Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

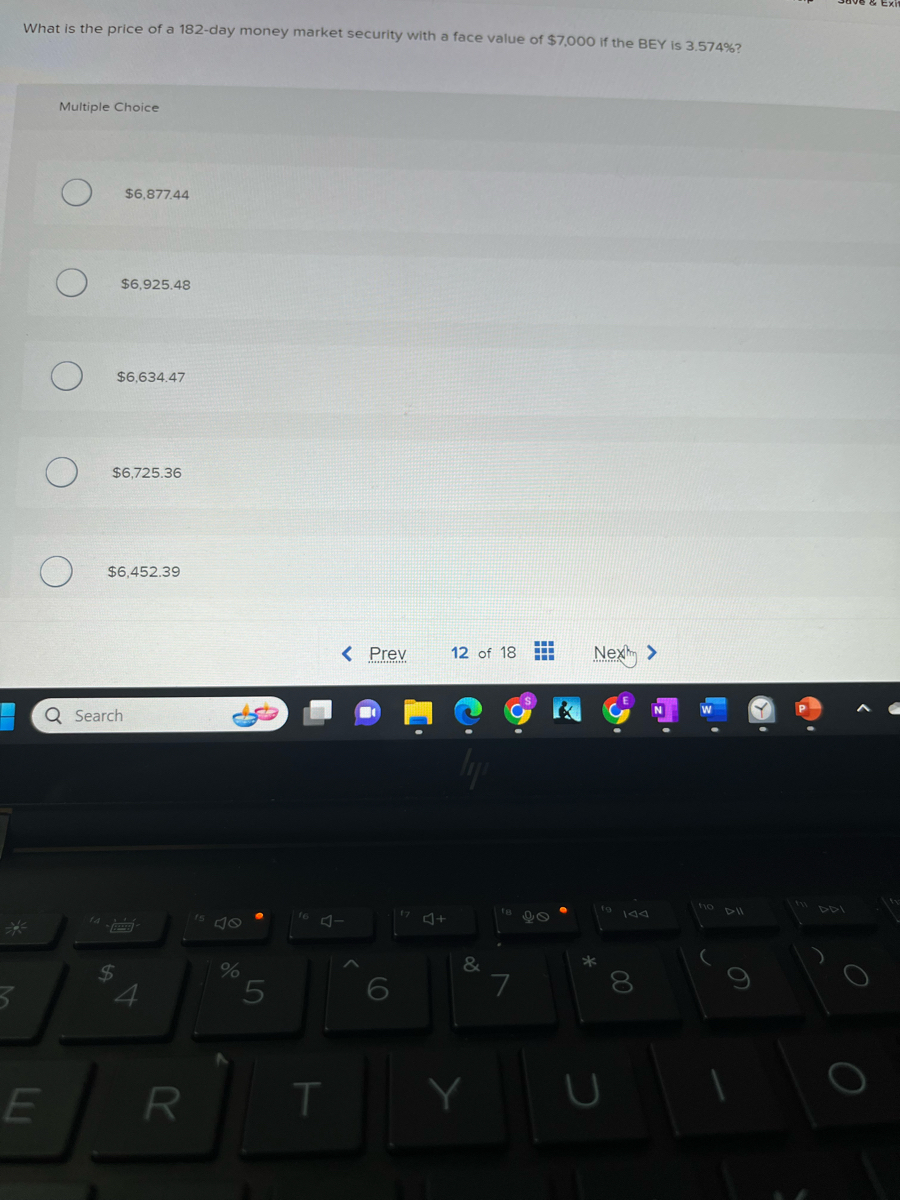

Transcribed Image Text:What is the price of a 182-day money market security with a face value of $7,000 if the BEY is 3.574%?

*

3

Multiple Choice

E

$6,877.44

$6,925.48

$6,634.47

$6,725.36

Q Search

$

$6,452.39

R

%

5

T

< Prev

4+

12 of 18 T

lyjs

&

98

Next >

*

U

00

O

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Give typing answer with explanation and conclusion 5. A European call option on Home Depot stock has a strike price of $160 and expires in 0.9 years. Home Depot stock has a current market price of $165.99 and the risk-free rate is 4%. What must be the minimum price of the option?arrow_forwardWhich if the following would you prefer to be buying based on yield to maturity (assume n = 25)? A) A $10,000 par value security with a 9% coupon rate selling for $9,000 B) A $15,000 par value security with a 7% coupon rate selling for $15,700 C) A $20,000 par value security with a 9% coupon rate selling for $20,500. D) A $25,000 par value security with a 7% coupon rate selling for $25,500.arrow_forwardWhat is the price of an American CALL option that is expected to pay a dividend of $2 in three months with the following parameters? s0 = $40d = $2 in 3 monthsk = $43 r = 10%sigma = 20%T = 0.5 years (required precision 0.01 +/- 0.01)arrow_forward

- The speculator buys one put option at a strike price of $70/barrel and expiry date October 2021 for a premium of $1.20/barrel. Consider the following expected payoff chart for buying a put option. What are the names of point A and B? What is the exact value of A? What is the exact value B?arrow_forwardMasukharrow_forwardToday's price of Microsoft (MSFT) is $150 per share. A retail investor purchases an at-the-money European put option on MSFT with a maturity of one year. She pays a premium of $14.11. The c.c. risk-free interest rate is one percent. What is the potentiality value of the option? Round your answer to three decimal places.arrow_forward

- Find the PUT option price using the following data: S0 = $215 X = $220 Risk-free Int Rate = 5% Two possibilities of ST at expiration: $200 or $250 Expiration: 2 years from todayarrow_forward5. Suppose you buy a one-year forward contract at $65. At expiration, the spot price is $73. The risk-free rate is 10 percent. What is the value of the contract at expiration? a. impossible to tell b. $8.00 c. $7.27 d. –$8.00 e. $0.00arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education