FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

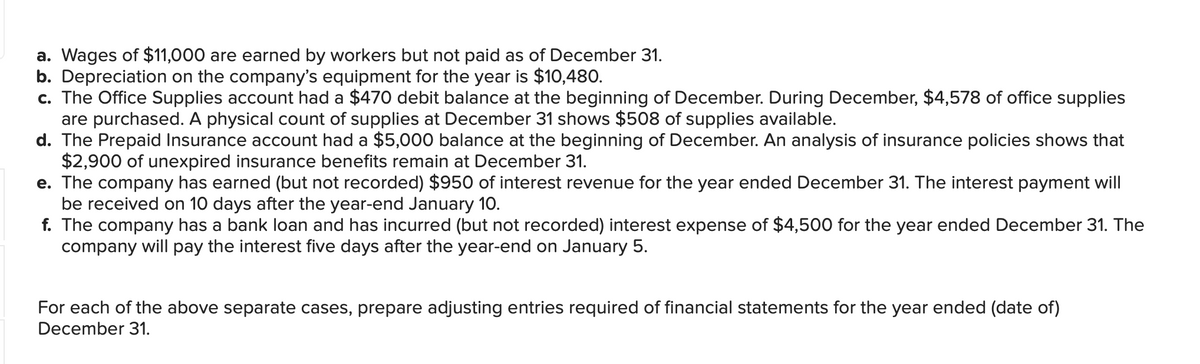

Transcribed Image Text:### Adjusting Entries for Financial Statements

Before preparing the year-end financial statements, companies need to ensure that their accounts reflect all earned revenue and incurred expenses. This process often involves adjusting entries. Below are scenarios and required adjustments:

a. **Accrued Wages**

- Workers have earned wages amounting to $11,000 by December 31, which have not been paid.

b. **Depreciation Expense**

- The annual depreciation on the company’s equipment is $10,480.

c. **Office Supplies Expense**

- The Office Supplies account had a starting balance (debit) of $470. During December, $4,578 worth of supplies were purchased. A physical count at December 31 shows $508 remains.

d. **Prepaid Insurance**

- The Prepaid Insurance account had a $5,000 balance at the start of December. Upon analysis, $2,900 of unexpired insurance benefits remain at year-end.

e. **Accrued Interest Revenue**

- The company has earned interest revenue of $950 for the year ending December 31, which has not been recorded. The payment will be received on January 10.

f. **Accrued Interest Expense**

- The company has a bank loan and has incurred an interest expense of $4,500 for the year ending December 31, which has not been recorded. The payment will occur on January 5.

### Instructions

For each scenario, prepare the necessary adjusting entries to ensure accurate financial statements as of December 31.

Transcribed Image Text:### Journal Entry Worksheet

**Transaction Details:**

- **Description:** Wages of $11,000 are earned by workers but not paid as of December 31.

**Instructions:**

- **Note:** Enter debits before credits.

**Journal Entry Table:**

| Transaction | General Journal | Debit | Credit |

|-------------|------------------|-------|--------|

| a. | | | |

| | | | |

| | | | |

| | | | |

| | | | |

**Buttons:**

- **Record entry**

- **Clear entry**

- **View general journal**

This worksheet is designed to help you record and manage journal entries, specifically for situations where wages have been earned but not yet paid by the end of the accounting period. Remember to enter all debit amounts before credit amounts to ensure accuracy in financial reporting.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Similar questions

- The management of Zigby Manufacturing prepared the following balance sheet for March 31. ZIGBY MANUFACTURING Balance Sheet March 31 Assets Liabilities and Equity Cash $ 104,000 Liabilities Accounts receivable 895,440 Accounts payable $ 522,600 Raw materials inventory 256,100 Loan payable 12,000 Finished goods inventory 846,404 Long-term note payable 1,300,000 $ 1,834,600 Equipment $ 1,560,000 Equity Less: Accumulated depreciation 390,000 1,170,000 Common stock 871,000 Retained earnings 566,344 1,437,344 Total assets $ 3,271,944 Total liabilities and equity $ 3,271,944 To prepare a master budget for April, May, and June, management gathers the following information. Sales for March total 53,300 units. Budgeted sales in units follow: April, 53,300; May, 50,700; June, 52,000; and July, 53,300. The product’s selling price is $24.00 per unit and its total product cost is $19.85 per unit. Raw materials inventory consists…arrow_forwardA company began operations in March with cash and common stock of $36,000. The company made $582,000 in net income in its first month. It performed print jobs for customers and billed these customers $900,000. The company collected half of its receivables by the end of the month. The company had a cost of goods sold of $162,000 paid for in cash and $6,000 inventory left over at the end of the month. The company's employees earned wages but those are not paid until the first of April. This was the company’s only liability. How would I calculate the income statement and balance sheet for the end of March?arrow_forwardMorrison Company Balance Sheet January 1 Assets Cash $ 40,950 Raw materials Work in process Finished goods Prepaid expenses Property, plant, and equipment (net) $ 17,800 6,600 31,800 56, 200 3,350 124,000 $ 224,500 Total assets Liabilities and Stockholders' Equity Accounts payable Retained earnings $ 7,100 217,400 Total liabilities and stockholders' equity $ 224,500 During January the company completed the following transactions: a. Purchased raw materials on account, $75,200. b. Raw materials used in production, $91,500 ($80,200 was direct materials and $11,300 was indirect materials). c. Paid $202.100 of salaries and wages in cash ($108,800 was direct labor, $41,700 was indirect labor, and $51,600 was related to employees responsible for selling and administration). d. Various manufacturing overhead costs incurred (on account) to support production, $43,350. e. Depreciation recorded on property, plant, and equipment, $63,600 (70% related to manufacturing equipment and 30% related to…arrow_forward

- Lawson Manufacturing Company has the following account balances at year end: Office supplies Raw materials Work-in-process $ 4,000 25,000 61,000 Finished goods 109,000 Prepaid insurance 6,000 What amount should Lawson report as inventories in its balance sheet?arrow_forwardWalter Company has the following information for the month of March: $ 17,520 40,450 23,100 Cash balance, March 1 Collections from customers Paid to suppliers Manufacturing overhead Direct labor Selling and administrative expenses Walter pays wages and other cash expenses in the month incurred. Manufacturing overhead includes $1,600 for machinery depreciation, but the amount for selling and administrative expenses is exclusive of depreciation. Additionally, Walter also expects to buy a piece of property for $7.800 during March. Walter can borrow in increments of $1,000 and would like to maintain a minimum cash balance of $10,000. Required: Prepare Walter's cash budget for the month of March. 6,900 8,650 5,000 Beginning Cash Balance Budgeted Cash Receipts Budgeted Cash Payments Preliminary Cash Balance Cash Borrowed Ending cash balance 4arrow_forwardNonearrow_forward

- 2. For each of the transactions for the month below, journalize the necessary entry. The first entry has been completed for you.arrow_forwardUsing the following information. a. Beginning cash balance on March 1, $81,000. b. Cash receipts from sales, $305.000. c. Cash payments for direct materials, $130.000. d. Cash payments for direct labor. $79,000. e. Cash payments for overhead, $38.00. f. Cash payments for sales commissions, $7000 g. Cash payments for interest, $130 (1% of beginning loan balance of $13,000) h. Cash repayment of loan, $13.000. Prepare a cash budget for March for Gado Company. GADO COMPANY Cash Budget March Total cash available Less: Cash payments for Total cash payments $4 Loan activity Loan balance, end of month %24 K Prev earcharrow_forward16. At the end of the year, a company finds that it has under-applied factory overhead by $1,000. What would be the most common accounting treatment in this case? Increase Assets by $1,000 on the Balance Sheet Increase Profit by $1,000 in the Income Statement Increase Liabilities by $1,000 on the Balance Sheet Decrease Cost of Goods Sold by $1,000 in the Income Statement Increase Cost of Goods Sold by $1,000 in the Income Statement.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education