Videos

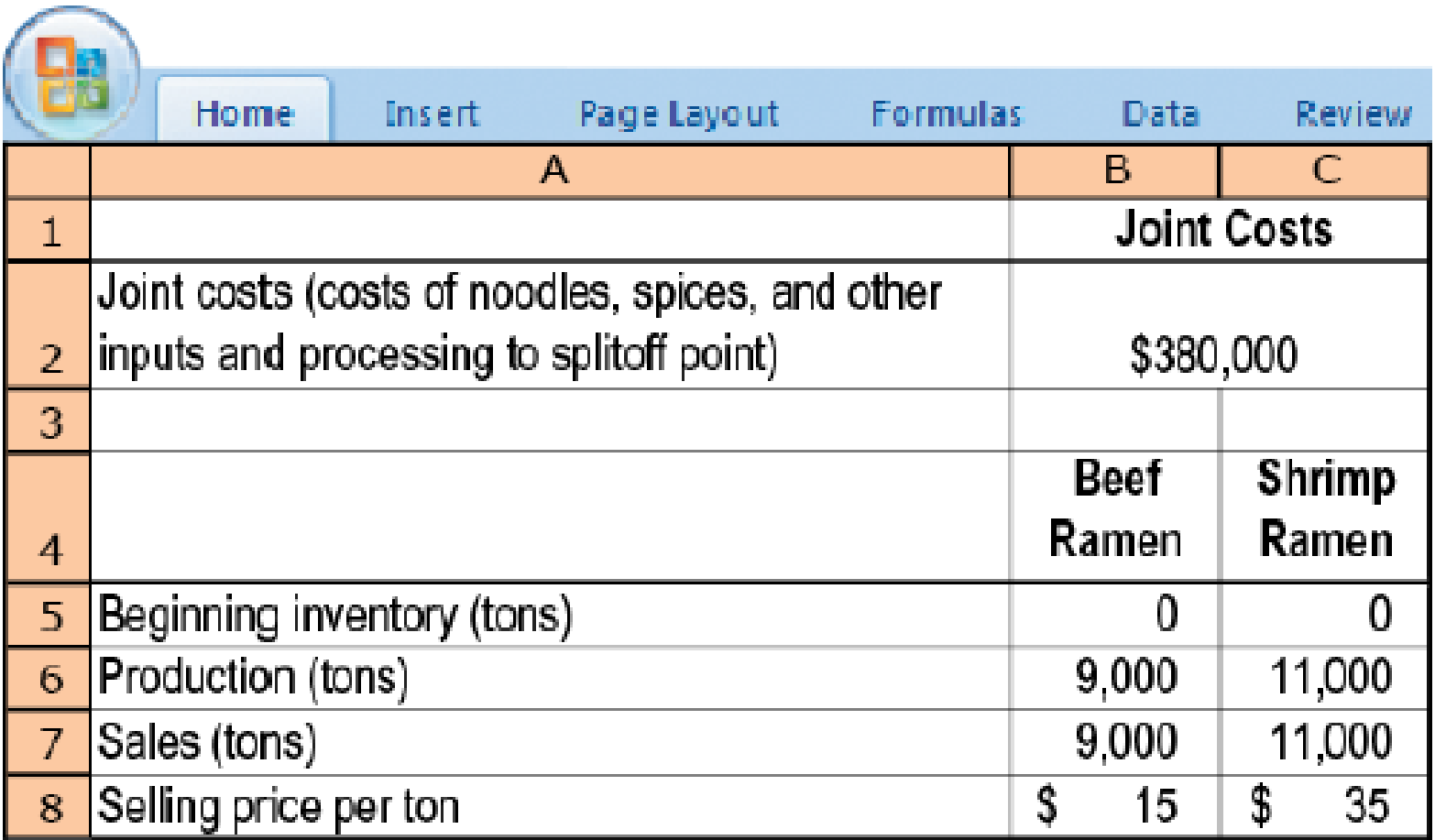

Joint-cost allocation, sales value, physical measure, NRV methods. Tasty Foods produces two types of microwavable products: beef-flavored ramen and shrimp-flavored ramen. The two products share common inputs such as noodle and spices. The production of ramen results in a waste product referred to as stock, which Tasty dumps at negligible costs in a local drainage area. In June 2017, the following data were reported for the production and sales of beef-flavored and shrimp-flavored ramen:

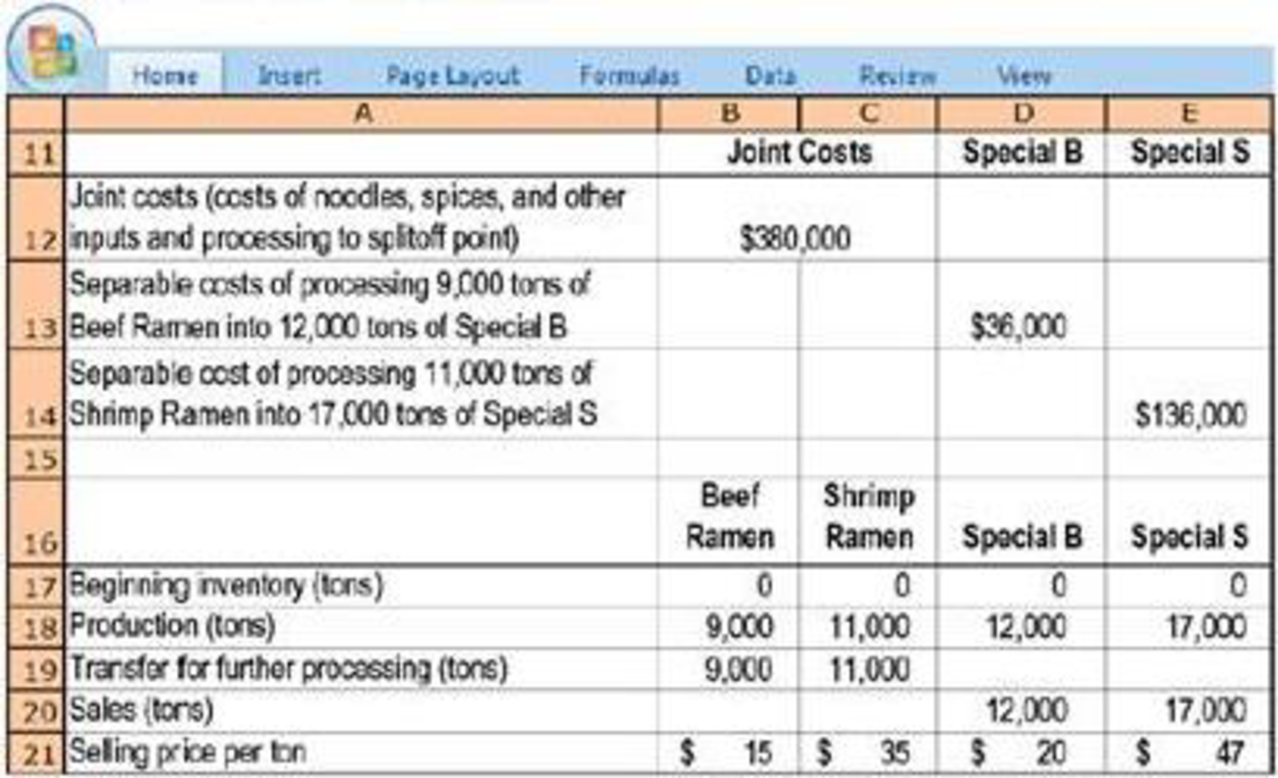

Due to the popularity of its microwavable products, Tasty decides to add a new line of products that targets dieters. These new products are produced by adding a special ingredient to dilute the original ramen and are to be sold under the names Special B and Special S, respectively. Following are the monthly data for all the products:

- 1. Calculate Tasty’s gross-margin percentage for Special B and Special S when joint costs are allocated using the following:

Required

- a. Sales value at splitoff method

- b. Physical-measure method

- c. Net realizable value method

Trending nowThis is a popular solution!

Chapter 16 Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- Accounting for a main product and a byproduct (Cheatham and green, adapted)Crispy,Inc., is a producer of potato chips. A single production process at crispy, Inc., yields potato chips as the main product, as well as byproduct that can be sold as a snack. Both products are fully processed by the splitoff point, and there are no separable costs. For September 2017, the cost of operations is $520,000. Production and sales data are as follows:arrow_forwardROI performance measures based on historical cost and current cost. Nature’s Juice Corporation operates three divisions that process and bottle natural fruit juices. The historical-cost accounting system reports the following information for 2017:arrow_forwardThis cost data from Hickory Furniture is for the year 2017. Using the high-low method, express the companys utility costs as an equation where X represents number of tables produced. Predict the utility costs if 800 tables are produced. Predict the utility costs if 600 tables are produced. Using Excel, create a scatter graph of the cost data and explain the relationship between number of tables produced and utility expenses.arrow_forward

- (Physical measure joint cost allocation) Powisett Farms Dairy began opera-tions at the start of May 2010. Powisett Farms operates a fleet of trucks to gather whole milk from local farmers. The whole milk is then separated into two joint products: skim milk and cream. Both products are sold at the split-off point to dairy wholesalers. For May, the firm incurred the following joint costs:Whole milk purchase cost $400,000Direct labor costs 180,000Overhead costs 292,000Total product cost $872,000During May, the firm processed 2,000,000 gallons of whole milk, producing 1,555,500 gallons of skim milk and 274,500 gallons of cream. The remaining gallons of the whole milk were lost during processing. There was no Raw Material or Work in Process Inventory at the end of May.After the joint process, the skim milk and cream were separately processed at costs, respectively, of $67,660 and $83,310. Of the products produced, Powisett Farms Dairy sold 1,550,000 gallons of skim milk for $1,472,500 and…arrow_forward1. ABC Corp is the owner of MBT bottling, a bulk soft-drink producer. A single process yields tow bulk soft drinks: Rain Dew (Main product) and Resi Dew (by product). Both products are fully processed at the split off point and there are no separable cost.For July 2015, the cost of soft drink operations is P 120,000 (Joint cost). Production and sales data are as follows: Main product and by product’s production are 20,000 liters and 4,000 liters, respectively ; sales price is 12 per liter for main and 2 per liter for by product; the unsold liters are 4,000 liters for Main product and 600 liters for by product. Operating expenses are as follows: Rent expense of P 5,000; salaries expense of P 4,000 and other expenses of P 6,000. By-Product is recognized at time of production. There were no beginning inventories on July 1, 2015. What is the gross margin for the company? choose the answer from the following: 99,200 84,200 102,000 96,200 None of the above 2. ABC Corp is the owner of…arrow_forwardPremium Candy Inc. is a producer of premium chocolate based in Palo Alto. For 2017, the trucking fleet had a practical capacity of 85 round-trips between the Palo Alto plant and the two suppliers. It recorded the following information: Premium Candy Inc. decides to examine the effect of using the dual-rate method for allocating truck costs to each round-trip. Read the requirements4. Requirement 1. Using the dual-rate method, what are the costs allocated to the dark chocolate division and the milk chocolate division when (a) variable costs are allocated using the budgeted rate per round-trip and actual round-trips used by each division and when (b) fixed costs are allocated based on the budgeted rate per round-trip and round-trips budgeted for each division? Dark chocolate Milk chocolate Variable costs Fixed costs Total costs Requirement 2. From the viewpoint of the dark chocolate…arrow_forward

- (Physical measure joint cost allocation) Powisett Farms Dairy began opera-tions at the start of May 2010. Powisett Farms operates a fl eet of trucks to gather whole milk from local farmers. The whole milk is then separated into two joint products: skim milk and cream. Both products are sold at the split-off point to dairy wholesalers. For May, the firm incurred the following joint costs:Whole milk purchase cost $400,000Direct labor costs 180,000Overhead costs 292,000Total product cost $872,000During May, the fi rm processed 2,000,000 gallons of whole milk, producing 1,555,500 gallons of skim milk and 274,500 gallons of cream. The remaining gallons of the whole milk were lost during processing. There was no Raw Material or Work in Process Inventory at the end of May.After the joint process, the skim milk and cream were separately processed at costs,respectively, of $67,660 and $83,310. Of the products produced, Powisett Farms Dairy sold 1,550,000 gallons of skim milk for $1,472,500 and…arrow_forwardNet realizable value method. Sweeney Company is one of the world’s leading corn reners. It produces two joint products —corn syrup and corn starch—using a common production process. In July 2017, Sweeney reported the following production and selling-price information:arrow_forwardYalland Manufacturing Company makes two different products, M and N. The company’s two departments are named after the products; for example, Product M is made in Department M. Yalland’s accountant has identified the following annual costs associated with these two products. Identify the costs that are (1) direct costs of Department M, (2) direct costs of Department N, and (3) indirect costs. Select the appropriate cost drivers for the indirect costs and allocate these costs to Departments M and N. Determine the total estimated cost of the products made in Departments M and N. Assume that Yalland produced 2,000 units of Product M and 4,000 units of Product N during the year. If Yalland prices its products at cost plus 40 percent of cost, what price per unit must it charge for Product M and for Product N?arrow_forward

- Net realizable value method. Sweeney Comapny is one of the world’s leading corn refiners. It produces two joint products –corn syrup and corn starch- using a common production process. In July 2017, Sweeney reported the following production and selling-price information:arrow_forwardA company manufactures two joint products at a joint cost of 1,000. These products can be sold at split-off, or when further processed at an additional cost, sold as higher quality items. The decision to sell at split-off or further process should be based on the: A. allocation of the 1,000 joint cost using the quantitative unit measure B. assumption that the 1,000 joint cost is irrelevant C. allocation of the $1,000 joint cost using the relative sales value approach D. assumption that the 1,000 joint cost must be allocated using a physical-measure approach E. allocation of the 1,000 joint cost using any equitable and rational allocation basisarrow_forwardCicleta Manufacturing has four activities: receiving materials, assembly, expediting products, and storing goods. Receiving and assembly are necessary activities; expediting and storing goods are unnecessary. The following data pertain to the four activities for the year ending 20x1 (actual price per unit of the activity driver is assumed to be equal to the standard price): Required: 1. Prepare a cost report for the year ending 20x1 that shows value-added costs, non-value-added costs, and total costs for each activity. 2. Explain why expediting products and storing goods are non-value-added activities. 3. What if receiving cost is a step-fixed cost with each step being 1,500 orders whereas assembly cost is a variable cost? What is the implication for reducing the cost of waste for each activity?arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College