Videos

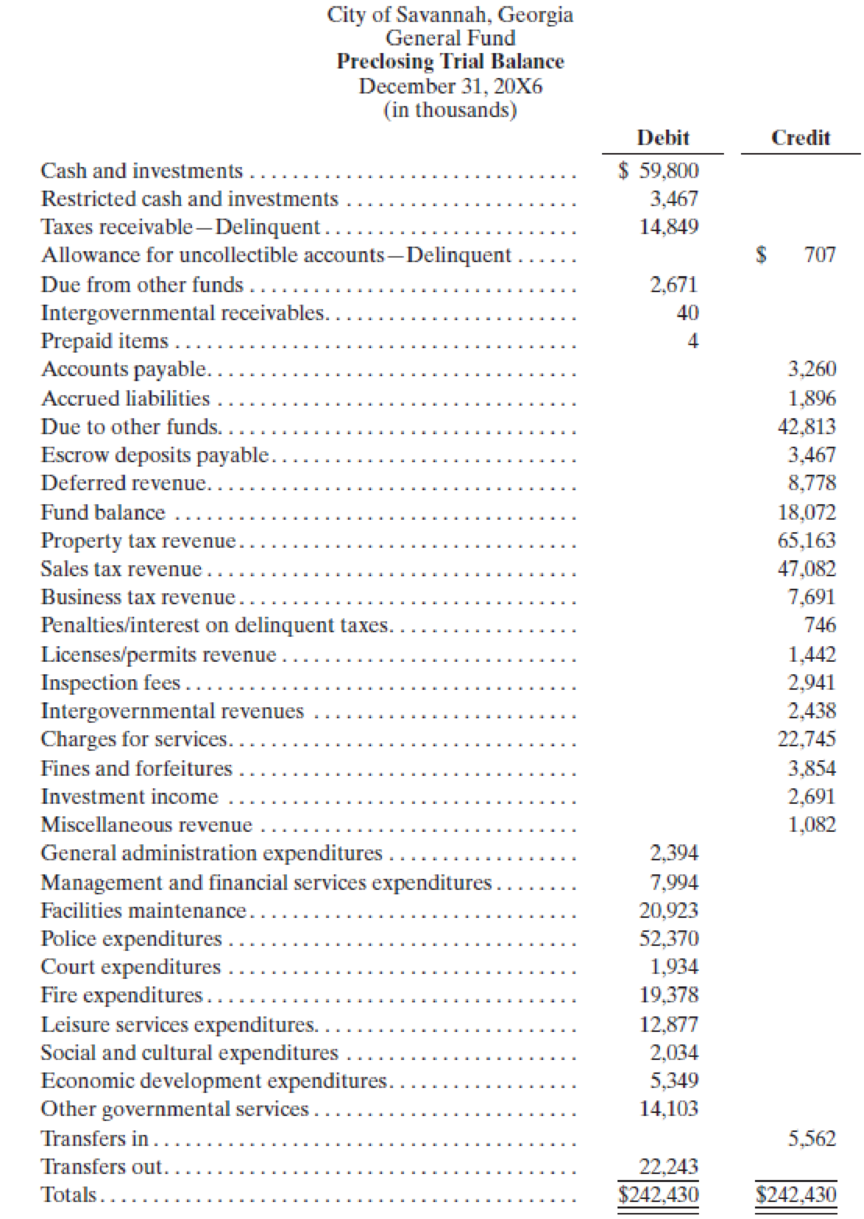

(Financial Statement Preparation—City of Savannah, Georgia) Presented here is the Preclosing

- 1. Outstanding encumbrances as of December 31, 20X6, all related to activities financed from resources available for general purposes, are $1,157

- 2. Receivables are reported at net amounts on the balance sheet.

Required Prepare the City of Savannah, Georgia, Balance Sheet at December 31, 20X6, and its 20X6 Statement of Revenues, Expenditures, and Changes in Fund Balances. The City has taken the formal action required to commit. $500 to economic development activities.

This case was based on the information in a comprehensive annual financial report for the City of Savannah, Georgia.

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Governmental and Nonprofit Accounting (11th Edition)

Additional Business Textbook Solutions

Managerial Accounting (5th Edition)

Financial Accounting

Principles Of Taxation For Business And Investment Planning 2020 Edition

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Introduction To Managerial Accounting

Advanced Financial Accounting

- The City of Stillwater's Airport Authority is included in the reporting entity as an Enterprise Fund. The trial balance for the Airport on June 30, 2018, included the following information: Debit Credit Cash Accounts Receivable Land Plant and Equipment Accumulated Depreciation Accounts Payable Bonds Payable Net Position: 762,453 41,346 3,485,663 25.441.366 12,739,880 60,605 282,809 15,904,340 743,194 29,730,828 Invested in Capital Assets, Net of Related Debt Unrestricted Total 29,730,828 1) Charge for services of $1,245,585 and receipts from customers of $1,213,330. 2) Additions for improvements other than buildings were added for a total cost of $156,996. All fixed asset additions were paid by June 30, 2018. 3) Operating expenses were Interest expense was Payments were made to suppliers Interest was paid 4) Transfers in from the General fund totaled: 2,469,127 22,625 1,586,894 22,625 2,741,794 5) Adjusting entries were as follows: Estimated uncollectible accounts reccivable: 12,456…arrow_forwardThe City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forwardThe City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: 1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance. 2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…arrow_forward

- Journal entries and financial statements for an Internal Service Fund The city of Pleasantville’s Data Processing Fund, an Internal Service Fund, provides services for a fee toall departments of Pleasantville’s government.The Fund had the following transactions and events during calendar year 2021. (There was no fund balanceat the beginning of the year.)1. The General Fund made a $2,000,000 transfer of cash to establish the Data Processing Fund.2. The Data Processing Fund pays cash for a $1,900,000 computer.3. Supplies costing $4,500 were purchased on credit.4. Bills totaling $650,000 were sent to the various city departments.5. Repairs to the computer were made at a cost of $2,400, on credit.6. Collections from city departments for services (see #4) were $629,000.7. Salaries of $200,000 were paid to the employees.8. Accounts payable totaling $5,900 was paid.9. As of the end of the year, $300 of supplies (see #3) had not been used.10. Depreciation expense on the computer for the year…arrow_forward! Required information [The following information applies to the questions displayed below.] The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2024, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Required A Required B Complete this question by entering your answers in the tabs below. Required C VILLAGE OF SEASIDE PINES ENTERPRISE FUND Statement of Net Position December 31, 2024 Net Position: Net Investment in Capital Assets Unrestricted Total Net Position Debits Required: a.…arrow_forwardThe following unadjusted trial balances are for the governmental funds of the City of Copeland prepared from the current accounting records: General Fund Debit Credit Cash $ 19,000 Taxes Receivable 202,000 Allowance for Uncollectible Taxes $ 2,000 Vouchers Payable 24,000 Due to Debt Service Fund 10,000 Unavailable Revenues 16,000 Encumbrances Outstanding 9,000 Fund Balance—Unassigned 103,000 Revenues 176,000 Expenditures 110,000 Encumbrances 9,000 Estimated Revenues 190,000 Appropriations 171,000 Budgetary Fund Balance 19,000 Totals $ 530,000 $ 530,000 Debt Service Fund Debit Credit Cash $ 8,000 Investments 51,000 Taxes Receivable 11,000 Due from General Fund 10,000 Fund Balance—Committed $ 45,000…arrow_forward

- 4. The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2020, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Debits $32,000 47,000 712,000 89,000 479,000 45,000 17,000 40,000 18,000 $1,479,000 Credits $ 96,000 28,000 45,000 12,000 550,000 4,000 119,000 625,000 $1,479,000 Required: a. Prepare the closing entries for December 31. b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended December 31. c. Prepare the Net Position section of the…arrow_forwardOn December 31, Year 1, the following balances were due from the state government to Clare City's various funds: Capital projects $300,000 Special revenue fund $18,000 Investment trust fund100,000 Enterprise 80,000 Custodial fund 100,000 Debt servide fund 100,000 In Clare's December 31, Year 1, financial statements, what amount should be reported in fiduciary funds? $600,000 $400,000. $300,000. $1,050,000arrow_forwardThe City of Grinders Switch Maintains its books in a manner that facilitates the preparation of fund accounting statements and uses worksheet adjustments to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations. General fixed assets as of the beginning of the year, which had not recorded, were as follows: Land $ 7,554,000 Buildings $33,355,000 Improvements Other Than Buildings $14,820,000 Equipment $11,690,000 Accumulated Depreciation, Capital Assets $25,800,000 2. During the year, expenditures for Capital outlays amounted to $7,500,000. Of that amount $4,800,000 was for buildings; the remainder was for improvements other than buildings. 3. The Capital…arrow_forward

- 3. The pre-closing trial balance of the General Fund for the City of Taif shows the following balances at the end of its fiscal year. Budgetary fund balance SAR 20,000 Fund balance, beginning (actual) 150.000 Estimated revenues 830.000 Appropriations 810.000 Revenues (actual) 725.000 Expenditures 675.000 Based on information presented above Prepare closing entries for the budgetary and financial accounts.arrow_forwardThe City of Soheil maintains its books so as to prepare fund accounting statements and prepares worksheet adjustments in order to prepare government-wide financial statements. Required: You are to prepare, in journal form, worksheet adjustments for each of the following situations. General fixed assets, as of the beginning of the year, which had not been recorded, were as follows: Land $ 96,000,000 Buildings 480,000,000 Improvements other than buildings 270,000,000 Equipment 60,000,000 Accumulated depreciation, capital assets 150,000,000 During the year, expenditures for capital outlays amounted to $22,700,000. Of that amount, $10,600,000 was for buildings; $8,300,000 was for improvements other than buildings, $95,000 was capitalized interest and the remainder was for land. The capital outlay expenditures outlined in (B) were completed at the end of the year (no depreciation until next year). For purposes of financial statement…arrow_forwardThe Principal City prepared the Trial Balance of the corporate-type fund as of December 31, 20X1. The enterprise fund was established this year through a transfer from the general fund. After having studied the Trial Balance of the company and the required resources of this module: 1.Prepare the fund's closing entries as of December 31, 20X1.2.Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ending December 31.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education