ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

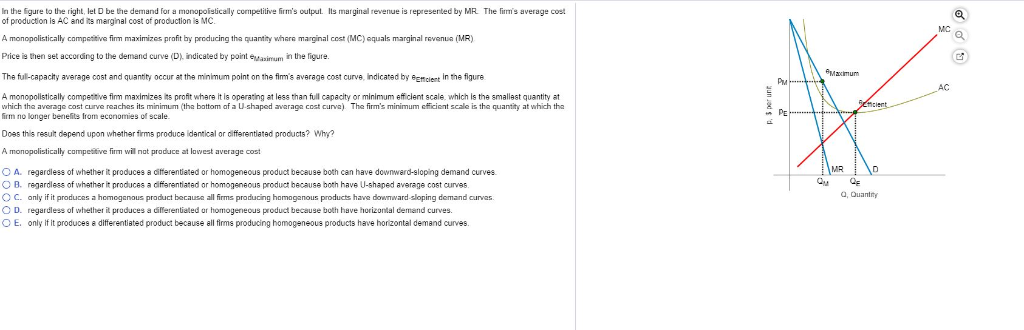

Transcribed Image Text:In the figure to the right, let D be the demand for a monopolistically competitive firm's output. Its marginal revenue is represented by MR. The firm's average cost

of production is AC and its marginal cost of production is MC.

A monopolistically competitive firm maximizes profit by producing the quantity where marginal cost (MC) equals marginal revenue (MR).

Price is then set according to the demand curve (D), indicated by point maximum in the figure.

The full-capacity average cost and quantity occur at the minimum point on the firm's average cost curve, indicated by @emclent in the figure

A monopolistically competitive firm maximizes its profit where it is operating at less than full capacity or minimum efficient scale, which is the smallest quantity at

which the average cost curve reaches its minimum (the bottom of a U-shaped average cost curve). The firm's minimum efficient scale is the quantity at which the

firm no longer benefits from economies of scale.

Does this result depend upon whether firms produce identical or differentiated products? Why?

A monopolistically competitive firm will not produce at lowest average cost

OA. regardless of whether it produces a differentiated or homogeneous product because both can have downward-sloping demand curves.

OB. regardless of whether it produces a differentiated or homogeneous product because both have U-shaped average cost curves.

OC. only if it produces a homogenous product because all firms producing homogenous products have downward sloping demand curves.

OD. regardless of whether it produces a differentiated or homogeneous product because both have horizontal demand curves.

OE. only if it produces a differentiated product because all firms producing homogeneous products have horizontal demand curves.

Puk

M

Qu

Maximum

MR

cient

D

QE

Q, Quantity

MC

AC

Q

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- hellparrow_forwardIn long run equilibrium, economic profits tend to zero in a perfectly competitive market and also in a monopolistically competitive market. This is true because both market structures share a crucial characteristic. What is the characteristic that causes economic profits to get pushed towards zero in both perfect competition and monopolistic competition?arrow_forwardWhat are the characteristics of monopolistically competitive markets? If the price of the product in a monopolistically competitive market increases what happens to the number of individual firms in the market and to the level of profit in the long run? Fully explain your answer.arrow_forward

- Suppose that a firm produces tennis racquets in a monopolistically competitive market. The following graph shows its demand curve (D), marginal revenue curve (MR), marginal cost curve (MC), and long-run average cost curve (LRAC). Assume that all firms in the industry face the same cost structure. Place the tan point (dash symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next, place the purple point (diamond symbol) to indicate the point at which this firm would produce in the long run if it operated in a perfectly competitive market. Note: Dashed drop lines will automatically extend to both axes. 100 LRAC 60 50 PRICE, COSTS, AND REVENUE (Dollars per racquet) 8 R 90 MC 10 0 0 10 D MR 50 60 70 80 90 100 20 30 40 QUANTITY (Thousands of racquets per month) Monopolistic Competition Outcome Perfect Competition Outcome Compare the average cost and the output in the long-run equilibrium for a monopolistically competitive…arrow_forwardDiscuss some products and markets that are good examples of Monopolistic Competition. Like the market structure of perfect competition, monopolistic competition assumes inexpensive entry into the market and thus many small sellers. Like the market structure of monopoly, monopolistic competition assumes a downward sloping demand curve. This is because, unlike the identical products found in perfectly competitive markets, the products in monopolistically competitive markets are differentiated and not perfect substitutes for one another. Therefore each monopolistically competitive seller has some degree of brand loyalty and would not lose all of its customers if it slightly raised its price above that of its competition. While not facing perfectly elastic, or horizontal, demand, the monopolistically competitive firm still faces a more elastic demand than the monopolist, whose product has no substitutes. Give two examples of markets where there are many choices among products, yet we…arrow_forwardSuppose that a firm produces wooden train engines in a monopolistically competitive market. The following graph shows its demand curve, marginal revenue (MR) curve, marginal cost (MC) curve, and average total cost (ATC) curve: Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm, Next, place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost.arrow_forward

- BYOB is a monopolist in beer production and distribution in the imaginary economy of Hopsville. Suppose that BYOB cannot price discriminate; that is, it sells its beer at the same price per can to all customers. The following graph shows the marginal cost (MC), marginal revenue (MR), average total cost (ATC), and demand (D) for beer in this market. Place the black point (plus symbol) on the graph to indicate the profit-maximizing price and quantity for BYOB. If BYOB is making a profit, use the green rectangle (triangle symbols) to shade in the area representing its profit. On the other hand, if BYOB is suffering a loss, use the purple rectangle (diamond symbols) to shade in the area representing its loss. PRICE (Dollars per can) 4.00 3.50 3.00 2.50 2.00 1.50 1.00 0.50 0 MC 0 0.5 1.5 ATC MR D 1.0 2.0 2.5 3.0 QUANTITY (Thousands of cans of beer) 3.5 4.0 Monopoly Outcome Profit Lossarrow_forwardLagatt Green is a monopoly beer producer and distributor operating in the hypothetical economy of Lightington. Assume that Lagatt Green is not able price discriminate, and so it sells its beer to all customers at the same price per bottle. The following graph gives the marginal cost (MC), marginal revenue (MR), average total cost (ATC), and demand (D) curves that Lagatt Green faces for beer in Lightington. Place the black point (plus symbol) on the graph to indicate the profit-maximizing price and quantity for Lagatt Green. If Lagatt Green is making a profit, use the green rectangle (triangle symbols) to shade in the area representing its profit. On the other hand, if Lagatt Green is suffering a loss, use the purple rectangle (diamond symbols) to shade in the area representing its loss. PRICE (Dollars per bottle) 4.00 3.50 3.00 2.50 2.00 1.50 1.00 0.50 D MC D 15 20 25 30 3.5 QUANTITY (Thousands of bottles of beer) 45 ATC MR Price (Dollars per bottle) 2.00 2.25 40 Monopoly Outcome…arrow_forwardProvide an example of an industry that is monopolistically competitive. Regarding average total cost at the profit maximizing output, what is the difference between perfect competition and monopolistic competition ?arrow_forward

- Suppose that a company operates in the monopolistically competitive market for denim jackets. The following graph shows the demand curve, marginal revenue (MR) curve, marginal cost (MC) curve, and average total cost (ATC) curve for the firm. Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next, place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost. PRICE (Dollars per jacket) 100 90 80 50 ATC 30 2 8 8 2 2 2 2 ° 60 MC MR Demand 0 + 0 10 20 30 40 50 60 70 80 90 100 QUANTITY (Thousands of jackets) Mon Comp Outcome Min Unit Cost (?)arrow_forwardSuppose you manage a firm in a monopolistically competitive market Suppose you manage a firm in a monopolistically competitive market. Which of the following strategies will do a better job of helping you maintain economic profits: obtaining a celebrity endorsement for your product or supporting the entry of firms that will compete directly with your biggest rival? Explain your answer. Suppose you manage a firm in a monopolistically competitive marketarrow_forwardQ2: You have a small decoration business primarily making custom paper mache pinata's. Monopolistic Competition. Each customer has unique custom order, therefore it is very difficult to figure out the marginal cost of each output. You charge a price of $15 for any small two foot by two foot pinata's. Without marginal cost, how can you check to see if the small pinata's were profitable?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education