Videos

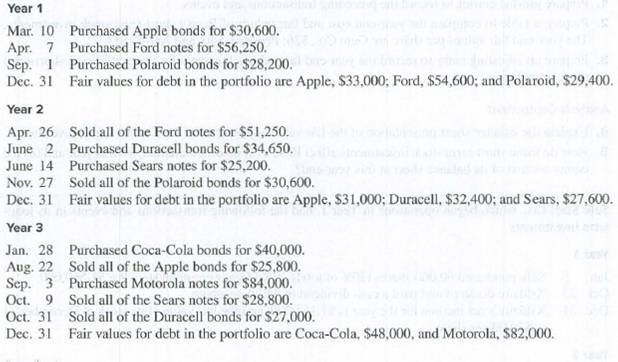

Paris Inc. began operations in Year 1. Following is a series of transactions and events involving its long-term debt investments in available-for-sale securities.

Required

- 1. Prepare

journal entries to record these transactions and events and any year-end fair value adjustments to the portfolio of long-term available-for-sale debt securities. - 2. Prepare a table that summarizes the (a) total cost, (b) total fair value adjustment, and (c) total fair value for the portfolio of long-term available-for-sale debt securities at each year-end.

- 3. Prepare a table that summarizes (a) the realized gains and losses and (b) the unrealized gains or losses for the portfolio of long-term available-for-sale debt securities at each year-end.

1.

Prepare journal entries to record the given transaction.

Explanation of Solution

Journal entry:

Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Prepare the journal entries to record the given transactions as follows:

| Journal | ||||

| Date | Account Title and Explanation | Post | Debit | Credit |

| Ref. | ($) | ($) | ||

| March 10, Year 1 | Debt Investments -AFS (Company A) | 30,600 | ||

| Cash | 30,600 | |||

| (To record the purchase of bonds) | ||||

| April 7, Year 1 | Debt Investments—AFS (Company F) | 56,250 | ||

| Cash | 56,250 | |||

| (To record the purchase of F notes) | ||||

| September, 1 Year 1 | Debt Investments —AFS (Company P) | 28,200 | ||

| Cash | 28,200 | |||

| (To record the purchase of bonds) | ||||

| December 31, Year 1 | Fair Value Adjustment—AFS | 1,950 | ||

| Unrealized Gain—Equity (LT) (2) | 1,950 | |||

| (To record the annual adjustment to fair value of securities) | ||||

| April 26, Year 2 | Cash | 51,250 | ||

| Loss on sale of debt investments (3) | 5,000 | |||

| Debt investment—AFS (Company F) | 56,250 | |||

| (To record the gain on sale of bond) | ||||

| June 2, Year 2 | Debt Investments—AFS (Company D) | 34,650 | ||

| Cash | 34,650 | |||

| (To record the purchase of bond) | ||||

| June 14, Year 2 | Debt Investments —AFS (Company S) | 25,200 | ||

| Cash | 25,200 | |||

| (To record the purchase of bond) | ||||

| November, 27 Year 2 | Cash | 30,600 | ||

| Gain on Sale of Investments (4) | 2,400 | |||

| Debt Investments—AFS (Company P) | 28,200 | |||

| (To record the loss on sale of bond) | ||||

| December 31, Year 2 | Fair Value Adjustment—AFS | 1,400 | ||

| Unrealized Gain—Equity (LT) (6) | 1,400 | |||

| (To record the Annual adjustment to fair value of securities) | ||||

| January 28, Year 3 | Debt Investments—AFS (Company C) | 40,000 | ||

| Cash | 40,000 | |||

| (To record the purchase of bonds) | ||||

| August 22, Year 3 | Cash | 25,800 | ||

| Loss on Sale of Investments (7) | 4,800 | |||

| Debt Investments—AFS (Company A) | 30,600 | |||

| (To record the sale of bond) | ||||

| September 3, Year 3 | Debt Investments—AFS (Company M) | 84,000 | ||

| Cash | 84,000 | |||

| (To record the purchase of bonds) | ||||

| October 9, Year 3 | Cash | 28,800 | ||

| Gain on Sale of Investments (8) | 3,600 | |||

| Debt Investments—AFS (Company S) | 25,200 | |||

| (To record the sale of bonds) | ||||

| October 31, Year 3 | Cash | 27,000 | ||

| Loss on Sale of Investments (9) | 7,650 | |||

| Debt Investments—AFS (Company D) | 34,650 | |||

| (To record the sale of bond) | ||||

| December 31, Year 3 | Fair Value Adjustment—AFS | 5,450 | ||

| Unrealized Gain—Equity (LT) (11) | 5,450 | |||

| (To record the Annual adjustment to fair value of securities) | ||||

Table (1)

Working note:

Calculate the total cost and fair value of the bonds for Year 1:

| Name of the company | Cost of debt investment | Fair value of debt investment |

| Company A | $30,600 | $33,000 |

| Company F | $56,250 | $54,600 |

| Company P | $28,200 | $29,400 |

| Total | $115,050 | $117,000 |

Table (2)

…… (1)

Calculate the unrealized gain or loss for year 1:

Calculate the value of cash received from the sale of stock investment (Company F stocks)

Calculate the value of cash received from the sale of stock investment (Company P stocks)

Calculate the total cost and fair value of the bonds for Year 2:

| Name of the company | Cost of debt investment | Fair value of debt investment |

| Company A | S30,600 | $31,200 |

| Company F | $34,650 | $32,400 |

| Company S | $25,200 | $27,600 |

| Total | $90,450 | $91,000 |

Table (3)

…… (5)

Calculate the unrealized gain or loss for year 2:

Calculate the value of cash received from the sale of stock investment (Company A stocks)

Calculate the value of cash received from the sale of stock investment (Company S stocks)

Calculate the value of cash received from the sale of stock investment (Company D stocks)

Calculate the total cost and fair value of the bonds for Year 3:

| Name of the company | Cost of debt investment | Fair value of debt investment |

| Company C | $40,000 | $48,000 |

| Company M | $84,000 | $82,000 |

| Total | $124,000 | $130,000 |

Table (4)

…… (10)

Calculate the unrealized gain or loss for year 3:

2.

Prepare a table that summarizes the following

- a. Total cost,

- b. Total fair value adjustments,

- c. Total fair value of the portfolio of long-term available-for-sale securities at year-end.

Explanation of Solution

Prepare a table that summarizes the total cost, total fair value adjustments, and the total fair value as follows:

| Particulars | December 31, Year 1 | December 31, Year 2 | December 31, Year 3 |

| a. Long-term AFS Securities (cost) | $115,050 | $90,450 | $124,000 |

| b. Fair Value Adjustment | 1,950 | 550 | 6,000 |

| c. Long-term AFS Securities (fair value) | $117,000 | $91,000 | $130,000 |

Table (5)

3.

Prepare a table that summarizes the following

- a. The realized gains and losses,

- b. The unrealized gains and losses for the portfolio of long-term available-for-sale securities at year-end.

Explanation of Solution

- a. Prepare a table that summarizes the realized gains and losses as follows:

| Particulars | Year 1 | Year 2 | Year 3 |

| Realized gains (losses) | |||

| Sale of F shares | $(5,000 ) | ||

| Sale of P shares | 2,400 | ||

| Sale of A shares | $(4,800) | ||

| Sale of S shares | $3,600 | ||

| Sale of D shares | $(7,650) | ||

| Total realized gain (loss) | $0 | $ (2,600) | $(8,850) |

Table (6)

- b. Prepare a table that summarizes the Unrealized gains and losses as follows

| Particulars | Year 1 | Year 2 | Year 3 |

| Unrealized gains (losses) at year-end | $1,950 | $ 550 | $ 6,000 |

Table (7)

Want to see more full solutions like this?

Chapter 15 Solutions

Principles of Financial Accounting.

- Indicate where each of the following items 1 through 5 is reported on financial statements. 1. Unrealized gain on available-for-sale securities 2. Held-to-maturity securities (due in 15 years) 3. Loss on sale of debt indestments 4. Fair Value Adjustment-Stock (Short term) 5. Unrealized gain on trading securities Equityarrow_forwardKitty Company began operations in the current year and acquired short-term debt investments in trading securities. The year-end cost and fair values for its portfolio of these debt investments follow. Trading Securities Tesla Bonds Nike Bonds Ford Bonds (1) After the fair value adjustment is made, prepare the assets section of Kitty Company's December 31 classified balance sheet. (2) In which income statement section is the unrealized gain (or loss) on the portfolio of trading securities reported? Required 1 Cost $ 12,900 21, 200 5,300 Complete this question by entering your answers in the tabs below. Required 2 Fair Value $ 9,675 22,260 4,240 KITTY COMPANY Assets Section of Balance Sheet December 31 Assets After the fair value adjustment is made, prepare the assets section of Kitty Company's December 31 classified balance sheet. Note: Amounts to be deducted should be indicated with a minus sign.arrow_forwardTicker Services began operations in Year 1 and holds long-term investments in available-for-sale debt securities. The year-end cost and fair values for its portfolio of these investments follow. Portfolio of Available-for-Sale Securities December 31, Year 1 December 31, Year 2 Cost $ 13,000 20,000 23,000 16,500 December 31, Year 3 December 31, Year 4 Complete this question by entering your answers in the tabs below. Prepare journal entries to record each year-end fair value adjustment for these securities. Adjustment General Journal Calculation Calculation adjustment required to fair value adjustment. 12/31/Year 1 Existing balance in Fair Value Adjustment-AFS (LT) Required balance in Fair Value Adjustment-AFS (LT) Adjustment required to Fair Value Adjustment-AFS (LT) 12/31/Year 2 Existing balance in Fair Value Adjustment-AFS (LT) Required balance in Fair Value Adjustment-AFS (LT) Adjustment required to Fair Value Adjustment-AFS (LT) 12/31/Year 3 Existing balance in Fair Value…arrow_forward

- Instructions: (Assume all transactions during the year were for cash.) a. Prepare the journal entry to record the sale of the available-for-sale debt securities in 2020. b. Prepare the journal entry to record the Unrealized Holding Gain or Loss for 2020. c. Prepare a statement of comprehensive income for 2020. d. Prepare a balance sheet as of December 31, 2020arrow_forwardRequired information [The following information applies to the questions displayed below.] Kitty Company began operations in the current year and acquired short-term debt investments in trading securities. The year-end cost and fair values for its portfolio of these debt investments follow. Trading Securities Tesla Bonds Nike Bonds Ford Bonds View transaction listarrow_forwardDuring the current year, Reed Consulting acquired long-term available-for-sale debt securities on July 1 at a $76,000 cost. At its December 31 year-end, these securities had a fair value of $63,400. This is the first and only time the company purchased such securities. 1. Prepare the July 1 entry to record the purchase of these debt securities. 2. Prepare the year-end adjusting entry related to these securities. View transaction list Journal entry worksheet 1 2 Record purchase of available-for-sale securities. Note: Enter debits before credits. Date July 01 Record entry General Journal Clear entry Debit Credit View general journalarrow_forward

- At December 31, 2021, Hull-Meyers Corp. had the following investments that were purchased during 2021, its first year of operations: Trading Securities: Security A Security B Totals Securities Available-for-Sale: Security C Security D Totals Securities to Be Held-to-Maturity: Security E Security F Totals Trading Securities Security A Security B Securities Available-for-Sale Security C Security D Securities to be Held-to-Maturity Security E Security F Totals Amortized cost Reported on Balance Sheet as: Current assets $ 905,000 110,000 $1,015,000 Noncurrent assets $ 705,000 905,000 $1,610,000 $ 495,000 620,000 $1,115,000 No investments were sold during 2021. All securities except Security D and Security F are considered short-term investments. None of the fair value changes is considered permanent. Required: Complete the following table. (Amounts to be deducted should be indicated with a minus sign.) Fair Value $915,500 104,900 $1,020,400 $ 784,500 920, 200 $1,704,700 Net Income (I/S) $…arrow_forwardRios Financial Co. is a regional insurance company that began operations on January 1, Year 1. The following transactions relate to trading securities acquired by Rios Financial Co., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. Prepare the investment-related current asset balance sheet presentation for Rios Financial Co. on December 31, Year 2. 3. How are unrealized gains or losses on trading investments presented in the financial statements of Rios Financial Co.?arrow_forwardRekya Mart Inc. is a general merchandise retail company that began operations on January 1, Year 1. The following transactions relate to debt investments acquired by Rekya Mart Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. If the bond portfolio is classified as available for sale, what impact would this have on financial statement disclosure?arrow_forward

- Refer to the information in RE13-5. Assume that on December 31, 2019, the investment in Smith Corporation bonds has a market value of 12,500. Prepare the year-end journal entry to record the unrealized gain or loss.arrow_forwardThe following equity investment transactions were completed by Romero Company during a recent year: Journalize the entries for these transactions.arrow_forwardComplete the following table by putting the proper amount in each column: Assume that $100,000 was invested in each of the following classifications and the market value at the end of the year was $95,000. (For the Current Long term column indicate which classification is correct assuming there are no current maturities on long-term investments) Investment Type Carrying Value Current (C) or Long Term (LT) Adjustment To Income Adjustment to Other Comp Inc Debt Investment Trading Available-For-Sale Held-to-Maturity Equity Investment < 20% Ownership >21%,<50% Ownershiparrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning