ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

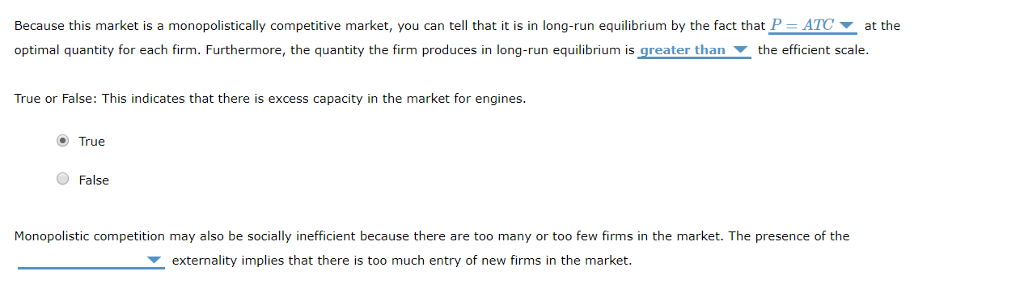

Transcribed Image Text:Because this market is a monopolistically competitive market, you can tell that it is in long-run equilibrium by the fact that P = ATC at the

optimal quantity for each firm. Furthermore, the quantity the firm produces in long-run equilibrium is greater than the efficient scale.

True or False: This indicates that there is excess capacity in the market

True

False

engines.

Monopolistic competition may also be socially inefficient because there are too many or too few firms in the market. The presence of the

externality implies that there is too much entry of new firms in the market.

Transcribed Image Text:4. Is monopolistic competition efficient?

Suppose that a firm produces wooden train engines in a monopolistically competitive market. The following graph shows its demand curve, marginal

revenue (MR) curve, marginal cost (MC) curve, and average total cost (ATC) curve.

Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next,

place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost.

?

PRICE (Dollars per engine)

100

90

80

70

60

50

40

30

20

10

0

MO

0 10

——-—_

20

I

ATC

MR

30 40 50 60 70

QUANTITY (Thousands of engines)

Demand

80

90 100

Mon Comp Outcome

Min Unit Cost

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The graph shows the cost curves, demand curve, and marginal revenue curve of a firm in monopolistic competition. If this firm is maximizing profits, what is the firm's economic profit in millions of dollars? [NOTE: The quantities shown in the graph are in millions. Please enter the number of millions of dollars of economic profit in the statement below.] The firm's economic profit is $ million. 2207 200- 180- 160- 140- 120- 100- 80- 60- 40- 20- Price and cost (dollars per pair) 10+ 0.0 MC MR ATC D 0.5 1.0 1.5 2.0 2.5 Quantity (millions of pairs of Uggs per year) 3.0arrow_forwardIf the firms in a monopolistically competitive market are earning economic profits or losses in the short run, would you expect them to continue doing so in the long run? Explain your answer Is a monopolistically competitive firm productively efficient? How can you tell? Offer one reason why a monopolistically competitive firm might be productively inefficient. Is it allocatively efficient? How can you tell? Offer one reason why a monopolistically competitive firm might be allocatively inefficient. What stops oligopolists from acting together as a monopolist and earning the highest possible level of profits? Offer two obstacles to oligopolists cooperating. Aside from advertising, how can monopolistically competitive firms increase demand for their products? What effect would doing this have on the elasticity of the firm’s perceived demand curve? Explain your answers. Would you expect the kinked demand curve to be more extreme (like a right angle) or less extreme (like a…arrow_forwardIn one paragraph, explain the pricing factor of competitor pricing. Why does what the competitors charge affect pricing? Consider that some companies charge more or less as the competition for the same product.arrow_forward

- With explain this questionarrow_forwardThe accompanying graph depicts average total cost (ATC) marginal cost (MC), marginal revenue (M), and demand (D) 50 facing a monopolistically competitive firm MC 45 Place point A at the firm's profit maximizing price and quantity 40 35 What is the firm's total cost? ATC 30 25 total cost: 20 15 What is the firm's total revenue? 10 5 total revenue: $ MR 0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95100 Quantity What is the firm's total profit? profit: $ Price and Cost ($)arrow_forwardQ. 2arrow_forward

- If Amazon sells dozens of similar types of pencils at slightly different prices, we might assume the pencil market is _________. Select one: a. an oligopoly. b. a monopolistically competitive market. c. a monopoly. d. a perfectly competitive market.arrow_forwardConsider the model with monopolistic competition and full symmetry between the firms (internal returns to scale) in a single integrated market. Now assume that a new technology becomes available that reduces a firm's marginal cost of production by a given amount but requires a larger fixed-cost investment to implement. Suppose that all fırms adopt the new technology. How does this impact the equilibrium number of varieties and the equilibrium price? Show your work. Edit View Insert Format Tools Tablearrow_forwardThe diagram above represents a monopolistically competitive firm. Answer the questions below. Is this firm operating in the short-run or long-run? How do you know? Calculate this firm’s accounting profit. From the diagram, what is the productively efficient output for this firm? From the diagram, economies of scale are maximized at which output level? Explain. From the diagram, what is the allocatively efficient output for this firm? Explain.arrow_forward

- Discuss the long-term effects in a monopolistically competitive market if an existing firm is making profits or losses. Use graphs to help your explanations.arrow_forwardThe graph depicts a monopolistically competitive firm. Assuming the firm's ATC is ATC', the firm's current economic profit (per day) is_____, and its long-run economic profit is _____. Price and cost $40 30 23 20 10 0 $3,000; $0 $1,500; $0 $1,500; $2,500 $4,000; $3,000 MR 150 200 MC ATC ATC AR=D Quantity (per day)arrow_forwardK Suppose the figure to the right represents the market for a particular brand of shampoo, such as L'Oreal, Lancome, or Maybelline. Assume the market is monopolistically competitive. What is the firm's profit-maximizing price and quantity? thousand per bottle. (Enter your The monopolistically competitive firm's profit-maximizing quantity is bottles of shampoo, and its profit-maximizing price is $ responses as integers.) Price and cost (per bottle) ♫ 3.00- MC 2.80- ATC 2.60- 2.40- 2.20- 2.00- 1.80- 1.60- 1.40- 1.20- 1.00- 0.80- 0.60- 0.40- 0.20- 0.00+ 0 MR 2 4 6 8 10 12 14 16 18 20 22 24 Quantity (shampoo bottles in thousands)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education