ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

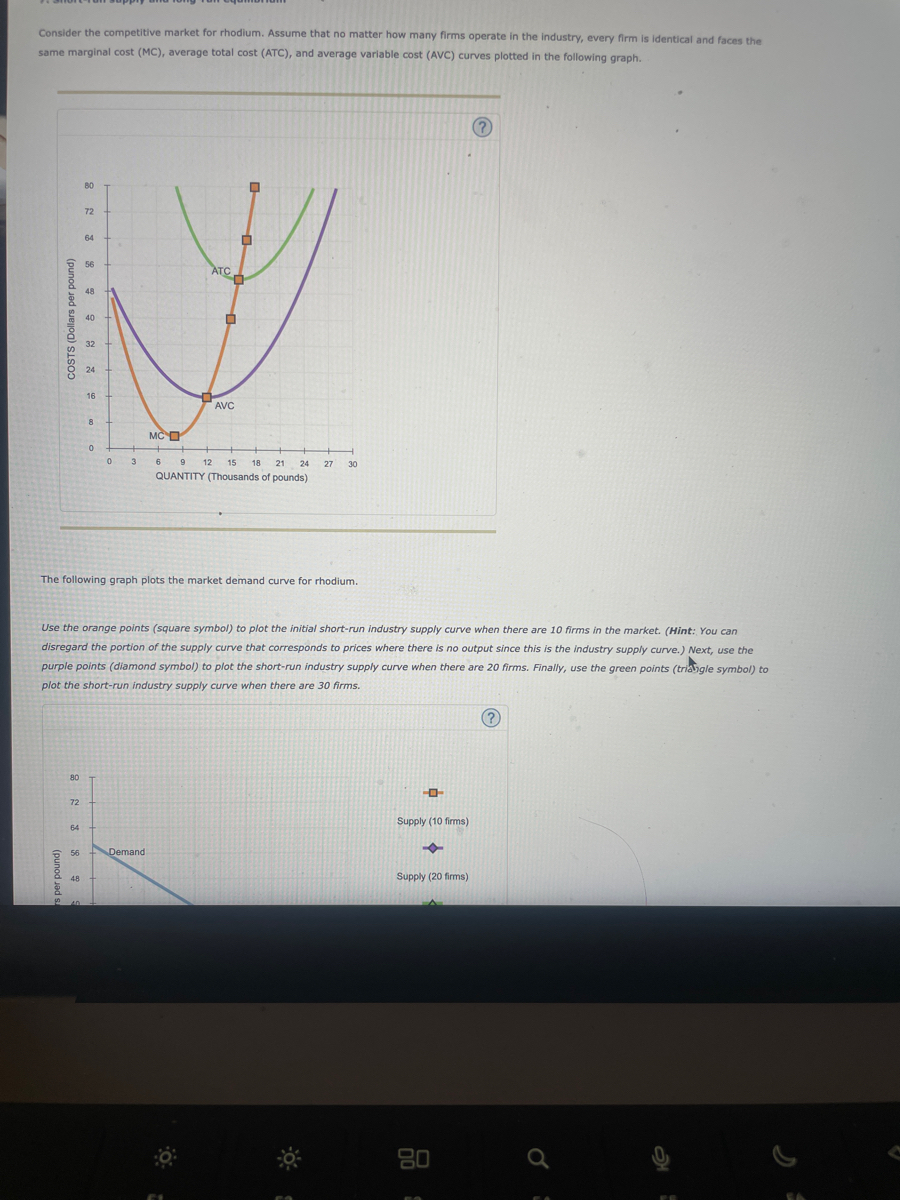

Transcribed Image Text:Consider the competitive market for rhodium. Assume that no matter how many firms operate in the industry, every firm is identical and faces the

same marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves plotted in the following graph.

COSTS (Dollars per pound)

80

2233 22

72

64

56

80

48

72

64

56

48

40

00

32

24

16

0

0

MCD

ATC

Demand

0

AVC

The following graph plots the market demand curve for rhodium.

-0.

☐

3 6 9 12 15 18 21

QUANTITY (Thousands of pounds)

D

Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 10 firms in the market. (Hint: You can

disregard the portion of the supply curve that corresponds to prices where there is no output since this is the industry supply curve.) Next, use the

purple points (diamond symbol) to plot the short-run industry supply curve when there are 20 firms. Finally, use the green points (triangle symbol) to

plot the short-run industry supply curve when there are 30 firms.

24

27

30

-0-

Supply (10 firms)

Supply (20 firms)

(?

80

Transcribed Image Text:esc

The following graph plots the market demand curve for rhodium.

Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 10 firms in the market. (Hint: You can

disregard the portion of the supply curve that corresponds to prices where there is no output since this is the industry supply curve.) Next, use the

purple points (diamond symbol) to plot the short-run industry supply curve when there are 20 firms. Finally, use the green points (triangle symbol) to

plot the short-run industry supply curve when there are 30 firms.

PRICE (Dollars per pound)

80

72

64

56

48

40

32

24

16

8

0

0

Demand

120

18 21 24 27 30

QUANTITY (Thousands of pounds)

240 360 480 600 720 840 960 1080 1200

QUANTITY (Thousands of pounds)

Because you know that competitive firms earn

$

O True

O False

---

If there were 30 firms in this market, the short-run equilibrium price of rhodium would be $

would

▼ Therefore, in the long run, firms would i

Supply (10 firms)

➜

F1

Supply (20 firms)

F2

A

per pound. From the graph, you can see that this means there will be

Supply (30 firms)

True or False: Assuming implicit costs are positive, each of the firms operating in this industry in the long run earns positive accounting profit.

economic profit in the long run, you know the long-run equilibrium price must be

firms operating in the rhodium industry in long-run equilibrium.

(?

80

per pound. At that price, firms in this industry

the rhodium market.

F3

Q

F4

H

F5

F6

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The following graph plots the marginal cost (MC) curve, average total cost (ATC) curve, and average variable cost (AVC) curve for a firm operating in the competitive market for snapback hats. COSTS (Dollars) 100 100 80 90 80 20 70 70 HD 50 40 30 20 0 11 D 10 O MC Price (Dollars per snapback) 15 15 20 25 55 70 85 201 ATC 0 D AVC O 50 60 70 80 QUANTITY (Thousands of snapbacks) For every price level given in the following table, use the graph to determine the profit-maximizing quantity of snapbacks for the firm. Further, select whether the firm will choose to produce, shut down, or be indifferent between the two in the short run. (Assume that when price exactly equals average variable cost, the firm is indifferent between producing zero snapbacks and the profit-maximizing quantity of snapbacks.) Lastly, determine whether the firm will earn a profit, incur a loss, or break even at each price. □ Quantity (Snapbacks) BO 100 ▼ On the following graph, use the orange points (square symbol) to…arrow_forwardIn competitive markets, there are many small firms with each firm unable to influence the market price. Suppose company ABX operates in the wheat market. The company produces and markets wheats at a Price = $20 per container. The firm’s total costs are given as: TC = 50 +2Q + 3Q2 What is the firm’s demand curve? Show it on a graph and label the axes showing P and Qarrow_forwardThe following diagram shows the market demand for steel. Use the orange points (square symbol) to plot the short-run industry supply curve when there are 20 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output since this is the industry supply curve.) Next, use the purple points (diamond symbol) to plot the short-run industry supply curve when there are 40 firms. Finally, use the green points (triangle symbol) to plot the short-run industry supply curve when there are 60 firms. PRICE (Dollars per ton) 80 72 Supply (20 firms) 64 58 Demand 48 Supply (40 firms) 40 32 2 24 16 8 ° 0 120 240 360 480 600 720 840 960 1080 1200 QUANTITY OF OUTPUT (Thousands of tons) Supply (60 firms) ? If there were 60 firms in this market, the short-run equilibrium price of steel would be $ Therefore, in the long run, firms would Because you know that perfectly competitive firms earn be $ per ton. At that price, firms in this industry…arrow_forward

- 3. Profit maximization using total cost and total revenue curves Suppose Bob runs a small business that manufactures teddy bears. Assume that the market for teddy bears is a competitive market, and the market price is $25 per teddy bear. The following graph shows Bob's total cost curve. Use the blue points (circle symbol) to plot total revenue and the green points (triangle symbol) to plot profit for teddy bears quantities zero through seven (inclusive) that Bob produces. TOTAL COST AND REVENUE (Dollars) 200 175 150 125 100 75 50 25 0 -25 O ☐ ☐ 0 1 2 3 4 5 QUANTITY (Teddy bears) ☐ 6 Total Cost 7 8 O Total Revenue Profit ?arrow_forward2. In the competitive mink oil industry, each fim has the same cost function: C = 10,000 100 + 0.01q. Demand for mink oil is as follows: Q = p2 What will be the long-run equilibrium price and quantity in the market? How many fims are in the industıy?arrow_forwardConsider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the Industry, every firm in the industry is Identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per pound) PRICE (Dollars per por 100 90 80 70 60 50 40 30 20 100 10 50 0 80 70 60 50 40 30 20 10 0 The following diagram shows the market demand for copper. 0 Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output since this is the Industry supply curve.) Next, use the purple points (diamond symbol) to plat the short-run industry supply curve when there are 30 firms. Finally, use the green points (triangle symbol) to plot the short-run Industry supply curve when there are 40 firms. MC D 0 5 10 ATC H AVC D 0 15…arrow_forward

- Suppose Rina runs a small business that manufactures frying pans. Assume that the market for frying pans is a competitive market, and the market price is $20 per frying pan. The following graph shows Rina's total cost curve. On the graph below, use the blue points (circle symbol) to plot total revenue and the green points (triangle symbol) to plot profit for the first seven frying pans that Rina produces, including zero frying pans. TOTAL COST AND REVENUE (Dollars) 200 175 150 125 100 75 50 25 0 -25 □ 0 1 U 2 ■ U 3 4 5 QUANTITY (Frying pans) n 6 Total Cost 7 8 Total Revenue Profit ?arrow_forward7. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) 100 90 80 70 60 50 40 ATC 30 20 10 + MC AVC 0 0 5 10 15 20 25 30 35 40 45 50 QUANTITY OF OUTPUT (Thousands of tons) The following diagram shows the market demand for steel. ⑦? Use the orange points (square symbol) to plot the short-run industry supply curve when there are 20 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output since this is the industry supply curve.) Next, use the purple points (diamond symbol) to plot the short-run industry supply curve when there are 30 firms. Finally, use the green points (triangle symbol) to plot the short-run industry…arrow_forwardThe value = = 30.775 should be used in the cost model to estimate the cost of producing how many widgets? widgets. Round to the nearest widget.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education