Concept explainers

Videos

Phoenix Company’s 2015

Required

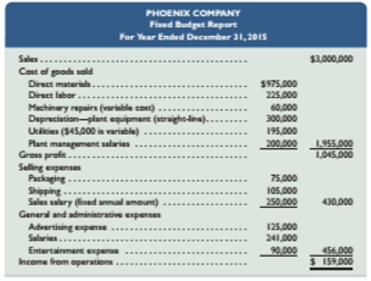

- Classify all items listed in the fixed budget as variable or fixed. Also determine their amounts per unit or their amounts for the year, as appropriate.

- Prepare flexible budgets (See Exhibit 8.3) for the company at sales volumes of 14,000 and 16,000 units.

- The company’s business conditions are improving. One possible result is a sales volume of 18,000 units. The company president in confident that this volume is within the relevant range of existing capacity. How much would operating income increase over the 2015 budgeted amount of $159,000 if this level is reached without increasing capacity?

- An unfavorable change in business is remotely possible; in this case, production and sales volume for 2015 could fall to 12,000 units. How much income (or loss) from operations would occurs if sales volume falls to this level?

Concept introduction:

Fixed Budget:

A fixed budget, also known as static budget does not adjust throughout the budget period and is prepared on the assumption that specific amount of goods would be sold in the concerned period.

Requirement 1:

Classification of items of fixed budget as fixed or variable and their amounts per unit or their amounts for the year.

Answer to Problem 1PSA

Classification of fixed budget items as fixed or variable:

| Particulars | Total amount (In $) | Amount per unit (In $) |

| Variable costs: | ||

| Direct materials | 9, 75, 000 | 65 |

| Direct labor | 2, 25, 000 | 15 |

| Machinery repairs | 60, 000 | 4 |

| Utilities | 45, 000 | 3 |

| Packaging | 75, 000 | 5 |

| Shipping | 1, 05, 000 | 7 |

| Total variable costs | 99 | |

| Fixed costs: | ||

| Depreciation- Plant equipment | 3, 00, 000 | |

| Utilities | 1, 50, 000 | |

| Plant management salaries | 2, 00, 000 | |

| Sales salaries | 2, 50, 000 | |

| Advertising expense | 1, 25, 000 | |

| Salaries | 2, 41, 000 | |

| Entertainment expense | 90, 000 | |

| Total fixed costs | 13, 56, 000 |

Explanation of Solution

The items laid in fixed budget of the company in the given problem can be classified into variable or fixed based on their nature i.e. on the basis of their behavior and traceability as explained below:

Variable costs vary directly with the production level i.e. company’s variable cost increases as the production increases and vice-a-versa. Therefore, following costs would be classified as Variable:

- Direct materials: The direct materials would be relate to the amount paid for procurement of materials which would vary

- Direct labor: The payment made to direct labor would vary depending on the production

- Machinery repairs: The repairs done on machinery would be varied depending upon the usage of machinery for production of output

- Utilities: Utilities would be acquired depending on their requirement which would vary

- Packaging: The amount spent on packaging would be in relation to products produced which would vary

- Shipping: Expenses incurred on shipping would be incurred based on the number of products produced

Fixed costs do not vary with the level of production. They do not change with the amount of goods or services a company produces. Therefore, those costs which are fixed in nature would be covered under fixed costs as given below:

- Depreciation- Plant equipment: The depreciation charged on plants equipment would remain fixed and would not change with the level of production

- Utilities: Utilities other than variable in nature would be covered under fixed cost

- Plant management salaries: The salaries paid for managing would be fixed in nature

- Sales salaries: Salaries paid to sales staff would remain fixed in nature

- Advertising expense: The expenses on advertising would be covered under fixed cost

- Salaries: Salaries paid to staff would remain fixed in nature and would not change with the level of production

- Entertainment expense: Expenses on entertainment are fixed irrespective of the level of production

Further, it is given in the problem that sales volume is 15, 000 units and Sales are $3, 000, 0000. Therefore, calculation of Variable cost per unit has been calculated using the following formula:

Following would be the per unit amounts:

Thus, the total variable costs would be the following:

Also, fixed costs would include the following;

Therefore, classification of fixed budget items as asked in the given problem is shown below in the tabular manner:

Classification of fixed budget items as fixed or variable:

| Particulars | Total amount (In $) | Amount per unit (In $) |

| Variable costs: | ||

| Direct materials | 9, 75, 000 | 65 |

| Direct labor | 2, 25, 000 | 15 |

| Machinery repairs | 60, 000 | 4 |

| Utilities | 45, 000 | 3 |

| Packaging | 75, 000 | 5 |

| Shipping | 1, 05, 000 | 7 |

| Total variable costs | 99 | |

| Fixed costs: | ||

| Depreciation- Plant equipment | 3, 00, 000 | |

| Utilities | 1, 50, 000 | |

| Plant management salaries | 2, 00, 000 | |

| Sales salaries | 2, 50, 000 | |

| Advertising expense | 1, 25, 000 | |

| Salaries | 2, 41, 000 | |

| Entertainment expense | 90, 000 | |

| Total fixed costs | 13, 56, 000 |

Concept introduction:

Flexible Budget:

A flexible budget, also known as variation budget adjusts to changes in volume or activity. Flexible budgets are prepared for comparing actual to budgeted performances at many levels of activity during the previous year. In order to accurately predict the changes in costs, management identifies them into fixed or variable costs.

Fixed cost:

These costs do not vary with the level of production. They do not change with the amount of goods or services a company produces. They remain same even if the company does not produce any product or provide any service during an accounting period.

Variable cost:

These costs vary with the level of production. They are usually shown in the budget as either a percentage of total revenue or at a constant rate per unit produced.

Requirement 2:

Flexible budget for the company at sales volume of 14, 000 units and 16, 000 units.

Answer to Problem 1PSA

Flexible budget for the company for the year ended December 31, 2015 (Amount in $):

| Company | ||||

| Flexible budget | ||||

| For year ended December 31, 2015 | ||||

| Particulars | Flexible budget | Flexible budget for 14, 000 units sold | Flexible budget for 16, 000 units sold | |

| Variable amount per unit | Total fixed cost | |||

| Sales | 200 | 28, 00, 000 | 32, 00, 000 | |

| Variable costs: | ||||

| Direct materials | 65 | 9, 10, 000 | 10, 40, 000 | |

| Direct labor | 15 | 2, 10, 000 | 2, 40, 000 | |

| Machinery repairs | 4 | 56, 000 | 64, 000 | |

| Utilities | 3 | 42, 000 | 48, 000 | |

| Packaging | 5 | 70, 000 | 80, 000 | |

| Shipping | 7 | 98, 000 | 1, 12, 000 | |

| Total variable costs | 99 | 13, 86, 000 | 15, 84, 000 | |

| Contribution margin | 101 | 14, 14, 000 | 16, 16, 000 | |

| Fixed costs: | ||||

| Depreciation- Plant equipment | 3, 00, 000 | 3, 00, 000 | 3, 00, 000 | |

| Utilities | 1, 50, 000 | 1, 50, 000 | 1, 50, 000 | |

| Plant management salaries | 2, 00, 000 | 2, 00, 000 | 2, 00, 000 | |

| Sales salary | 2, 50, 000 | 2, 50, 000 | 2, 50, 000 | |

| Advertising expense | 1, 25, 000 | 1, 25, 000 | 1, 25, 000 | |

| Salaries | 2, 41, 000 | 2, 41, 000 | 2, 41, 000 | |

| Entertainment expense | 90, 000 | 90, 000 | 90, 000 | |

| Total fixed costs | 13, 56, 000 | 13, 56, 000 | 13, 56, 000 | |

| Income from operations | 58, 000 | 2, 60, 000 | ||

Explanation of Solution

For preparation of flexible budget of the company, following formulas would be used:

In the given problem, it is given that sales are $30, 00, 000 and sales volume is 15, 000 units.

Flexible budget has to be prepared at sales volume of 14, 000 and 16, 000 units. We have already calculated variable cost per unit of all the items. Now, calculations for variable cost have been made in the following manner:

| Particulars | Variable amount per unit (Amount in $) | For 14, 000 units sold | For 16, 000 units sold |

| Sales | 200 | $200*14, 000 = 28, 00, 000 | $200*16, 000 = 32, 00, 000 |

| Variable costs: | |||

| Direct materials | 65 | $65*14, 000 = 9, 10, 000 | $65*16, 000 = 10, 40, 000 |

| Direct labor | 15 | $15*14, 000 = 2, 10, 000 | $15*16, 000 = 2, 40, 000 |

| Machinery repairs | 4 | $4*14, 000 = 56, 000 | $4*16, 000 = 64, 000 |

| Utilities | 3 | $3*14, 000 = 42, 000 | $3*16, 000 = 48, 000 |

| Packaging | 5 | $5*14, 000 = 70, 000 | $5*16, 000 = 80, 000 |

| Shipping | 7 | $7*14, 000 = 98, 000 | $7*16, 000 = 1, 12, 000 |

| Total variable costs | 99 | 13, 86, 000 | 15, 84, 000 |

Further, contribution margin can be calculated using the below- mentioned formulas:

Thus, contribution margin would be:

Fixed costs would remain same irrespective of the changes in sales volume. Also, Income from operations can be computed using the following formula:

Therefore, flexible budget asked in the given problem at 14, 000 and 16, 000 units is given below:

Flexible budget for the company for the year ended December 31, 2015 (Amount in $):

| Company | ||||

| Flexible budget | ||||

| For year ended December 31, 2015 | ||||

| Particulars | Flexible budget | Flexible budget for 14, 000 units sold | Flexible budget for 16, 000 units sold | |

| Variable amount per unit | Total fixed cost | |||

| Sales | 200 | 28, 00, 000 | 32, 00, 000 | |

| Variable costs: | ||||

| Direct materials | 65 | 9, 10, 000 | 10, 40, 000 | |

| Direct labor | 15 | 2, 10, 000 | 2, 40, 000 | |

| Machinery repairs | 4 | 56, 000 | 64, 000 | |

| Utilities | 3 | 42, 000 | 48, 000 | |

| Packaging | 5 | 70, 000 | 80, 000 | |

| Shipping | 7 | 98, 000 | 1, 12, 000 | |

| Total variable costs | 99 | 13, 86, 000 | 15, 84, 000 | |

| Contribution margin | 101 | 14, 14, 000 | 16, 16, 000 | |

| Fixed costs: | ||||

| Depreciation- Plant equipment | 3, 00, 000 | 3, 00, 000 | 3, 00, 000 | |

| Utilities | 1, 50, 000 | 1, 50, 000 | 1, 50, 000 | |

| Plant management salaries | 2, 00, 000 | 2, 00, 000 | 2, 00, 000 | |

| Sales salary | 2, 50, 000 | 2, 50, 000 | 2, 50, 000 | |

| Advertising expense | 1, 25, 000 | 1, 25, 000 | 1, 25, 000 | |

| Salaries | 2, 41, 000 | 2, 41, 000 | 2, 41, 000 | |

| Entertainment expense | 90, 000 | 90, 000 | 90, 000 | |

| Total fixed costs | 13, 56, 000 | 13, 56, 000 | 13, 56, 000 | |

| Income from operations | 58, 000 | 2, 60, 000 | ||

Thus, the income from operations of company at sales volume of 14, 000 and 16, 000 units are $58, 000 and $2, 60, 000 respectively.

Concept introduction:

Fixed cost:

These costs do not vary with the level of production. They do not change with the amount of goods or services a company produces. They remain same even if the company does not produce any product or provide any service during an accounting period.

Variable cost:

These costs vary with the level of production. They are usually shown in the budget as either a percentage of total revenue or at a constant rate per unit produced.

Requirement 3:

Increase in operating income at 18, 000 units without increasing capacity.

Answer to Problem 1PSA

Increase in operating income at 18, 000 units without increasing capacity = $3, 03, 000

Explanation of Solution

Sales volume has been increased to 18, 000 units from 15, 000 units, thereby increasing 3, 000 units sold (18, 000 units- 15, 000 units). For calculating increase in operating income with existing capacity and fixed costs, firstly total contribution margin would be calculated using the following formula:

Contribution margin per unit has already been calculated as $101 per unit. Thus,

Total fixed costs are calculated as $13, 56, 000. Therefore, all the calculations have been shown in the table below:

| Particulars | Amount |

| Total contribution margin | $101* 18, 000 units = $18, 18, 000 |

| Less: Fixed costs | ($13, 56, 000) |

| Potential operating loss | $4, 62, 000 |

| Budgeted income of 2015 | ($1, 59, 000) |

| Increase in operational income | $3, 03, 000 |

Therefore, Increase in operating income at 18, 000 units without increasing capacity is coming out to be $3, 03, 000.

Concept introduction:

Fixed cost:

These costs do not vary with the level of production. They do not change with the amount of goods or services a company produces. They remain same even if the company does not produce any product or provide any service during an accounting period.

Variable cost:

These costs vary with the level of production. They are usually shown in the budget as either a percentage of total revenue or at a constant rate per unit produced.

Requirement 4:

Income (or loss) from operations if sales volume fall to 12, 000 units.

Answer to Problem 1PSA

Potential operating loss at sales volume of 12, 000 units = $1, 44, 000

Explanation of Solution

Sales volume has fallen to 12, 000 units from 15, 000 units, thereby decreasing 3, 000 units sold (15, 000 units- 12, 000 units). For calculating income (or loss) from operations, firstly total contribution margin would be calculated using the following formula:

Contribution margin per unit has already been calculated as $101 per unit. Thus,

Total fixed costs are calculated as $13, 56, 000. Therefore, all the calculations have been shown in the table below:

| Particulars | Amount |

| Total contribution margin | $101* 12, 000 units = $12, 12, 000 |

| Less: Fixed costs | ($13, 56, 000) |

| Potential operating loss | $1, 44, 000 |

Therefore, the potential operating loss at 12, 000 units is coming out to be $1, 44, 000.

Want to see more full solutions like this?

Chapter 8 Solutions

MANAGERIAL ACCOUNTING FUND. W/CONNECT

- Carmichael Corporation is in the process of preparing next years budget. The pro forma income statement for the current year is as follows: Required: 1. What is the break-even sales revenue (rounded to the nearest dollar) for Carmichael Corporation for the current year? 2. For the coming year, the management of Carmichael Corporation anticipates an 8 percent increase in variable costs and a 60,000 increase in fixed expenses. What is the break-even point in dollars for next year? (CMA adapted)arrow_forwardReview the completed master budget and answer the following questions: Is Ranger Industries expecting to earn a profit during the next quarter? If so, how much? Does the company need to borrow cash during the quarter? Can it make any repayments? Explain. (Carefully review rows 74 through 80.)arrow_forwardBefore the year began, the following static budget was developed for the estimated sales of 50,000. Sales are higher than expected and management needs to revise its budget. Prepare a flexible budget for 100,000 and 110,000 units of sales.arrow_forward

- Before the year began, the following static budget was developed for the estimated sales of 100,000. Sales are sluggish and management needs to revise its budget. Use this information to prepare a flexible budget for 80,000 and 90,000 units of sales.arrow_forwardStarburst Inc. has the following items and amounts as part of its master budget at the 10,000-unit level of sales and production: Determine the total dollar amounts for the above items that would appear in a flexible budget at the following volume levels, assuming that both levels are within the relevant range: a. 8,000-unit level of sales and production b. 12,000-unit level of sales and production (Hint: You must first determine the unit selling price and certain unit costs.)arrow_forwardRegal Furnitures produces and sells high-quality reading tables. One of the very popular models in the reading table lineup is RT360. The management accountant of the company is in the process of preparing its Selling and Administrative Expense Budget for the first quarter of the year. The following budget data are available: Assume that all of these expenses (except depreciation) are paid in cash in the month they are incurred. Answer the following questions:a) If Regal Furnitures has budgeted to sell 19,000 RT360 tables in January, then what will be the total budgeted selling and administrative expenses for January?b) If the company has budgeted to sell 16,000 RT360 tables in February, then what will be the budgeted total cash disbursements for selling and administrative expenses for February?c) If the budgeted total cash disbursements for selling and administrative expenses for March total Tk. 459,200, then how many RT360 table does the company plan to sell in March?arrow_forward

- McGuire Industries prepares budgets to help manage the company. McGuire is budgeting forthe fiscal year ended January 31, 2018. During the preceding year ended January 31, 2017, salestotaled $9,200 million and cost of goods sold was $6,300 million. At January 31, 2017, inventorywas $1,700 million. During the upcoming 2018 year, suppose McGuire expects cost of goodssold to increase by 12%. The company budgets next year’s ending inventory at $2,000 million.Requirement1. One of the most important decisions a manager makes is how much inventory to buy. Howmuch inventory should McGuire purchase during the upcoming year to reach its budget?arrow_forwardMcGuire prepares budgets to help manage the company. McGuire is budgeting forthe fiscal year ended January 31, 2016. During the preceding year ended January 31, 2015, salestotaled $9,500 million and cost of goods sold was $6,300 million. At January 31, 2015, inventorywas $1,800 million. During the upcoming 2016 year, suppose McGuire expects cost of goodssold to increase by 10%. The company budgets next year’s ending inventory at $2,100 million.Requirement1. One of the most important decisions a manager makes is how much inventory to buy. Howmuch inventory should McGuire purchase during the upcoming year to reach its budget?arrow_forwardPhoenix Company’s 2019 master budget included the following fixed budget report. It is based on an expected production and sales volume of 15,000 units. d. Organize a template for variable costing income statements in which the sales volume is a variable.e. Test your template for 15,000 units sales volume to see if you get the same income as stated abovearrow_forward

- Using sensitivity analysis Holly Company prepared the following budgeted income statement for the first quarter of 2018: Holly Company is considering two options. Option 1 is to increase advertising by $700 per month. Option 2 is to use better-quality materials in the manufacturing process. The better materials will increase the cost of goods sold to 45% but will provide a better product at the same sales price. The marketing manager projects either option will result in sales increases of 30% per month rather than 20%. Requirements Prepare budgeted income statements for both options, assuming both options begin in January and January sales remain $8,000. Round all calculations to the nearest dollar. Which option should Holly choose? Explain your reasoning.arrow_forwardKirkland Company combines its operating expenses for budget purposes in a selling and administrative expense budget. For the first 6 months of 2020, the following data are available. 1. Sales: 20,300 units quarter 1; 22,000 units quarter 2. 2. Variable costs per dollar of sales: sales commissions 5%, delivery expense 2%, and advertising 3%. 3. Fixed costs per quarter: sales salaries $10,200, office salaries $6,160, depreciation $4,730, insurance $1,660, utilities $890, and repairs expense $610. 4. Unit selling price: $22. Prepare a selling and administrative expense budget by quarters for the first 6 months of 2020. (List variable expenses before fixed expense.) KIRKLAND COMPANY Selling and Administrative Expense Budget Quarter 1 2 Six Monthsarrow_forwardPhoenix Company’s 2019 master budget included the following fixed budget report. It is based on an expected production and sales volume of 15,000 units. Test your template for 15,000 units sales volume to see if you get the same income as stated abovearrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College