Principles of Corporate Finance (Mcgraw-hill/Irwin Series in Finance, Insurance, and Real Estate)

12th Edition

ISBN: 9781259144387

Author: Richard A Brealey, Stewart C Myers, Franklin Allen

Publisher: McGraw-Hill Education

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 3, Problem 15PS

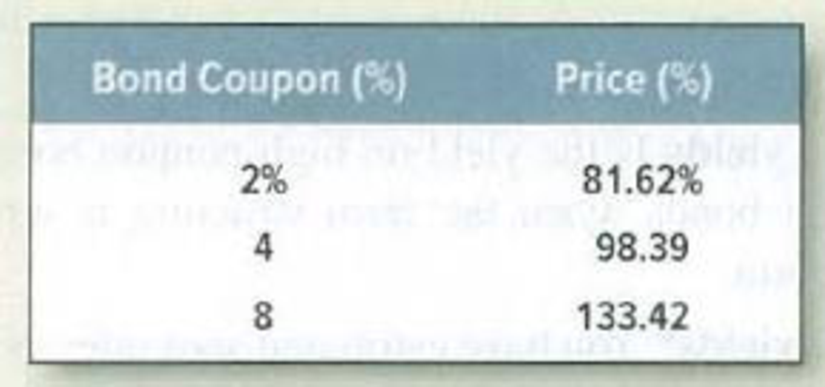

Duration Here are the prices of three bonds with 10-year maturities:

If coupons are paid annually, which bond offered the highest yield to maturity? Which had the lowest? Which bonds had the longest and shortest durations?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of the face value):

Maturity (years)

Price (per $100 face value)

1

$96.32

a. Compute the yield to maturity for each bond.

b. Plot the zero-coupon yield curve (for the first five years).

c. Is the yield curve upward sloping, downward sloping, or flat?

a. Compute the yield to maturity for each bond.

The yield on the 1-year bond is

%. (Round to two decimal places.)

2

$91.93

3

$87.36

4

5

$82.57

$77.42

The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of the face value):

a. Compute the yield to maturity for each bond.

b. Plot the zero-coupon yield curve (for the first five years).

c. Is the yield curve upward sloping, downward sloping, or flat?

a. Compute the yield to maturity for each bond.

The yield on the 1-year bond is 3.92 %. (Round to two decimal places.)

Data table

(Click on the following icon in order to copy its contents into a spreadsheet.)

Maturity (years)

Price (per $100 face value)

1

$95.51

2

3

$91.10

$86.55

$81.69

$76.45

Print

Donday

The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of the face value):.

a. Compute the yield to maturity for each bond.

b. Plot the zero-coupon yield curve (for the first five years).

c. Is the yield curve upward sloping, downward sloping, or flat?

a. Compute the yield to maturity for each bond.

The yield on the 1-year bond is%. (Round to two decimal places.)

Data table

(Click on the following icon

Maturity (years)

Price (per $100 face value)

in order to copy its contents into a spreadsheet.)

2

$91.99

3

$87.33

1

$96.35

Print

Done

4

$82.48

5

$77.37

X

Chapter 3 Solutions

Principles of Corporate Finance (Mcgraw-hill/Irwin Series in Finance, Insurance, and Real Estate)

Ch. 3 - (PRICE) In February 2009, Treasury 8.5s of 2020...Ch. 3 - (YLD) On the same day, Treasury 3.5s of 2018 were...Ch. 3 - (DURATION) What was the duration of the Treasury...Ch. 3 - (MDURATION) What was the modified duration of the...Ch. 3 - Prob. 1PSCh. 3 - Bond prices and yields The following statements...Ch. 3 - Prob. 3PSCh. 3 - Bond prices and yields A 10-year German government...Ch. 3 - Bond prices and yields Construct some simple...Ch. 3 - Spot interest rates and yields Which comes first...

Ch. 3 - Prob. 7PSCh. 3 - Spot interest rates and yields Assume annual...Ch. 3 - Prob. 9PSCh. 3 - Prob. 10PSCh. 3 - Duration True or false? Explain. a....Ch. 3 - Duration Calculate the durations and volatilities...Ch. 3 - Term-structure theories The one-year spot interest...Ch. 3 - Real interest rates The two-year interest rate is...Ch. 3 - Duration Here are the prices of three bonds with...Ch. 3 - Prob. 16PSCh. 3 - Prob. 17PSCh. 3 - Spot interest rates and yields A 6% six-year bond...Ch. 3 - Spot interest rates and yields Is the yield on...Ch. 3 - Prob. 20PSCh. 3 - Prob. 21PSCh. 3 - Duration Find the spreadsheet for Table 3.4 in...Ch. 3 - Prob. 23PSCh. 3 - Prob. 25PSCh. 3 - Prob. 26PSCh. 3 - Prob. 27PSCh. 3 - Prob. 28PSCh. 3 - Prob. 29PSCh. 3 - Prices and yields If a bonds yield to maturity...Ch. 3 - Prob. 31PSCh. 3 - Price and spot interest rates Find the arbitrage...Ch. 3 - Prob. 33PSCh. 3 - Prices and spot interest rates What spot interest...Ch. 3 - Prices and spot interest rates Look one more time...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The return an investor earns on a bond over a period of time is known as the holding period return, defined as interest income plus or minus the change in the bond's price, all divided by the beginning bond price. a. What is the holding period return on a bond with a par value of $1,000 and a coupon rate of 7.5 percent if its price at the beginning of the year was $1,070 and its price at the end was $960? Assume interest is paid annually. Note: Negative value should be indicated by parenthesis. Round your answer to 2 decimal places. Holding period return %arrow_forwardAssume that a bond will make payments every six months as shown on the following timeline (using six- month periods): Period 0 Cash Flows $20.87 a. What is the maturity of the bond (in years)? b. What is the coupon rate (as a percentage)? c. What is the face value? 2 $20.87 *** a. What is the maturity of the bond (in years)? The maturity is years. (Round to the nearest integer.) 39 $20.87 40 $20.87 + $1,000arrow_forwardthe following are three 15-year bonds. The three semiannual coupon rates are 0%, 3.5%, and 7%. Which coupon rate belongs to which bond? What is the shape (“increasing”, “decreasing”, or “flat”) of the term structure of spot rates underlying the valuation of these bonds?arrow_forward

- Complete the following table and draw a graph showing how bond price for each bond changes over time as they move towards their maturity dates. Describe the relationship between bond prices and time remaining for maturity. Years remaining to maturity BOND A Coupon rate = 8% p.a. Market interest rate = 6% p.a. BOND B Coupon rate = 6% p.a. Market interest rate = 6% p.a. BOND C Coupon rate = 4% p.a. Market interest rate = 6% p.a.arrow_forwardAssume that a bond will make payments every six months as shown on the following timeline (using six-month periods): Period 1 2 29 30 Cash Flows $20.37 $20.37 $20.37 $20.37 + $1,000 a. What is the maturity of the bond (in years)? b. What is the coupon rate (as a percentage)? c. What is the face value?arrow_forwardAssume coupons are paid annually. Here are the prices of three bonds with 10-year maturities. Assume face value is $100. Bond Coupon (%) Price (%) 2 81.55 4 98.31 8 133.52 a. What is the yield to maturity of each bond?b. What is the duration of each bond?arrow_forward

- Assume that a bond will make payments every six months as shown on the following timeline (using six-month periods): a. What is the maturity of the bond (in years)? (Round to the nearest integer.)b. What is the coupon rate (as a percentage)? (Round to two decimal places.)c. What is the face value? (Round to the nearest dollar.)arrow_forwardConsider information on the following bonds (with face value 100): Bond Maturity (years) Coupon rate Yield-to-maturity А 1 0% 5.0% В 2 5% 5.5% C 3 6% 6.0% Coupons are paid annually. What is the three-year spot interest rate?arrow_forwardYield to maturity. What is the yield of each of the following bonds, , if interest (coupon) is paid semiannually?arrow_forward

- Suppose the yield on a one year bond is currently 2.5%. Further assume that the expected yield on a one-yea the next four years are, respectively: 2.4%, 2.3%, 2.2%, and 2.1%. Additionally, the term premium on the one-, three-, four-, and five-year bonds are given in the table below: Term Premium on Different Maturity Length Bonds Maturity Length Term Premium one-year 0.00% two-year three-year four-year five-year a. b. flat 0.05% Given the information above, if the yield curve of these five bonds were graphed, it would be 0.10% e. 0.15% downward sloping upward sloping 0.20% C. flat then upward sloping d. upward sloping then downward slopingarrow_forwardThe bond shown in the following table pays interest annually in the table attached. a. Calculate the yield to maturity (YTM) for the bond. b. What relationship exists between the coupon interest rate and yield to maturity and the par value and market value of a bond? Explain.arrow_forwardAssume coupons are paid annually. Here are the prices of three bonds with 10-year maturities. Assume face value is $100. Bond Coupon (%) 2 Price (%) 48 80.57 97.19 134.92 a. What is the yield to maturity of each bond? b. What is the duration of each bond? Complete this question by entering your answers in the tabs below. Required A Required B What is the yield to maturity of each bond? Note: Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places. Bond Coupon YTM (%) 2 4 6.00 % 7.42% 8 7.01 %arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

Journalizing Bonds Payable/Amortization of a Premium; Author: TLC Tutoring;https://www.youtube.com/watch?v=5gEpAFFnIE8;License: Standard YouTube License, CC-BY

Investing Basics: Bonds; Author: TD Ameritrade;https://www.youtube.com/watch?v=IuyejHOGCro;License: Standard YouTube License, CC-BY