Concept explainers

Videos

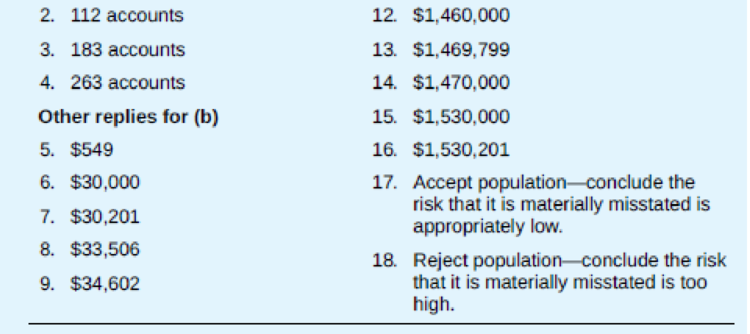

Smith, Inc.

Rachel Robertson wishes to use mean-per-unit sampling to evaluate the reasonableness of the book value of the

Required:

- a. Calculate the required

sample size . - b. Assuming the following results:

Book value of items in sample = $149

Average audited value of items in sample = $146

Standard deviation of sample = $28

use the mean-per-unit method to:

- (1) Calculate the point estimate of the account’s audited value.

- (2) Calculate the projected misstatement for the population.

- (3) Calculate the adjusted allowance for sampling risk.

- (4) State the auditors’ conclusion in this situation (accept or reject).

Use the following replies for the above questions—replies may be used once, more than once, or not at all. In all cases, select the reply closest to your answer.

Want to see the full answer?

Check out a sample textbook solution

Chapter 9 Solutions

Principles Of Auditing & Other Assurance Services

- Comprehensive Problem: Monetary Unit Sampling. Dylan Mays is auditing the accountsreceivable of Channel Company. Channel’s accounts receivable were recorded at $2,000,000and comprised more than 1,500 customer accounts. However, Channel’s ten largest customers’ balances comprised a high percentage of the recorded accounts receivable (over$500,000, or 25 percent). As a result, Mays is considering the use of MUS.Based on prior audits and other judgments, Mays has established the following parameters: Risk of incorrect acceptance 5% Tolerable misstatement $120,000 Expected misstatement $ 24,000 Required:a. Briefly identify what factors Mays should consider in determining sample size and howthese factors would be assessed.b. Calculate the necessary sample size and sampling interval used by Mays in the audit ofChannel Company.c. Given the information in part (b), describe how Mays would select the sample fromChannel’s computerized accounts receivable ledger.d. [Note: Part (d) is…arrow_forwardThe accounting department of the client reports that the balance of Accounts Receivable is $210,000. Using classical variable sampling, the auditor computes an estimated total population value of $216,500 and computed a 95% achieved allowance for sampling risk of +- $8,500. The auditor should conclude that the accounts receivable balance is fairly stated. on Select one: O a. False Ob. True Iarrow_forwardIn an MUS sample with a sampling interval of $5,000, an auditor discovered that aselected accounts receivable with a recorded amount of $10,000 had an audit valueof $8,000. If this is the only error discovered by the auditor, the projected error ofthe sample would be(1) $1,000. (3) $4,000.(2) $2,000. (4) $5,000.arrow_forward

- Sample Size Relationships: Monetary Unit Sampling. Noel Frehley is examining theaccounts receivable of Kiss Company and is considering the use of MUS. Kiss’s accountsreceivable are recorded at $400,000. Based on the necessary level of risk, Frehley has established a risk of incorrect acceptance of 5 percent. In addition, based on previous audits,Frehley estimates misstatements of $10,000. Finally, based on the overall level of performance materiality, Frehley has established tolerable misstatement at $20,000.Required:a. Determine the necessary sample size for Frehley’s examination of Kiss Company’saccounts receivable.b. Assume that Frehley was interested in trying to reduce the necessary sample size. Whatare some options available in this regard?c. Based on a discussion with the senior manager, Frehley knows that increasing the level ofthe risk of incorrect acceptance will reduce sample size. For the same level of expectedmisstatement, tolerable misstatement, and population size,…arrow_forwardThe auditors of Landi Corporation wish to use a structured approach to nonstatistical sampling to evaluate the reasonableness of the accounts receivable. Landi has 15,000 receivable accounts with a total book value of $2,500,000. The auditors have assessed the combined level of inherent and control risk at a moderate level and believe that their other substantive procedures are so limited as to require a “maximum” risk assessment. After considering the overall audit plan, the auditors believe that the test’s tolerable misstatement is $57,500. Use figure below to determine the reliability factor. Please calculate the sample size. Risk That Other Substantive Procedures Will Fail to Detect a Material Misstatement Combined Assessment of Inherent and Control Risk Maximum Moderate Low Maximum 3.0 2.3 1.9 Slightly below Maximum 2.7 2.0 1.6 Moderate 2.3 1.6 1.2 Low 1.9 1.2 1.0arrow_forwardThe 1,000 accounts receivable of Baker Company have a total book value of $60,000 (average book value $60), Wendy Duffo, Certified Public Accountant (CPA). has selected and audited a sample of 50 accounts with the following mean values: 1 Book value of $58.00 2. Audited value of $59.00. What is the estimated total audited value using mean-per-unit classical variables sampling? Multiple Choice $61,034 $59,000 $61,000 $58,000arrow_forward

- Sample Size Determination: Monetary Unit Sampling. The recorded accounts receivable balance for Warner Company was $500,000.Required:For each of the following independent sets of conditions, determine the appropriate samplesize for the examination of Warner’s accounts receivable in MUS. Based on the differencesin your calculations, identify the general relationship between different factors and samplesize. (RIA = risk of incorrect acceptance, TM = tolerable misstatement, EM = expectedmisstatement).a. RIA = 5%, TM = $50,000, EM = $10,000.b. RIA = 5%, TM = $50,000, EM = $25,000.c. RIA = 10%, TM = $50,000, EM = $10,000.d. RIA = 10%, TM = $50,000, EM = $25,000.arrow_forwardSample Size Determination: Classical Variables Sampling. Shannon Solomon, CPA, isauditing the accounts receivable of Warner Company and is using mean-per-unit estimation.Accounts receivable were recorded at $2,000,000 and comprised 1,250 individual customeraccounts. Solomon established the following parameters for the audit of accounts receivable:∙ Using firm policy, tolerable misstatement for accounts receivable is established at 6 percent of the recorded account balance.∙ Based on prior audits of Warner’s accounts receivable, the standard deviation of auditedvalues is estimated to be $100.∙ Based on prior audits of Warner’s accounts receivable, Solomon estimates that accountsreceivable will be misstated by 4 percent of the recorded account balance.Solomon is now establishing the acceptable levels of the risk of incorrect acceptance and therisk of incorrect rejection for the audit of Warner Company’s accounts receivable.Required:a. What factors should Solomon consider in establishing…arrow_forwardAn audit firm is conducting the audit of Diaz Construction Company for the fiscal year ended October 31. Rebecca Smith, the partner in charge of the audit, decides that MUS is the appropriate sampling technique to use in order to audit Diaz’s inventory account. The balance in the inventory at October 31 was $4,250,000. Rebecca has established the following: risk of incorrect acceptance = 5% (i.e., the desired confidence level of 95%), tolerable misstatement = $212,500, and expected misstatement = $63,750. Calculate the sample size and sampling interval using Table 8-5 in the textbook (round your interval answer to the nearest whole number).arrow_forward

- Upper Limit on Misstatements Calculation: Monetary Unit Sampling. The auditorsmailed positive confirmations on 60 customers’ accounts receivable balances. The company’saccounts receivable balance comprised 2,356 customer accounts with a total recorded balanceof $19,600,000, and the sampling interval was $280,000. The auditors received four positiveconfirmation returns reporting exceptions. Upon follow-up, they found the following:∙ Account 2333. Recorded balance $8,345. The account was overstated by $1,669 becausethe client made an arithmetic mistake recording a credit memo. The company issued only86 credit memos during the year. The auditors examined all of them for the same arithmetic mistake and found no similar misstatements.∙ Account 363. Recorded balance $7,460. The account was overstated by $1,865 because thecompany sold merchandise to a customer with payment due in six months plus 15 percentinterest. The billing clerk made a mistake and recorded the sales price and the…arrow_forwardCarson Allister is performing a PPS application in the audit of Bird Company’s accounts receivable. Based on the acceptable level of the risk of incorrect acceptance of 5 percent and a tolerable misstatement of $120,000, Allister has calculated a sample size of 75 items and a sampling interval of $25,000. After examining the sample items, the following misstatements were identified: (Use Exhibit F.A.2.) Item Recorded Balance Audited Value 1 $35,000 $28,000 2 10,000 8,000 3 6,000 3,000 Required: Calculate the upper limit on misstatements for Bird Company’s accounts receivable.arrow_forwardThe 10,000 accounts receivable of DEF Company have a total book value of $120,000. A CPA has selected and audited a sample of 100 accounts with a total book value of $1,000 and an audited value of $1,200. Using the ratio estimation technique, the estimated total audited value of the population is: 140,000 100,000 144,000 120,000arrow_forward

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning