Concept explainers

Videos

Operating Budget, Comprehensive Analysis

Allison Manufacturing produces a subassembly used in the production of jet aircraft engines.

The assembly is sold to engine manufacturers and aircraft maintenance facilities. Projected sales in units for the coming 5 months follow:

The following data pertain to production policies and manufacturing specifications followed by Allison Manufacturing:

- a. Finished goods inventory on January 1 is 32,000 units, each costing $166.06. The desired ending inventory for each month is 80% of the next month’s sales.

- b. The data on materials used are as follows:

Inventory policy dictates that sufficient materials be on hand at the end of the month to produce 50% of the next month’s production needs. This is exactly the amount of material on hand on December 31 of the prior year.

- c. The direct labor used per unit of output is 3 hours. The average direct labor cost per hour is $14.25.

- d.

Overhead each month is estimated using a flexible budget formula. (Note: Activity is measured in direct labor hours.)

- e. Monthly selling and administrative expenses are also estimated using a flexible budgeting formula. (Note: Activity is measured in units sold.)

- f. The unit selling price of the subassembly is $205.

- g. All sales and purchases are for cash. The cash balance on January 1 equals $400,000. The firm requires a minimum ending balance of $50,000. If the firm develops a cash shortage

by the end of the month, sufficient cash is borrowed to cover the shortage. Any cash borrowed is repaid at the end of the quarter, as is the interest due (cash borrowed at the end of the quarter is repaid at the end of the following quarter). The interest rate is 12% per annum. No money is owed at the beginning of January.

Required:

- 1. Prepare a monthly operating budget for the first quarter with the following schedules. (Note: Assume that there is no change in work-in-process inventories.)

- a. Sales budget

- b. Production budget

- c. Direct materials purchases budget

- d. Direct labor budget

- e. Overhead budget

- f. Selling and administrative expenses budget

- g. Ending finished goods inventory budget

- h. Cost of goods sold budget

- i.

Budgeted income statement - j.

Cash budget

- 2. CONCEPTUAL CONNECTION Form a group with two or three other students. Locate a manufacturing plant in your community that has headquarters elsewhere. Interview the controller for the plant regarding the

master budgeting process. Ask when the process starts each year, what schedules and budgets are prepared at the plant level, how the controllerforecasts the amounts, and how those schedules and budgets fit in with the overall corporate budget. Is the budgetary process participative? Also, find out how budgets are used for performance analysis. Write a summary of the interview.

1.

a.

Prepare sales budget.

Explanation of Solution

Sales budget for the first quarter:

| Particulars |

January ($) |

February ($) |

March ($) |

Total ($) |

| Sales units (A) | 40,000 | 50,000 | 60,000 | 150,000 |

| Selling price (B) | 205 | 205 | 205 | 205 |

| Sales | 8,200,000 | 10,250,000 | 12,300,000 | 30,750,000 |

Table (1)

b.

Prepare production budget.

Explanation of Solution

Production budget for the first quarter:

| Particulars |

January ($) |

February ($) |

March ($) |

Total ($) |

| Expected sales | 40,000 | 50,000 | 60,000 | 150,000 |

| Add: Closing units. 80% of sales units of next month |

40,000 |

48,000 | 136,000 | |

| Less: Opening units. 80% of sales units of the current month | 32,000 | 120,000 | ||

| Production units | 48,000 | 58,000 | 60,000 | 166,000 |

Table (2)

c.

Prepare direct materials purchases budget.

Explanation of Solution

Materials purchases budget:

| Particulars |

January ($) |

February ($) |

March ($) |

Total ($) |

| Expected production (sub-part b) | 48,000 | 58,000 | 60,000 | 166,000 |

| Add: Closing units. 50% of production units of next month 1 |

29,000 |

30,000 | 89,800 | |

| Less: Opening units. 50% of production units of the current month | 83,000 | |||

| Production units for which material is required to be purchased | 53,000 | 59,000 | 60,800 | 172,800 |

|

Metal cost: 10 lbs. per unit @ $8 (A) |

4,240,000 |

4,720,000 |

4,864,000 | 13,824,000 |

| Component cost: 6 per unit @ $5 (B) |

1,590,000 |

1,770,000 |

1,824,000 | 5,184,000 |

| Total material cost | 5,830,000 | 6,490,000 | 6,688,000 | 19,008,000 |

Table (3)

Working Notes:

1. Computation of production units of April:

d.

Prepare direct labor budget.

Explanation of Solution

Direct labor budget:

| Particulars |

January ($) |

February ($) |

March ($) |

Total ($) |

| Expected production (sub-part b) | 48,000 | 58,000 | 60,000 | 166,000 |

| Hours per unit | 3 | 3 | 3 | |

| Number of hours |

144,000 |

174,000 |

180,000 | 498,000 |

| Rate per hour | 14.25 | 14.25 | 14.25 | |

| Labor cost |

2,052,000 |

2,479,500 |

2,565,000 | 7,096,500 |

Table (4)

e.

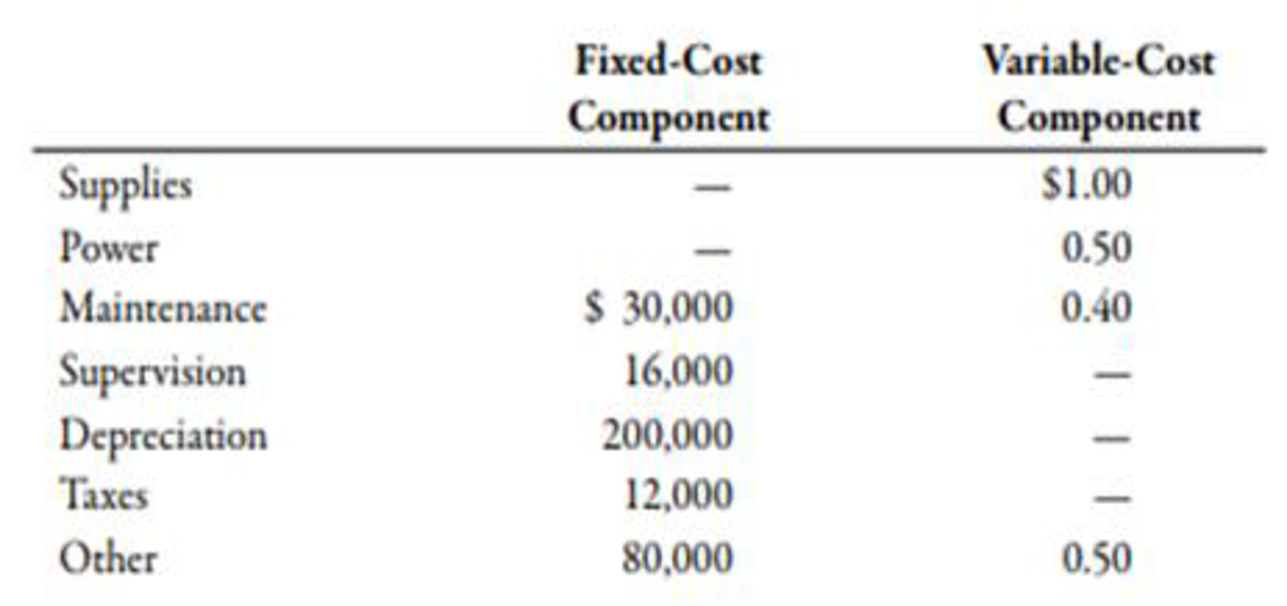

Prepare overhead budget.

Explanation of Solution

Overhead budget:

| Particulars |

January ($) |

February ($) |

March ($) |

Total ($) |

| Number of hours (sub-part d) | 144,000 | 174,000 | 180,000 | 498,000 |

| Variable overhead1 |

345,600 |

417,600 |

432,000 | 1,195,200 |

| Fixed overhead2 (B) | 338,000 | 338,000 | 338,000 | 1,014,000 |

|

Total overhead | 683,600 | 755,600 | 770,000 | 2,209,200 |

Table (5)

Working Notes:

1. Computation of variable overhead rate per hour per month:

2. Computation of fixed overhead rate per month:

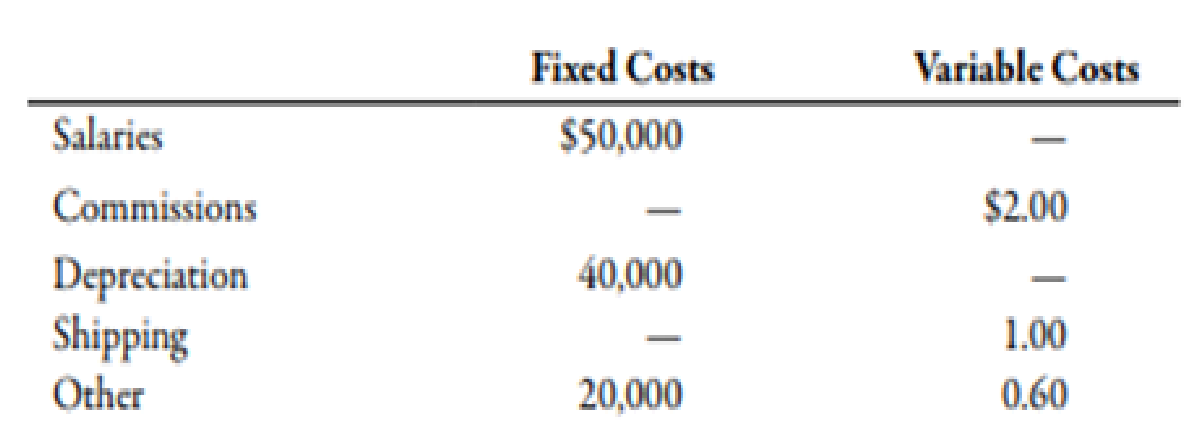

f.

Prepare selling and administrative expenses budget.

Explanation of Solution

Selling and administrative expenses budget:

| Particulars |

January ($) |

February ($) |

March ($) |

Total ($) |

| Number of sales units | 40,000 | 50,000 | 60,000 | 150,000 |

| Variable expense1 |

144,000 |

180,000 |

216,000 | 540,000 |

| Fixed expense2 (B) | 110,000 | 110,000 | 110,000 | 330,000 |

|

Total overhead | 254,000 | 290,000 | 326,000 | 870,000 |

Table (6)

Working Notes:

1. Computation of variable selling and administrative expense rate per unit:

2. Computation of fixed selling and administrative expense per month:

g.

Prepare ending goods inventory budget.

Explanation of Solution

Ending goods inventory budget:

| Particulars |

Amount ($) |

| Material cost: | |

| Metal | 80 |

| Add: Component | 30 |

| Add: Labor cost | 42.75 |

| Add: Variable overheads | 7.2 |

| Add: Fixed overheads1 | 6.11 |

| Unit cost | 166.06 |

| Cost of ending goods | 7,970,880 |

Table (7)

Working Notes:

1. Computation of fixed overhead per unit:

h.

Prepare COGS budget.

Explanation of Solution

Cost of goods sold budget:

| Particulars |

Amount ($) |

| Material cost: | |

| Metal | 13,280,000 |

| Add: Component | 4,980,000 |

| Add: Labor cost | 7,096,500 |

| Add: Variable overheads | 1,195,200 |

| Add: Fixed overheads | 1,014,000 |

| Manufacturing cost (A) | 27,565,700 |

| Add: Beginning finished goods | 5,313,920 |

| Cost of goods available for sale | 32,879,620 |

| Less: Ending goods (sub-part g) (D) | 7,970,880 |

| COGS | 24,908,740 |

Table (8)

i.

Prepare budgeted income statement.

Explanation of Solution

Budgeted income statement:

| Particulars |

Amount ($) |

| Sales | 30,750,000 |

| Less: COGS (sub-part h) | 24,908,740 |

| Operating profit | 5,841,260 |

| Less: Selling and administrative expenses | 870,000 |

| Income | 4,971,260 |

Table (9)

i.

Prepare budgeted income statement.

Explanation of Solution

Budgeted income statement:

| Particulars |

Amount ($) |

| Sales | 30,750,000 |

| Less: COGS (sub-part h) | 24,908,740 |

| Operating profit | 5,841,260 |

| Less: Selling and administrative expenses | 870,000 |

| Income | 4,971,260 |

Table (10)

j.

Prepare cash budget.

Explanation of Solution

Cash Budget:

| Particulars |

January ($) |

February ($) |

March ($) |

Total ($) |

| Opening balance | 400,000 | 50,000 | 524,900 | 400,000 |

| Sales (sub-part a) | 8,200,000 | 10,250,000 | 12,300,000 | 30,750,000 |

| Less: Material purchase (sub-part c) | 5,830,000 | 6,490,000 | 6,688,000 | 19,008,000 |

| Less: labor cost (sub-part d) | 2,052,000 | 2,479,500 | 2,565,000 | 7,096,500 |

| Less: Overhead cost (sub-part e) | 483,600 | 555,600 | 570,000 | 1,609,200 |

| Less: Selling and administrative expense (sub-part f) | 214,000 | 250,000 | 286,000 | 750,000 |

| Cash available | 20,400 | 524,900 | 2,715,900 | 2,686,300 |

| Amount borrowed | 29,600 | 0 | 0 | 29,600 |

| Amount repaid1 | 0 | 0 | 30,488 | 30,488 |

| Closing balance | 50,000 | 524,900 | 2,685,412 | 2,685,412 |

Table (11)

Working Notes:

1. Computation of amount repaid:

Depreciation is not considered in cash payments since it is a non-cash expense.

2.

Prepare summary regarding budgets used in ABC incorporation.

Explanation of Solution

In ABC incorporation, participative budgeting is used; all the supervisors and department heads are involved in preparation of the relevant budgets to increase the probability of meeting the budgets.

However, preparation of budgets is not entirely delegated to the sub-ordinate managers and supervisors, their issues and reasonable figures are asked and on that basis, higher management decides budgetary figures.

After expiry of the period, budgets are adjusted according to actual units sold and thereafter, such budget is prepared with actual budget to find out discrepancies.

Thereafter, reasons behind all the variances are observed. Amount of variance, attributable to managerial performances are considered as one of the factors in performance analysis.

All the operating budgets like; sales, production, material purchase, labor, overhead, selling and administrative overhead, finished goods inventory, COGS as well as cash budget is prepared for planning and controlling purposes.

All these budgets help in determination of budgeted income and cash requirements. This can be explained as follows:

- Sales budget is used to prepare production budget and selling and administrative expenses budget.

- Production budget is used to prepare material purchase budget and labor budget.

- Labor budget (labor hours) is used to prepare manufacturing overhead budget.

- Production, material, labor, and production overhead budgets are used to compute ending finished goods inventory budget and based on these budgets COGS budget is prepared.

- Budgeted income statement is prepared by using sales budget, COGS budget and selling and administrative expenses budget.

- Sales, material, labor, production overhead, and selling overhead budgets are used to prepare cash budget.

Budgets are forecasted by using past year data. Past year data is adjusted with inflation and other economic factors like availability of new clients, to prepare budgets for the current year.

Want to see more full solutions like this?

Chapter 9 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- Cash budget The controller of Bridgeport Housewares Inc. instructs you to prepare a monthly cash budget for the next three months. You are presented with the following budget information: The company expects to sell about 10% of its merchandise for cash. Of sales on account, 70% are expected to be collected in the month following the sale and the remainder the following month (second month following sale). Depreciation, insurance, and property tax expense represent 50,000 of the estimated monthly manufacturing costs. The annual insurance premium is paid in January, and the annual property taxes are paid in December. Of the remainder of the manufacturing costs, 80% are expected to be paid in the month in which they are incurred and the balance in the following month. Current assets as of September 1 include cash of 40,000, marketable securities of 75,000, and accounts receivable of 300,000 (60,000 from July sales and 240,000 from August sales). Sales on account for July and August were 200,000 and 240,000, respectively. Current liabilities as of September 1 include 40,000 of accounts payable incurred in August for manufacturing costs. All selling and administrative expenses are paid in cash in the period they are incurred. An estimated income tax payment of 55,000 will be made in October. Bridgeports regular quarterly dividend of 25,000 is expected to be declared in October and paid in November. Management desires to maintain a minimum cash balance of 50,000. Instructions Prepare a monthly cash budget and supporting schedules for September, October, and November. On the basis of the cash budget prepared in part (1), what recommendation should be made to the controller?arrow_forwardCash budget The controller of Mercury Shoes Inc. instructs you to prepare a monthly cash budget for the next three months. You are presented with the following budget information: The company expects to sell about 10% of its merchandise for cash. Of sales on account, 60% are expected to be collected in the month following the sale and the remainder the following month (second month after sale). Depreciation, insurance, and property tax expense represent 12,000 of the estimated monthly manufacturing costs. The annual insurance premium is paid in February, and the annual property taxes are paid in November. Of the remainder of the manufacturing costs, 80% are expected to be paid in the month in which they are incurred and the balance in the following month. Current assets as of June 1 include cash of 42,000, marketable securities of 25,000, and accounts receivable of 198,000 (150,000 from May sales and 48,000 from April sales). Sales on account in April and May were 120,000 and 150,000, respectively. Current liabilities as of June 1 include 13,000 of accounts payable incurred in May for manufacturing costs. All selling and administrative expenses are paid in cash in the period they are incurred. An estimated income tax payment of 24,000 will be made in July. Mercury Shoes regular quarterly dividend of 15,000 is expected to be declared in July and paid in August. Management desires to maintain a minimum cash balance of 40,000. Instructions Prepare a monthly cash budget and supporting schedules for June, July, and August. On the basis of the cash budget prepared in part (1), what recommendation should be made to the controller?arrow_forwardBudgeted income statement and supporting budgets for three months Bellaire Inc. gathered the following data for use in developing the budgets for the first quarter (January, February, March) of its fiscal year: Estimated sales at 125 per unit: Estimated finished goods inventories: Work in process inventories are estimated to be insignificant (zero). Estimated direct materials inventories: Manufacturing costs: Selling expenses: Instructions Prepare the following budgets using one column for each month and a total column for the first quarter, as shown for the sales budget: Prepare a sales budget for March. Prepare a production budget for March. Prepare a direct materials purchases budget for March. Prepare a direct labor cost budget for March. Prepare a factory overhead cost budget for March. Prepare a cost of goods sold budget for March. Prepare a selling and administrative expenses budget for March. Prepare a budgeted income statement with budgeted operating income for March.arrow_forward

- Production budget Healthy Measures Inc. produces a Bath and Gym version of its popular electronic scale. The anticipated unit sales for the scales by sales region are as follows: The finished goods inventory estimated for March 1, for the Bath and Gym scale models is 11,800 and 8,100 units, respectively. The desired finished goods inventory for March 31 for the Bath and Gym scale models is 15,000 and 7,500 units, respectively. Prepare a production budget for the Bath and Gym scales for the month ended March 31.arrow_forwardPalmgren Company produces consumer products. The sales budget for four months of the year is presented below. Company policy requires that ending inventories for each month be 25 percent of next months sales. At the beginning of July, the beginning inventory of consumer products met that policy. Required: Prepare a production budget for the third quarter of the year. Show the number of units that should be produced each month as well as for the quarter in total.arrow_forwardStatic budget versus flexible budget The production supervisor of the Machining Department for Hagerstown Company agreed to the following monthly static budget for the upcoming year: The actual amount spent and the actual units produced in the first three months in the Machining Department were as follows: The Machining Department supervisor has been very pleased with this performance because actual expenditures for May-July have been significantly less than the monthly static budget of2,358,000. However, the plant manager believes that the budget should not remain fixed for every month but should flex or adjust to the volume of work that is produced in the Machining Department. Additional budget information for the Machining Department is as follows: a. Prepare a flexible budget for the actual units produced for May, June, and July in the MachiningDepartment. Assume depreciation is a fixed cost. b. Compare the flexible budget with the actual expenditures for the first three months.What does this comparison suggest?arrow_forward

- Preparing a Direct Materials Purchases Budget Patrick Inc. makes industrial solvents sold in 5-gallon drums. Planned production in units for the first 3 months of the coming year is: Each drum requires 5.5 gallons of chemicals and one plastic drum. Company policy requires that ending inventories of raw materials for each month be 15% of the next months production needs. That policy was met for the ending inventory of December in the prior year. The cost of one gallon of chemicals is 2.00. The cost of one drum is 1.60. (Note: Round all unit amounts to the nearest unit. Round all dollar amounts to the nearest dollar.) Required: 1. Calculate the ending inventory of chemicals in gallons for December of the prior year and for January and February. What is the beginning inventory of chemicals for January? 2. Prepare a direct materials purchases budget for chemicals for the months of January and February. 3. Calculate the ending inventory of drums for December of the prior year and for January and February. 4. Prepare a direct materials purchases budget for drums for the months of January and February.arrow_forwardRelevant data from the Poster Companys operating budgets are: Additional data: Capital assets were sold in January for $10,000 and $4,500 in May. Dividends of $4,500 were paid in February. The beginning cash balance was $60,359 and a required minimum cash balance is $59,000. Use this information to prepare a cash budget for the first two quarters of the yeararrow_forwardBudgeted income statement and balance sheet As a preliminary to requesting budget estimates of sales, costs, and expenses for the fiscal year beginning January 1, 20Y9, the following tentative trial balance as of December 31, 20Y8, is prepared by the Accounting Department of Mesa Publishing Co.: Factory output and sales for 20Y9 are expected to total 3,800 units of product, which are to be sold at 120 per unit. The quantities and costs of the inventories at December 31, 20Y9, are expected to remain unchanged from the balances at the beginning of the year. Budget estimates of manufacturing costs and operating expenses for the year are summarized as follows: Balances of accounts receivable, prepaid expenses, and accounts payable at the end of the year are not expected to differ significantly from the beginning balances. Federal income tax of 35,000 on 20Y9 taxable income will be paid during 20Y9. Regular quarterly cash dividends of 0.20 per share are expected to be declared and paid in March, June, September, and December on 20,000 shares of common stock outstanding. It is anticipated that fixed assets will be purchased for 22,000 cash in May. Instructions Prepare a budgeted income statement for 20Y9. Prepare a budgeted balance sheet as of December 31, 20Y9, with supporting calculations.arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College