PRIN.OF CORPORATE FINANCE

13th Edition

ISBN: 9781260013900

Author: BREALEY

Publisher: RENT MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 3, Problem 13PS

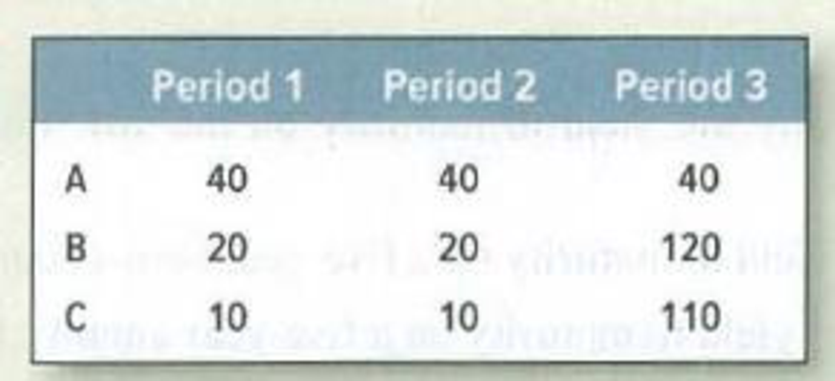

Duration Calculate the durations and volatilities of securities A, B, and C. Their cash flows are shown below. The interest rate is 8%.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

he interest rate used to calculate the present value of a bond's cash flows is often referred to as the:Group of answer choices dividend rate. discount rate. multiplier. yield to maturity

13. Duration Calculate the durations and volatilities of securities A, B, and C. Their cash flows

are shown below. The interest rate is 8%.

A

B

C

Period 1

40

20

10

Period 2

40

20

10

Period 3

40

120

110

Which of the following is an example of a money market instrument? (Select all that apply)

a. 2-year Treasury Bond

b. Certificate of Deposit

C. Swap

d. Stop-call

Chapter 3 Solutions

PRIN.OF CORPORATE FINANCE

Ch. 3 - (PRICE) In February 2009, Treasury 8.5s of 2020...Ch. 3 - (YLD) On the same day, Treasury 3.5s of 2018 were...Ch. 3 - (DURATION) What was the duration of the Treasury...Ch. 3 - (MDURATION) What was the modified duration of the...Ch. 3 - Bond prices and yields A 10-year bond is issued...Ch. 3 - Bond prices and yields The following statements...Ch. 3 - Bond prices and yields Construct some simple...Ch. 3 - Bond prices and yields A 10-year German government...Ch. 3 - Bond prices and yields A 10-year German government...Ch. 3 - Bond prices and yields A 10-year U.S. Treasury...

Ch. 3 - Bond returns If a bonds yield to maturity does not...Ch. 3 - Bond returns a. An 8%, five-year bond yields 6%....Ch. 3 - Prob. 10PSCh. 3 - Duration True or false? Explain. a....Ch. 3 - Duration Here are the prices of three bonds with...Ch. 3 - Duration Calculate the durations and volatilities...Ch. 3 - Prob. 14PSCh. 3 - Duration Find the spreadsheet for Table 3.4 in...Ch. 3 - Prob. 16PSCh. 3 - Spot interest rates and yields Which comes first...Ch. 3 - Prob. 18PSCh. 3 - Spot interest rates and yields Look again at Table...Ch. 3 - Prob. 20PSCh. 3 - Spot interest rates and yields Assume annual...Ch. 3 - Spot interest rates and yields A 6% six-year bond...Ch. 3 - Spot interest rates and yields Is the yield on...Ch. 3 - Prob. 24PSCh. 3 - Measuring term structure The following table shows...Ch. 3 - Term-structure theories The one-year spot interest...Ch. 3 - Term-structure theories Look again at the spot...Ch. 3 - Real interest rates The two-year interest rate is...Ch. 3 - Prob. 30PSCh. 3 - Bond ratings A bonds credit rating provides a...Ch. 3 - Prob. 32PSCh. 3 - Price and spot interest rates Find the arbitrage...Ch. 3 - Prob. 34PSCh. 3 - Prices and spot interest rates What spot interest...Ch. 3 - Prices and spot interest rates Look one more time...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The Macaulay duration is the weighted average number of coupon periods until a bond’s scheduled cash flows. Select one: True Falsearrow_forwardIn a bond portfolio, the following are the present values of all cash flows by annual period: Year PV Cash flows (millions) 1 14.3 2 13.2 3 15.3 4 10.5 5 18.4 What is the percentage contribution to duration of the year 3 cash flows? Enter answer in percents.arrow_forwardThe actual interest paid or earned is commonly referred to as the: a. Risk premium. b. Annual effective interest rate. c. Nominal interest rate. d. Real rate of return.arrow_forward

- A balance sheet that displays only component percentages is a a.comparative balance sheet. b.condensed balance sheet. c.common-sized balance sheet. d.trend balance sheet. If the straight-line method of amortization of bond premium or discount is used, which of the following statements is true? A. Annual interest expense will remain the same over the life of the bonds with the amortization of bond discount. B. Annual interest expense will increase over the life of the bonds with the amortization of bond discount. C. Annual interest expense will decrease over the life of the bonds with the amortization of bond discount. D. Annual interest expense will increase over the life of the bonds with the amortization of bond premium. A statement of cash flows would be least useful in answering which of the following questions? Double-click on the box below to edit your answer choices. A.Cash used to purchase equipment B.Change in total expenses C.cash provided from sale of stockarrow_forwardThe dollar interest received divided by the market price of the bond is called the Group of answer choices A. current yield. B. yield to maturity. C. coupon rate. D. par value.arrow_forwardListed below are several terms and phrases associated with current liabilities. Pair each item from List A (by letter) with the item from List B that is most appropriately associated with it. 1. 2. Payable with current assets. 3. List A Face amount x Interest rate x Time. 4. a. b. Short-term debt to be refinanced with common stock. c. Present value of interest plus present value of principal. 5. Noninterest-bearing. 6. Noncommitted line of credit. 7. Pledged accounts receivable. 8. Reclassification of debt. 9. Purchased by other corporations. 10. Expenses not yet paid. 11. Liability until refunded. 12. Liability until satisfy performance obligation d. e. f. g. |h. I. J. k. 1. List B Informal agreement Secured loan Refinancing prior to the issuance of the financial statements Accounts payable Accrued liabilities Commercial paper Current liabilities Long-term liability Usual valuation of liabilities Interest on debt Customer advances Customer depositsarrow_forward

- Calculate the durations and volatilities of securities A, B, and C. Their cash flows are shown below. The interest rate is 6%. (Do not round intermediate calculations. Round "Duration" to 4 decimal places and "Volatility" to 2 decimal places.) Period 1 Period 2 Period 3 Duration Volatility A B C Duration Volatility 85 85 130 --------years ---------- 65 65 210 --------years --------- 55 55 200 --------years ----------arrow_forwardThe yield to maturity reported in the financial pages for Treasury securities A. is calculated by doubling the semiannual yield. B. is calculated by doubling the semiannual yield and is also called the bond equivalent yield. C. is calculated as the yield-to-call for premium bonds. D. is also called the bond equivalent yield. E. is calculated by compounding the semiannual yield.arrow_forwardThe amount of no.3 is to be amortized. Calculate the interest portion of the 4th coupon.arrow_forward

- Define each of the following terms:b. Par value; maturity date; coupon payment; coupon interest ratearrow_forwardThis first table describes prevailing market interest rates. Market Data Yield 0.05 Required: Using the yield above and the information contained in the table below, please calculate the price and duration of the bond as well as all necessary steps. (Use cells A5 to B5 from the given information to complete this question.) Time Until Payment Payment Discounted Payment Weight Time × Weight 1.00 $30.00 2.00 $30.00 3.00 $30.00 4.00 $1,030.00 Price: Durationarrow_forward25) The coupon rate is identified on the bond indenture and determines the amount of cash payment for each period. TRUE FALSEarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education

Liquidity Risk (FRM Part 2 – Book 4 – Chapter 1); Author: AnalystPrep;https://www.youtube.com/watch?v=TguAvyxM6vg;License: Standard Youtube License