two-concept Risk and return individually is necessary.

Capital Asset Pricing Model

Capital asset pricing model, also known as CAPM, shows the relationship between the expected return of the investment and the market at risk. This concept is basically used particularly in the case of stocks or shares. It is also used across finance for pricing assets that have higher risk identity and for evaluating the expected returns for the assets given the risk of those assets and also the cost of capital.

Question

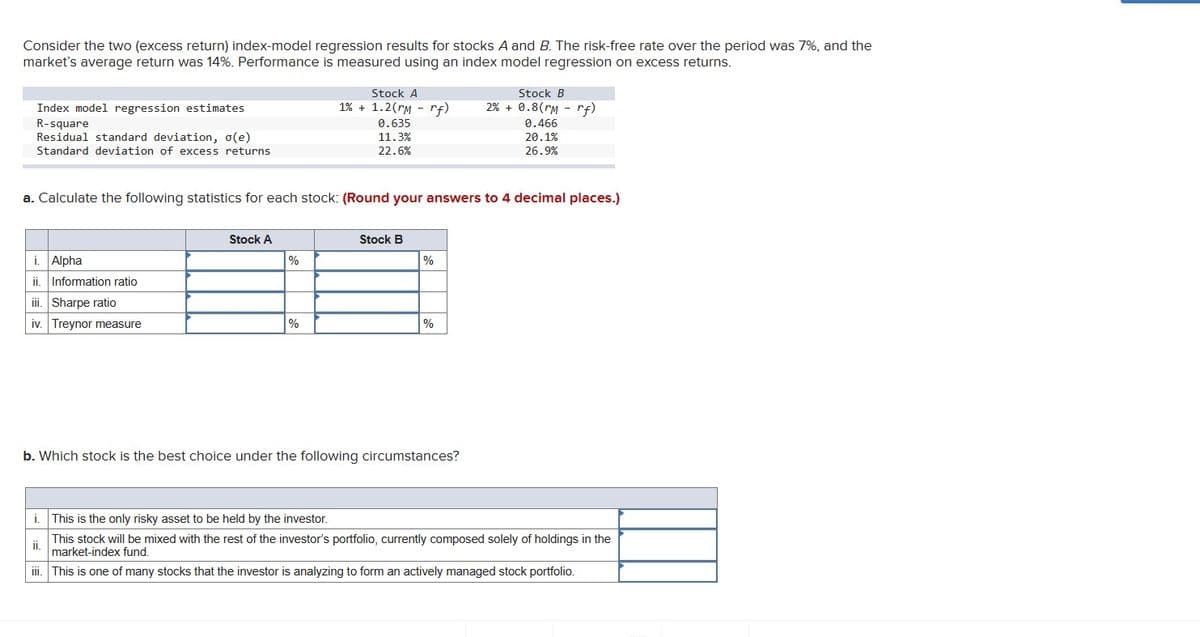

Transcribed Image Text:Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 7%, and the

market's average return was 14%. Performance is measured using an index model regression on excess returns.

Index model regression estimates

R-square

Residual standard deviation, o(e)

Standard deviation of excess returns.

i. Alpha

ii. Information ratio

iii. Sharpe ratio

iv. Treynor measure

Stock A

a. Calculate the following statistics for each stock: (Round your answers to 4 decimal places.)

%

Stock A

1% +1.2(rm rf)

%

0.635

11.3%

22.6%

Stock B

%

%

Stock B

2% +0.8( rm -rf)

b. Which stock is the best choice under the following circumstances?

0.466

20.1%

26.9%

i. This is the only risky asset to be held by the investor.

ii.

This stock will be mixed with the rest of the investor's portfolio, currently composed solely of holdings in the

market-index fund.

iii. This is one of many stocks that the investor is analyzing to form an actively managed stock portfolio.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 5 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning